Watts Water Technologies (WTS) shares have pulled back about 2% over the past month, even as the company’s returns this year remain strong. Investors may be weighing recent performance alongside steady growth in annual revenue and net income.

Watts Water Technologies has climbed steadily in 2024, with a 36% year-to-date share price return and a robust 44% total shareholder return over the past year. This highlights real long-term momentum. While shares have eased slightly in recent weeks, investors seem to be recalibrating after substantial multi-year gains and strong financial growth.

With Watts shares hovering near their recent highs and growth metrics remaining healthy, the key question now is whether the current price reflects all that future momentum or if investors still have a buying opportunity.

Advertisement

Most Popular Narrative: Fairly Valued

Watts Water Technologies’ most followed narrative points to a fair value of $277.80, almost identical to the recent closing price of $273.07, highlighting a market consensus that the stock is currently priced about right. This sets the stage for a closer look at what’s driving analyst conviction about Watts’ future earnings and market opportunity.

The accelerating rollout and success of Nexa, Watts' intelligent water management platform, positions the company to capture the growing demand for advanced, data-driven water conservation, efficiency, and regulatory compliance solutions. This is expected to drive higher-margin, recurring revenue and support long-term earnings and margin expansion.

Curious what assumptions drive this razor-thin fair value margin? The narrative’s ultra-optimistic earnings outlook hinges on digital innovation, margin expansion, and aggressive growth forecasts. But what’s the catch behind these aggressive numbers? Dive in to see the details shaping this razor's edge valuation call.

However, persistent European market weakness or slower adoption of smart water technologies could quickly challenge the current optimism and lead analysts to reassess their outlooks.

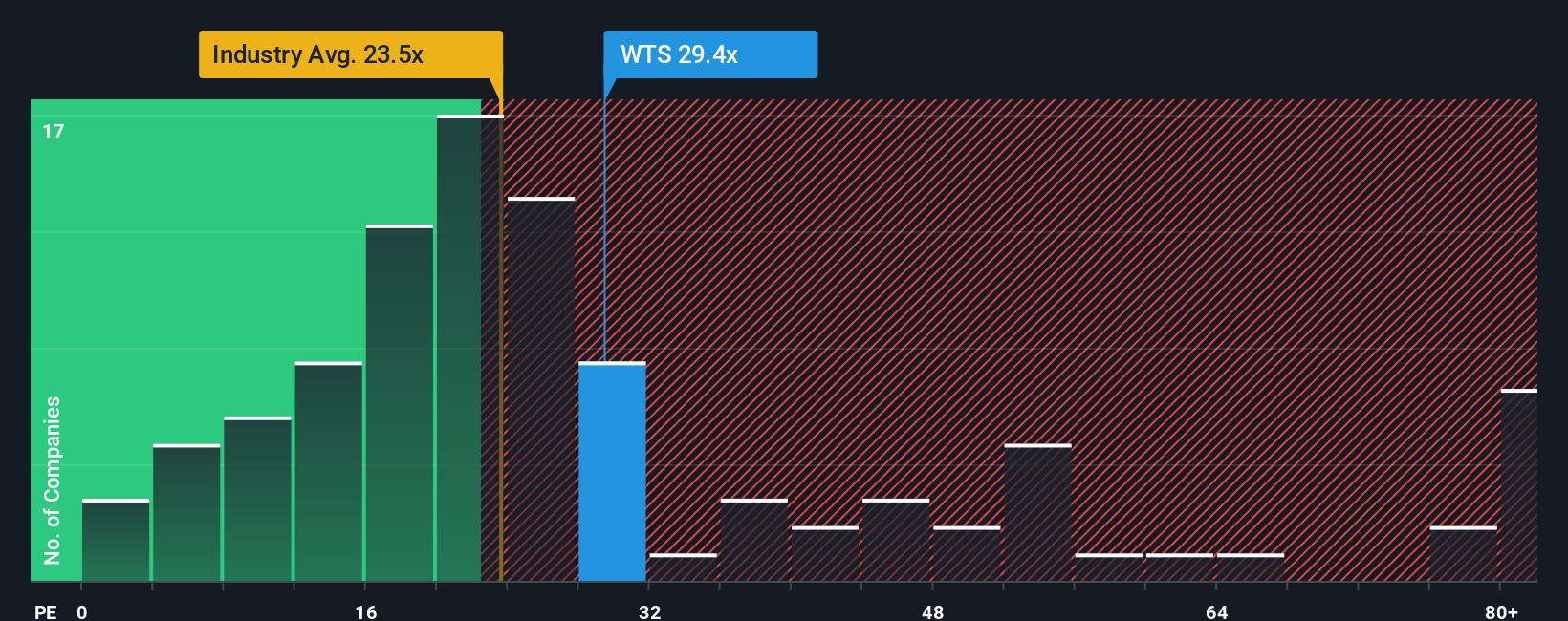

While consensus points to fair value, looking at company valuation through a price-to-earnings lens raises questions. Watts trades at 29.2x earnings, noticeably higher than both the industry average of 24.6x and the peer average of 28.7x. The fair ratio, which could be the level the market moves toward, is just 21.1x. This premium signals the market expects outsized growth or rewards quality. However, it may also set a higher bar for future performance.

If you prefer to analyze the numbers yourself or want to chart a different story, it’s easy to build your own perspective in just minutes, and Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Watts Water Technologies.

Looking for More Smart Investment Ideas?

If you want an edge in the market, don't wait for tomorrow's headlines. Tap into new trends right now using the Simply Wall Street Screener. Smart investors make the first move, not the last!

Catalyze your growth strategy and seize the momentum with these 26 AI penny stocks, featuring picks at the intersection of artificial intelligence innovation and rapid financial upside.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Watts Water Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Supplies systems, products and solutions that manage and conserve the flow of fluids and energy into, though, and out of buildings in the commercial, industrial, and residential markets in the Americas, Europe, the Asia-Pacific, the Middle East, and Africa.