Advertisement

- United States

- /

- Professional Services

- /

- NasdaqGS:HURN

Why Huron Consulting Group (HURN) Is Up 7.4% After Raising Full-Year Outlook on Record Q3 Results

Simply Wall St

Reviewed by Sasha Jovanovic

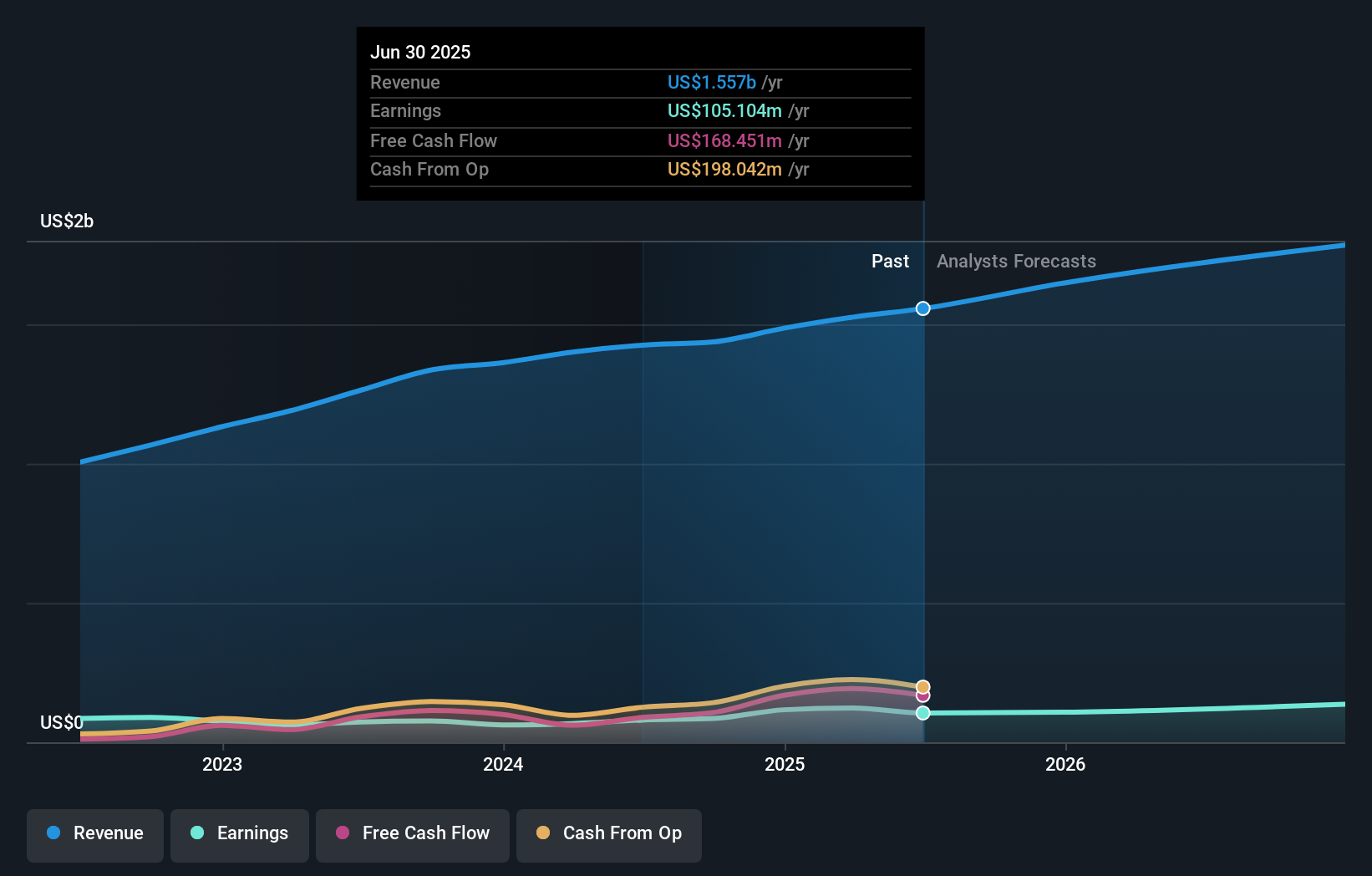

- Huron Consulting Group reported record third-quarter 2025 results, with revenues rising to US$441.28 million and net income increasing to US$30.42 million, while also raising its full-year adjusted earnings guidance and narrowing revenue expectations to a range of US$1.65–1.67 billion.

- These results were driven by strong growth across Healthcare, Education, and Commercial segments and supported by recent acquisitions and expanding digital transformation and managed services offerings.

- We’ll explore how Huron’s raised full-year adjusted earnings outlook impacts the company’s long-term investment narrative.

These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Huron Consulting Group Investment Narrative Recap

To be a Huron Consulting Group shareholder, you need to believe in its ability to grow through client demand for specialized consulting, especially in healthcare, education, and digital transformation. The recent record quarter and upgraded earnings guidance support this view, reinforcing the immediate catalyst of strong project pipelines, but rising compensation and integration costs remain the biggest near-term risk. These results are affirming for Huron’s story and may shift focus toward sustained margin performance.

The company’s ongoing share buyback, with nearly 150,000 shares repurchased in the last quarter alone, is the most relevant announcement connected to the strong quarterly results; continued buybacks could reinforce investor confidence in capital discipline and future earnings per share, supporting the same story that underpins Huron’s raised outlook and the catalyst of margin improvement.

On the other hand, investors should be mindful that even as demand surges, rising compensation expense and integration hurdles could ...

Read the full narrative on Huron Consulting Group (it's free!)

Huron Consulting Group's narrative projects $2.0 billion revenue and $172.9 million earnings by 2028. This requires 9.4% yearly revenue growth and a $67.8 million earnings increase from $105.1 million.

Uncover how Huron Consulting Group's forecasts yield a $171.50 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members value Huron between US$171.50 and US$356.61, reflecting two diverse viewpoints. While many expect margin gains to fuel future earnings, consider how operating costs shape sentiment and long-term results.

Explore 2 other fair value estimates on Huron Consulting Group - why the stock might be worth just $171.50!

Build Your Own Huron Consulting Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Huron Consulting Group research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Huron Consulting Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Huron Consulting Group's overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Find companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Huron Consulting Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:HURN

Huron Consulting Group

Provides consultancy and managed services in the United States and internationally.

Good value with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor