Advertisement

- United States

- /

- Machinery

- /

- NYSE:MLI

Mueller Industries (MLI): Assessing Valuation After Strong 12% Monthly Share Price Gain

Simply Wall St

Reviewed by Simply Wall St

Mueller Industries (MLI) has caught the eye of investors recently, as the company's stock continues to advance. Over the past month, shares have climbed 12%, adding to a strong streak of returns throughout the year.

See our latest analysis for Mueller Industries.

The latest rally builds on a remarkable run for Mueller Industries, with a 35.8% year-to-date share price return and a five-year total shareholder return of nearly 590%. This kind of sustained momentum signals growing confidence in the company’s future prospects.

If you’re interested in discovering other companies with a track record of growth and strong insider support, broaden your search and see what you find in the fast growing stocks with high insider ownership.

But with such impressive gains already logged, the key question is whether Mueller Industries is still trading below its true value or if the market has already fully priced in its future growth potential.

Price-to-Earnings of 16x: Is it justified?

Mueller Industries is valued at a price-to-earnings (P/E) multiple of 16x, noticeably below the US market average and the industry standard, based on the most recent closing price of $108.28. This suggests the market may be placing a discount on expected earnings relative to competitors.

The price-to-earnings ratio compares the company’s share price with its earnings per share. It is a quick reference for how investors are pricing the firm’s future profitability. For a mature business in the capital goods sector, a reasonable P/E points to what the market anticipates for steady earnings growth ahead.

What stands out is that Mueller Industries’ P/E of 16x is not only lower than the US market at 18.2x, but also well below the industry average of 24x and its own estimated fair P/E of 20.5x. The market could be underestimating the company’s earning power or overlooking its recent acceleration in profit growth and high return on equity.

The gap between the current and fair P/E suggests a level where the market could potentially re-rate the shares if expectations shift. Explore the SWS fair ratio for Mueller Industries

Result: Price-to-Earnings of 16x (UNDERVALUED)

However, slower revenue and net income growth compared to peers could challenge the current momentum and make ongoing outperformance harder to sustain.

Find out about the key risks to this Mueller Industries narrative.

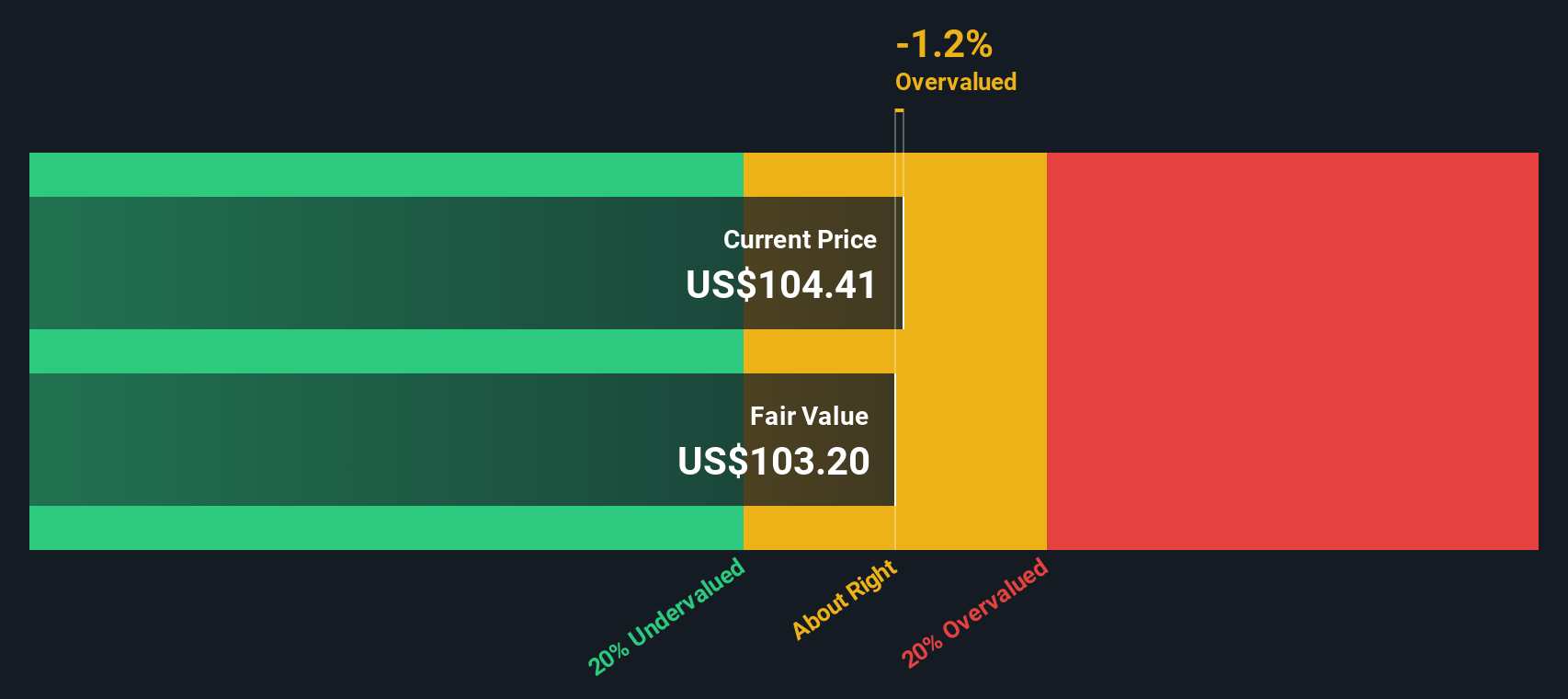

Another View: Discounted Cash Flow Analysis

While the price-to-earnings ratio points to undervaluation, our SWS DCF model offers a more cautious take. According to this method, Mueller Industries' share price is currently above the estimated fair value, which suggests the stock may be slightly overvalued on a cash flow basis.

Look into how the SWS DCF model arrives at its fair value.

With these two valuation methods pointing in different directions, are investors leaning on recent momentum or could the fundamentals prompt a shift in sentiment?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Mueller Industries for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 855 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Mueller Industries Narrative

Keep in mind, if you have a different perspective or want to dive deeper on your own, you can put together your own view in just a few minutes. Do it your way.

A great starting point for your Mueller Industries research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Winning Investment Ideas?

Seize the advantage by tapping into stock ideas that could transform your portfolio. The right screener reveals hidden gems. Don’t watch from the sidelines when opportunities are out there to be acted on.

- Capitalize on the future of healthcare by checking out these 32 healthcare AI stocks, delivering breakthroughs at the intersection of medicine and artificial intelligence.

- Boost your potential income stream with these 15 dividend stocks with yields > 3%, offering attractive yields above 3% to strengthen your returns.

- Position yourself at the forefront of innovation with these 27 quantum computing stocks, driving the next leaps in computing and technology applications.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MLI

Mueller Industries

Manufactures and sells copper, brass, and aluminum products in the United States, the United Kingdom, Canada, Asia and the Middle East, and Mexico.

Outstanding track record with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor