Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:TDG

Evaluating TransDigm Group’s Valuation Following Strong Earnings and 2026 Guidance Update

Simply Wall St

Reviewed by Simply Wall St

TransDigm Group (NYSE:TDG) caught investors’ eyes following its latest quarterly and annual earnings update. Sales and net income climbed for fiscal 2025, with management issuing fresh 2026 guidance. The outlook highlights ongoing growth but also some margin pressures.

See our latest analysis for TransDigm Group.

TransDigm shares have gained fresh momentum following upbeat earnings and new guidance. After some recent choppiness, the 1-year total shareholder return sits at 15.5%, with longer-term investors also enjoying outstanding three- and five-year returns. Ongoing buybacks and robust 2025 results appear to be shifting sentiment back toward growth potential, even as the outlook acknowledges some profit pressures ahead.

If TransDigm’s resilience has you rethinking your watchlist, now’s the perfect time to discover See the full list for free.

So with TransDigm’s solid results and a new price target well above current levels, this raises the question: is there room for more upside, or have recent gains already accounted for the company’s future growth prospects?

Most Popular Narrative: 13.3% Undervalued

TransDigm Group’s most widely followed narrative places fair value above the latest closing price, suggesting room for upside from these levels. The narrative’s calculation incorporates sector trends alongside future earnings and margin projections, giving investors a bullish sense of the company’s forward prospects compared to its current valuation.

The growing age of the global aircraft fleet, combined with heightened airline investment in refurbishments and mandatory regulatory maintenance, is increasing the need for proprietary replacement parts, positively impacting TransDigm's high-margin aftermarket revenues and supporting continued margin expansion.

How high are analysts betting on those margins? One driver behind this compelling valuation: ambitious growth for both profits and sales, paired with a bold premium multiple. There is a lot going on behind these numbers. Find out which assumption really tips the scale by reading the full narrative.

Result: Fair Value of $1,557.89 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, growing regulatory pressures and TransDigm’s heavy reliance on legacy aftermarket revenues could challenge its growth story if market dynamics shift suddenly.

Find out about the key risks to this TransDigm Group narrative.

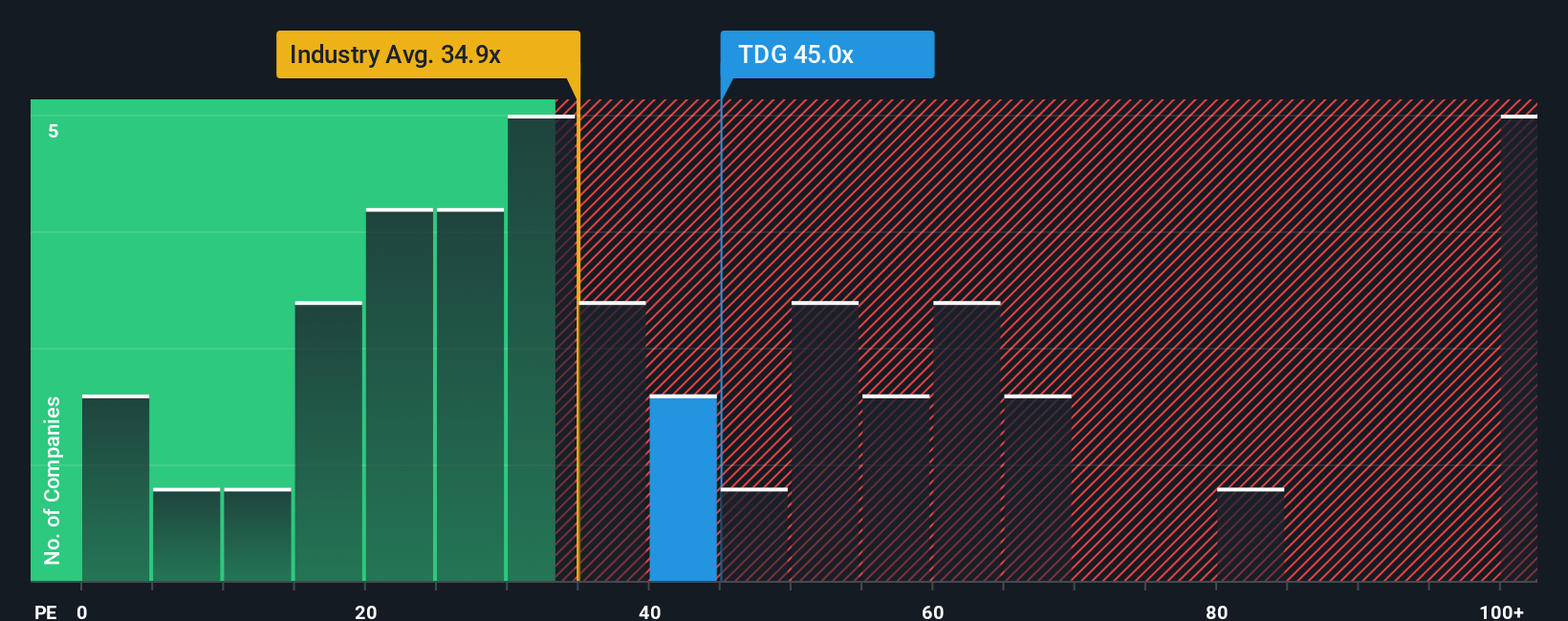

Another View: Multiples Paint a Costly Picture

Looking beyond fair value estimates, TransDigm’s current price-to-earnings ratio stands at 40.8 times, which is notably higher than the industry average of 37.7 times and well above the fair ratio of 33.4 times. This premium signals investors are already factoring in a strong future. However, it could also mean increased valuation risk if growth disappoints.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own TransDigm Group Narrative

If you want a fresh perspective or would rather investigate the numbers your own way, it takes just minutes to build a personal narrative. Do it your way.

A great starting point for your TransDigm Group research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t let opportunity pass you by. Discover standout stocks and themes beyond TransDigm with the Simply Wall Street Screener for your next strategic move.

- Start building long-term wealth by exploring these 18 dividend stocks with yields > 3%, a selection of stocks that offer generous yields and reliable passive income potential.

- Harness the potential of next-generation breakthroughs with these 27 AI penny stocks, featuring innovators who are transforming industries with artificial intelligence.

- Take advantage of market mispricings with these 900 undervalued stocks based on cash flows, which highlights stocks trading below intrinsic value for growth-minded investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TransDigm Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TDG

TransDigm Group

Designs, produces, and supplies aircraft components in the United States and internationally.

Acceptable track record with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor