Walmart (WMT) shares have tracked slightly lower over the past month, with investors quietly weighing the latest shifts in retail demand and broader market trends. The stock remains a key barometer for the consumer sector.

Walmart’s share price has pulled back nearly 6% over the past month after a strong run earlier this year. Recent moves reflect investors’ shifting optimism and caution amid changing retail trends. That said, its 1-year total shareholder return of 18.2% and a remarkable 108% over three years show plenty of long-term momentum behind the stock.

With shares easing back from their highs and still trading below most analyst price targets, investors are considering whether Walmart is currently undervalued or if the market is already pricing in all of the retail giant’s future growth.

Advertisement

Most Popular Narrative: 10.9% Undervalued

Walmart’s latest fair value estimate stands at $113.78 per share, roughly 11% higher than its recent close. This gap has investors questioning what’s fueling such confidence in future upside.

Expansion of high-margin business streams such as Walmart Connect (advertising, up 31-46% globally), marketplace, and Walmart+ memberships (global advertising up 46%, membership income up 15%) is diversifying Walmart's income base beyond retail. This is gradually transforming the company's profit mix and resulting in structurally higher net margins and earnings over time.

Want to know what’s powering Walmart’s recent valuation boost? The most followed perspective backs up this price with bold growth assumptions, shifting profit streams, and margin ambitions. Which surprising forecasts unlock this potential? Dive in and see how this narrative assembles its high-conviction price target.

However, persistent cost pressures or setbacks in international expansion could threaten Walmart’s ability to deliver the margin gains and growth that analysts are counting on.

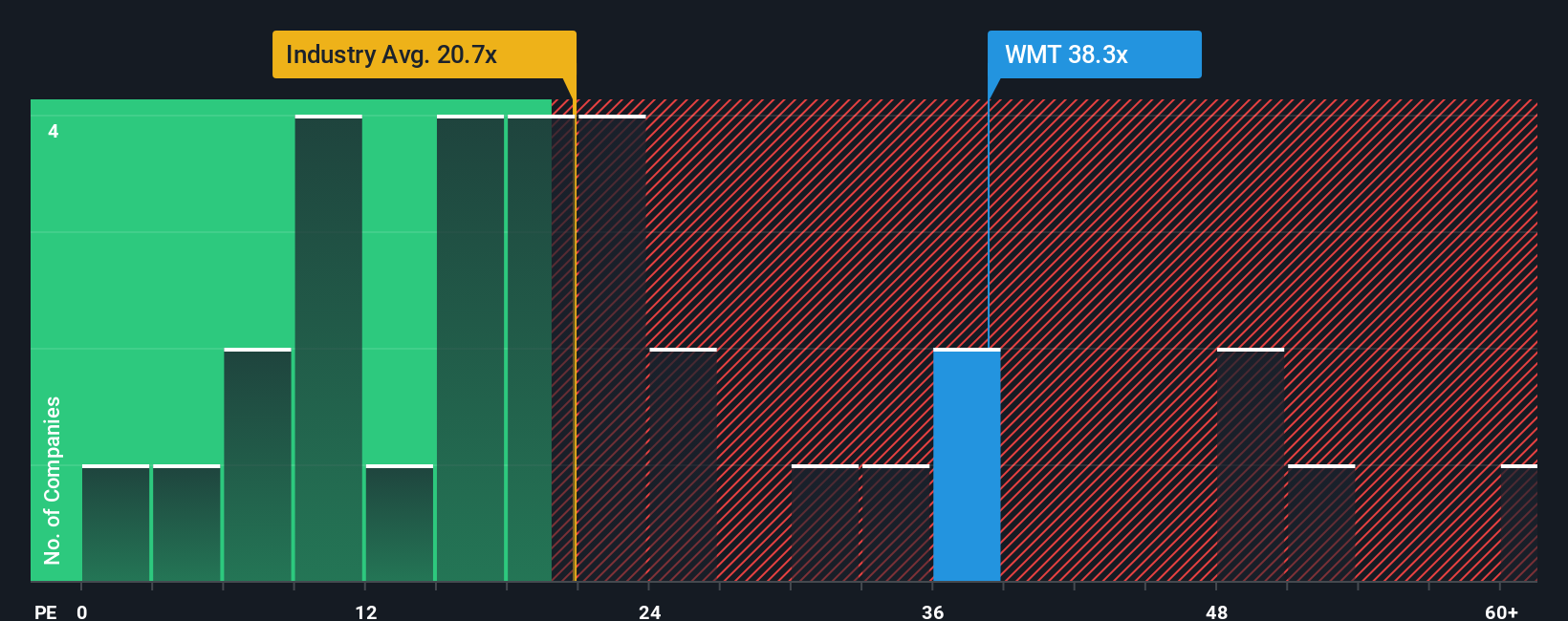

While our previous analysis suggests Walmart is undervalued, looking through the lens of its price-to-earnings ratio paints a different picture. Walmart trades at 37.9x earnings, a notable premium over both its peers (24.8x) and the industry average (21.1x). Even compared to its fair ratio of 35.1x, the shares appear expensive, raising questions about valuation risk if market sentiment shifts. Is this premium a sign of untapped growth or growing complacency among investors?

If the mainstream outlook does not match your view, or you would rather rely on your own research, it only takes a few minutes to chart your own course and Do it your way.

Expand your portfolio with promising stocks beyond the retail sector. With the right tools, you can spot unique trends and make confident investment decisions before the crowd does.

Tap into the future of medicine by checking out these 31 healthcare AI stocks, which offers innovation in artificial intelligence for healthcare breakthroughs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Walmart might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.