Advertisement

- United States

- /

- Commercial Services

- /

- NasdaqGS:CPRT

Will Copart's (CPRT) Shift to Higher-Margin Services Redefine Its Profitability Story?

Simply Wall St

Reviewed by Sasha Jovanovic

- Copart recently reported quarterly earnings, showing 5.25% revenue growth and more than 20% growth in earnings per share, with increasing margins and a shift toward higher-margin service revenue even as vehicle sales declined.

- This highlights Copart’s ability to drive profit growth through operational efficiency and changing revenue mix, even amid softer vehicle auction volumes.

- We’ll explore how Copart’s margin expansion and earnings growth may influence its broader investment narrative and outlook for future profitability.

Find companies with promising cash flow potential yet trading below their fair value.

Copart Investment Narrative Recap

To own Copart, shareholders need to believe in the company’s ability to generate consistent profit growth via operational efficiency and shifting toward higher-margin services, even if auction volumes soften in the near term. The latest quarterly results reinforce this narrative, as rising margins and earnings per share offset declining vehicle sales; however, this does not meaningfully change the biggest short-term catalyst, which remains Copart’s expansion of technology-driven services, or the most important risk, which is a potential slowdown in total loss vehicle supply.

Among recent announcements, Copart’s collaboration with One Inc. to modernize lienholder payments stands out, as it directly supports the expansion of value-added services. This effort could reinforce the company’s push for higher-margin service revenue and strengthen relationships with insurers, a key short-term driver for Copart as it navigates potential volume headwinds.

By contrast, investors should be aware that structural changes in vehicle accident rates could impact the future pool of salvage auction inventory...

Read the full narrative on Copart (it's free!)

Copart's narrative projects $6.4 billion revenue and $2.1 billion earnings by 2028. This requires 11.1% yearly revenue growth and a $0.5 billion earnings increase from $1.6 billion.

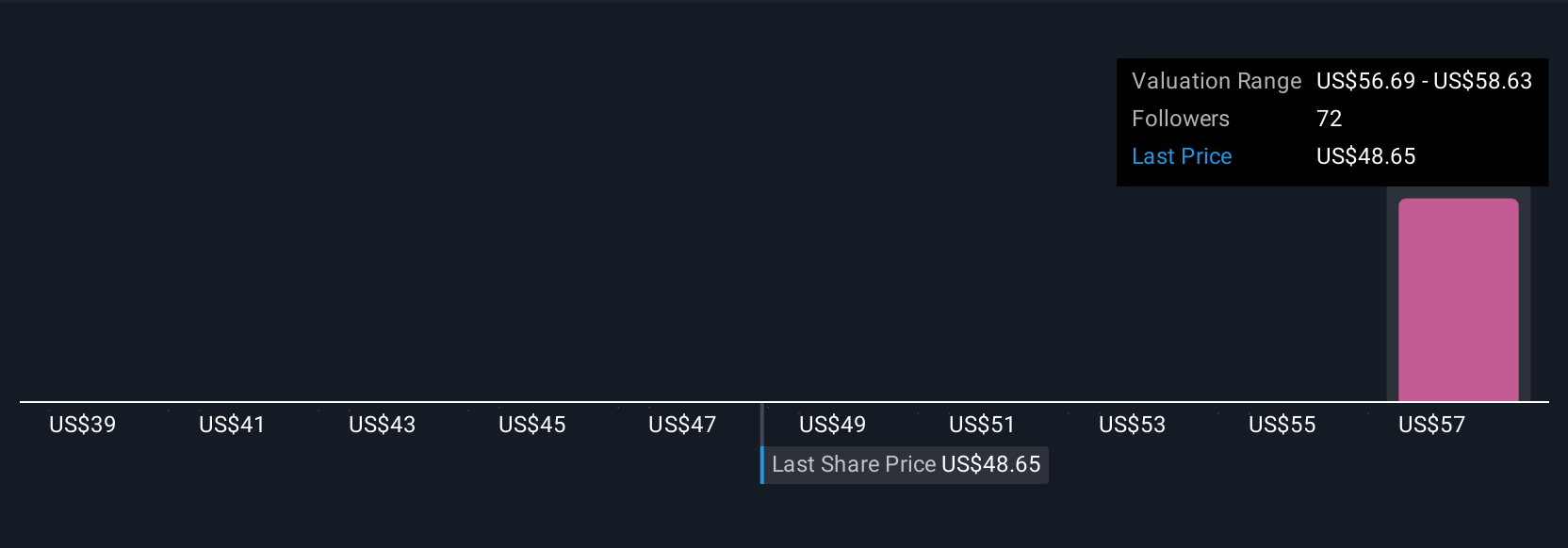

Uncover how Copart's forecasts yield a $56.00 fair value, a 30% upside to its current price.

Exploring Other Perspectives

Twelve members of the Simply Wall St Community put Copart’s fair value between US$39.26 and US$63.08, highlighting broad differences in opinion. With ongoing expansion of value-added services, your outlook on Copart’s growth drivers may align or contrast with others, consider exploring several perspectives before making any investment decisions.

Explore 12 other fair value estimates on Copart - why the stock might be worth 9% less than the current price!

Build Your Own Copart Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Copart research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Copart research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Copart's overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 37 companies in the world exploring or producing it. Find the list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CPRT

Copart

Provides online auctions and vehicle remarketing services in the United States, the United Kingdom, Germany, Brazil, Canada, the United Arab Emirates, Spain, Finland, Oman, the Republic of Ireland, and Bahrain.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor