Advertisement

- United States

- /

- Luxury

- /

- NasdaqCM:JRSH

Jerash Holdings (US), Inc. Just Missed Earnings With A Surprise Loss - Here Are Analysts Latest Forecasts

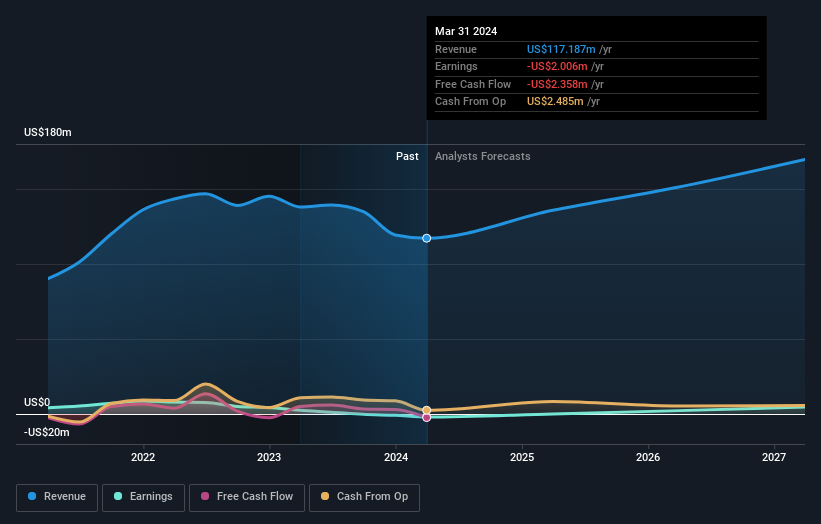

As you might know, Jerash Holdings (US), Inc. (NASDAQ:JRSH) recently reported its annual numbers. Revenues came in at US$117m, in line with estimates, while Jerash Holdings (US) reported a statutory loss of US$0.16 per share, well short of prior analyst forecasts for a profit. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

Check out our latest analysis for Jerash Holdings (US)

After the latest results, the dual analysts covering Jerash Holdings (US) are now predicting revenues of US$135.8m in 2025. If met, this would reflect a decent 16% improvement in revenue compared to the last 12 months. In the lead-up to this report, the analysts had been modelling revenues of US$127.2m and earnings per share (EPS) of US$0.18 in 2025. While next year's revenue estimates increased, there was also a EPS expectations, suggesting the consensus has a bit of a mixed view of these results.

The average price target fell 10.0% to US$4.50, withthe analysts clearly having become less optimistic about Jerash Holdings (US)'sprospects following its latest earnings.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Jerash Holdings (US)'s past performance and to peers in the same industry. It's clear from the latest estimates that Jerash Holdings (US)'s rate of growth is expected to accelerate meaningfully, with the forecast 16% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 11% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 6.2% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that Jerash Holdings (US) is expected to grow much faster than its industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Jerash Holdings (US). Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Jerash Holdings (US)'s future valuation.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At least one analyst has provided forecasts out to 2027, which can be seen for free on our platform here.

And what about risks? Every company has them, and we've spotted 2 warning signs for Jerash Holdings (US) (of which 1 can't be ignored!) you should know about.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:JRSH

Jerash Holdings (US)

Through its subsidiaries, manufactures and exports customized, ready-made sportswear, and outerwear through knitted fabrics.

Moderate growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

930 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative