Advertisement

- United States

- /

- Food and Staples Retail

- /

- NasdaqCM:HFFG

Is HF Foods Group (NASDAQ:HFFG) A Risky Investment?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, HF Foods Group Inc. (NASDAQ:HFFG) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for HF Foods Group

What Is HF Foods Group's Debt?

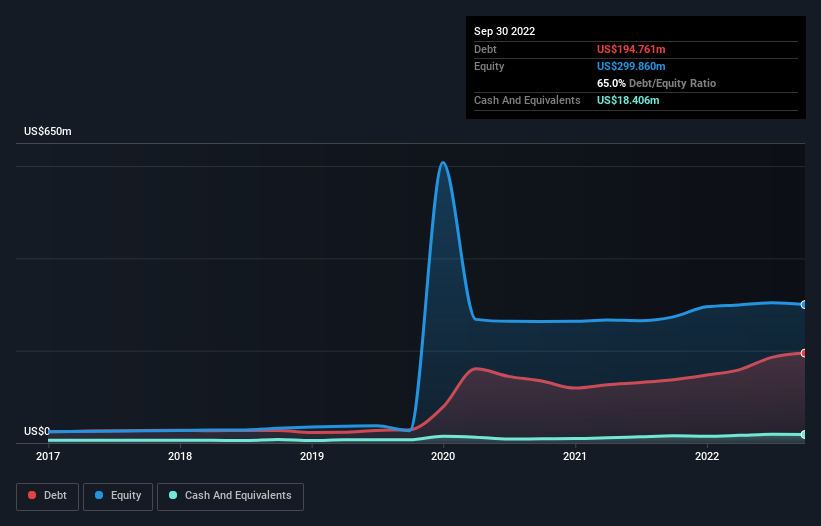

The image below, which you can click on for greater detail, shows that at September 2022 HF Foods Group had debt of US$194.8m, up from US$137.2m in one year. On the flip side, it has US$18.4m in cash leading to net debt of about US$176.4m.

How Strong Is HF Foods Group's Balance Sheet?

The latest balance sheet data shows that HF Foods Group had liabilities of US$168.9m due within a year, and liabilities of US$181.9m falling due after that. Offsetting these obligations, it had cash of US$18.4m as well as receivables valued at US$44.7m due within 12 months. So it has liabilities totalling US$287.7m more than its cash and near-term receivables, combined.

When you consider that this deficiency exceeds the company's US$231.5m market capitalization, you might well be inclined to review the balance sheet intently. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

HF Foods Group's debt is 3.6 times its EBITDA, and its EBIT cover its interest expense 4.5 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. It is well worth noting that HF Foods Group's EBIT shot up like bamboo after rain, gaining 51% in the last twelve months. That'll make it easier to manage its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is HF Foods Group's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Looking at the most recent two years, HF Foods Group recorded free cash flow of 42% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

HF Foods Group's level of total liabilities and net debt to EBITDA definitely weigh on it, in our esteem. But its EBIT growth rate tells a very different story, and suggests some resilience. Taking the abovementioned factors together we do think HF Foods Group's debt poses some risks to the business. While that debt can boost returns, we think the company has enough leverage now. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that HF Foods Group is showing 4 warning signs in our investment analysis , and 1 of those can't be ignored...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if HF Foods Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:HFFG

HF Foods Group

Operates as a marketer and distributor of specialty food products, seafood, fresh produce, frozen and dry food, and non-food products to Asian restaurants and other foodservice customers in the United States.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.1% undervalued

TI

Community Contributor