Advertisement

- United States

- /

- Professional Services

- /

- NasdaqGS:ADP

How Investors Are Reacting To Automatic Data Processing (ADP) Steady Earnings Growth and Russell 1000 Influence

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent days, Automatic Data Processing (NASDAQ:ADP) reported earnings per share growth of 13% per year over the last three years and a 7.1% increase in revenue to US$21 billion, with EBIT margins holding steady and insider ownership valued at US$78 million.

- ADP’s reinforced role in the Russell 1000 index and sustained institutional interest highlight its operational efficiency, technological advancements, and influence within the technology sector.

- Now, we’ll assess how ADP’s consistent revenue growth and strong index presence shape the latest investment narrative for the company.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Automatic Data Processing Investment Narrative Recap

To be a shareholder in Automatic Data Processing, you need to believe in the long-term demand for outsourced, cloud-based HR and payroll solutions as businesses digitize operations. The recent results, showing stable margins and healthy revenue gains, reinforce the view that ADP’s core franchises remain resilient. These updates do not appear to materially affect the key short-term catalyst for ADP, sustaining growth in advanced technology product adoption, nor do they significantly shift the main risk: ongoing competitive pressure and delayed deal closures. Among recent company news, ADP’s product launches, particularly the rollout of ADP® Embedded Payroll for SMB software providers, aligns closely with the company’s growth catalysts. This move supports ADP’s efforts to increase customer lock-in and expand its addressable market through technology adoption, potentially offsetting booking slowdowns or sales cycle delays if widely embraced. Yet, the growing influence of newer, SaaS-native competitors could lead to an acceleration in pricing pressure and pipeline delays, which investors should be aware of as...

Read the full narrative on Automatic Data Processing (it's free!)

Automatic Data Processing is projected to reach $24.3 billion in revenue and $5.1 billion in earnings by 2028. This outlook depends on a 5.7% annual revenue growth rate and a $1.0 billion increase in earnings from the current level of $4.1 billion.

