Advertisement

- United States

- /

- Building

- /

- NYSE:BLDR

Is Builders FirstSource’s Cautious Outlook and Efficiency Focus Reshaping the BLDR Investment Case?

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this week, Builders FirstSource reported a 5% year-on-year revenue decline and issued weaker-than-expected full-year revenue and EBITDA guidance, missing analyst forecasts.

- The company’s update highlighted a sharp contrast with industry peers, as it provided the most cautious full-year outlook among home construction materials suppliers and is intensifying efforts to improve technology and efficiency amid these pressures.

- We’ll explore how Builders FirstSource’s weaker full-year outlook and focus on operational efficiency may affect its investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Builders FirstSource Investment Narrative Recap

For investors to remain confident in Builders FirstSource, they need to believe the company can leverage digital investments and operational efficiencies to weather ongoing weakness in housing starts and volatile construction demand. The recently lowered revenue and EBITDA guidance may weaken the near-term catalyst of a housing rebound, while exposing the business to heightened risk from persistent demand softness and margin pressures; if these headwinds persist, the impact could be material for the company’s recovery trajectory.

One of the most relevant recent announcements is Builders FirstSource’s acquisition of Builder's Door & Trim and Rystin Construction in Las Vegas, extending its footprint and boosting value-added offerings. This move directly ties to the company’s efforts to diversify revenue streams and enhance margin opportunities, which should be viewed in context with the current pressures on its core markets and the need to deliver on promised technology-driven growth.

By contrast, ongoing unpredictability in single-family housing starts remains a risk that investors should keep front of mind as...

Read the full narrative on Builders FirstSource (it's free!)

Builders FirstSource's outlook anticipates $16.4 billion in revenue and $684.5 million in earnings by 2028. This scenario implies a -0.9% annual revenue decline and a $71.9 million decrease in earnings from the current $756.4 million.

Uncover how Builders FirstSource's forecasts yield a $140.32 fair value, a 13% upside to its current price.

Exploring Other Perspectives

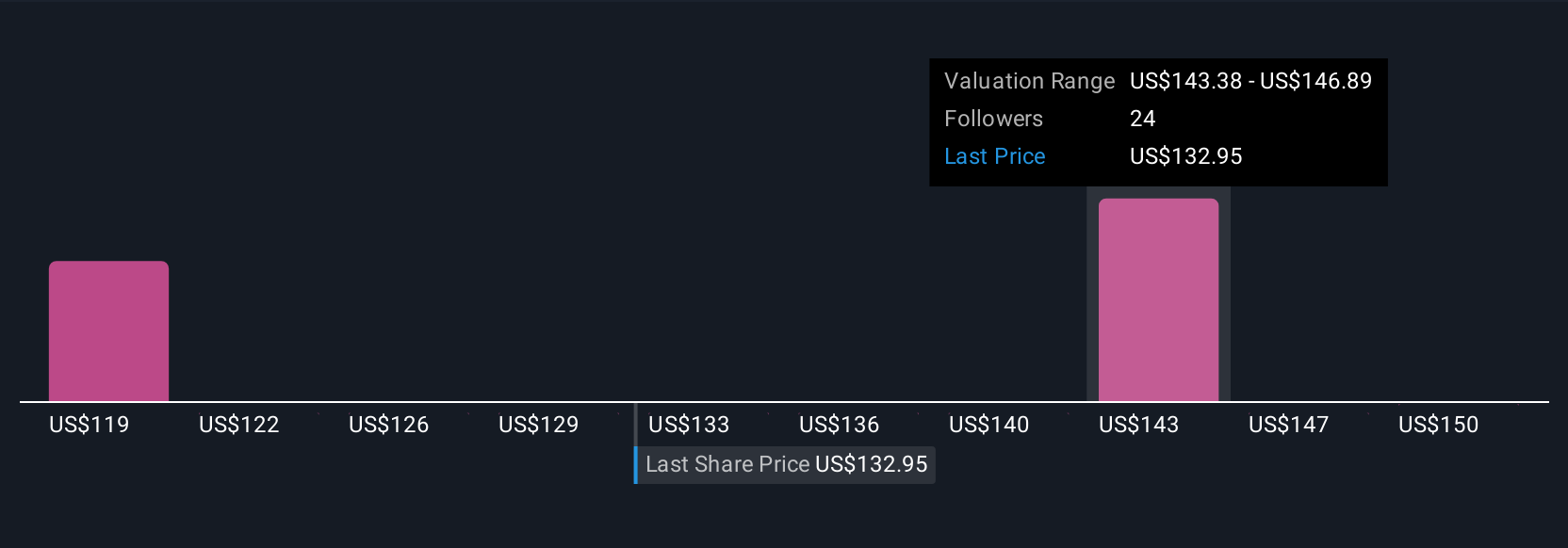

Two recent fair value estimates from the Simply Wall St Community range between US$118.72 and US$140.32 per share. While some see upside potential, persistent softness in single-family starts continues to weigh on the company’s outlook, so consider how these different viewpoints might fit your own expectations.

Explore 2 other fair value estimates on Builders FirstSource - why the stock might be worth just $118.72!

Build Your Own Builders FirstSource Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Builders FirstSource research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Builders FirstSource research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Builders FirstSource's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Builders FirstSource might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BLDR

Builders FirstSource

Manufactures and supplies building materials, manufactured components, and construction services to professional homebuilders, sub-contractors, remodelers, and consumers in the United States.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor