Stock Analysis

- United States

- /

- Commercial Services

- /

- NasdaqGS:SRCL

Returns On Capital At Stericycle (NASDAQ:SRCL) Paint A Concerning Picture

To avoid investing in a business that's in decline, there's a few financial metrics that can provide early indications of aging. Typically, we'll see the trend of both return on capital employed (ROCE) declining and this usually coincides with a decreasing amount of capital employed. This indicates to us that the business is not only shrinking the size of its net assets, but its returns are falling as well. In light of that, from a first glance at Stericycle (NASDAQ:SRCL), we've spotted some signs that it could be struggling, so let's investigate.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Stericycle:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

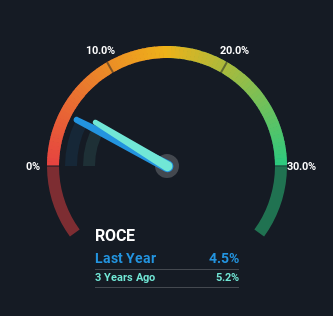

0.045 = US$207m ÷ (US$5.2b - US$650m) (Based on the trailing twelve months to September 2023).

Thus, Stericycle has an ROCE of 4.5%. Ultimately, that's a low return and it under-performs the Commercial Services industry average of 9.6%.

See our latest analysis for Stericycle

In the above chart we have measured Stericycle's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

So How Is Stericycle's ROCE Trending?

The trend of returns that Stericycle is generating are raising some concerns. Unfortunately, returns have declined substantially over the last five years to the 4.5% we see today. What's equally concerning is that the amount of capital deployed in the business has shrunk by 25% over that same period. The combination of lower ROCE and less capital employed can indicate that a business is likely to be facing some competitive headwinds or seeing an erosion to its moat. Typically businesses that exhibit these characteristics aren't the ones that tend to multiply over the long term, because statistically speaking, they've already gone through the growth phase of their life cycle.

In Conclusion...

To see Stericycle reducing the capital employed in the business in tandem with diminishing returns, is concerning. Investors must expect better things on the horizon though because the stock has risen 12% in the last five years. Either way, we aren't huge fans of the current trends and so with that we think you might find better investments elsewhere.

One more thing, we've spotted 1 warning sign facing Stericycle that you might find interesting.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Valuation is complex, but we're helping make it simple.

Find out whether Stericycle is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:SRCL

Stericycle

Stericycle, Inc., together with its subsidiaries, provides regulated waste and compliance services in the United States, Europe, and internationally.

Good value with moderate growth potential.