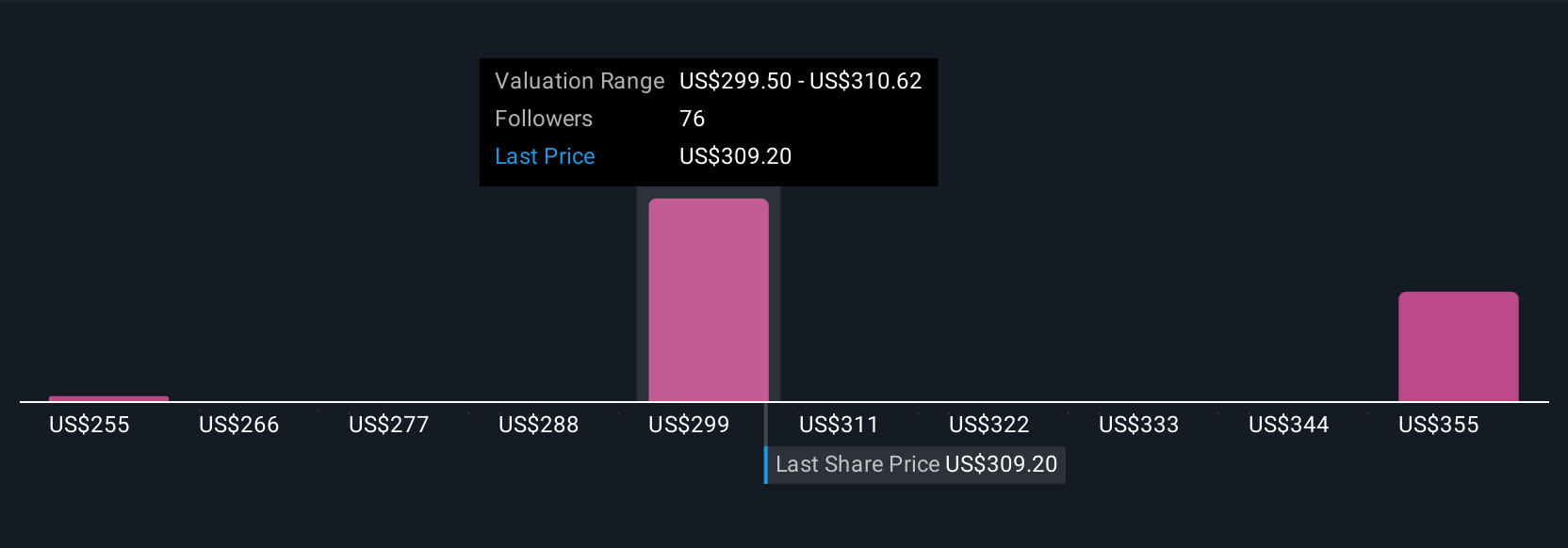

Uncover how Automatic Data Processing's forecasts yield a $314.17 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Private fair value estimates from eight Simply Wall St Community members for ADP range widely from US$235 to US$387 per share. With deal cycle delays posing a real risk, you may want to review how others see pressure points shaping future results.

Explore 8 other fair value estimates on Automatic Data Processing - why the stock might be worth 17% less than the current price!

Build Your Own Automatic Data Processing Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Automatic Data Processing research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Automatic Data Processing research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Automatic Data Processing's overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find companies with promising cash flow potential yet trading below their fair value.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ADP

Automatic Data Processing

Provides cloud-based human capital management (HCM) solutions worldwide.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

TA

Talos on Tesla ·

The "Physical AI" Monopoly – A New Industrial Revolution

Fair Value:US$665.3637.3% undervalued

35 followersusers have followed this narrative

14 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

Marek_Trnka on CSG ·

Czechoslovak Group - is it really so hot?

Fair Value:€5548.6% undervalued

38 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

AL

alex30free on Swedencare ·

The Compound Effect: From Acquisition to Integration

Fair Value:SEK 46.2846.8% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

DO

Double_Bubbler on Spectral AI ·

Spectral AI: First of Its Kind Automated Wound Healing Prediction

Fair Value:US$569.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DO

Double_Bubbler on EnSilica ·

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value:UK£590.1% undervalued

113 followersusers have followed this narrative

17 commentsusers have commented on this narrative

0 likesusers have liked this narrative

QU

Quant_Trader on SoFi Technologies ·

SoFi Technologies will ride a 33% revenue growth wave in the next 5 years

Fair Value:US$39.9851.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.886.3% undervalued

58 followersusers have followed this narrative

5 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.7% undervalued

1072 followersusers have followed this narrative

6 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$603.2233.5% undervalued

1272 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

US

User on Tesla ·

When was the last time that Tesla delivered on its promises? Lets go through the list! The last successful would be the Tesla Model 3 which was 2019 with first deliveries 2017. Roadster not shipped. Tesla Cybertruck global roll out failed. They might have a bunch of prototypes (that are being controlled remotely) And you think they'll be able to ship something as complicated as a robot? It's a pure speculation buy.

3

|1

US

User on Tesla ·

This article completely disregards (ignores, forgets) how far China is in this field. If Tesla continues on this path, they will be fighting for their lives trying to sell $40000 dollar robots that can do less than a $10000 dollar one from China will do. Fair value of Tesla? It has always been a hype stock with a valuation completely unbased in reality. Your guess is as good as mine, but especially after the carbon credit scheme got canned, it is downwards of $150.

2

|0

US

User on Tesla ·

It was crazy to start a capital intensive car company from scratch having cars run on batteries. It was crazy to start a captial intensive space company. It was crazy to think you could launch 1000s of satelites and provide internet coverage anywhere in the world. It was crazy to imagine a car direct off the assembly line could drive itself (mine does and nobody is controlling it). It's crazy to think that a single $17 share of tesla stock at IPO is worth $6, 378 today. There is a big difference between a company that doesn't promise anything new or groundbreaking and meets expectations and a company that promises things that seem crazy and delivers them late. I'm happy to invest in the later.

2

|1