Advertisement

The analysts covering AECOM (NYSE:ACM) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. This report focused on revenue estimates, and it looks as though the consensus view of the business has become substantially more conservative.

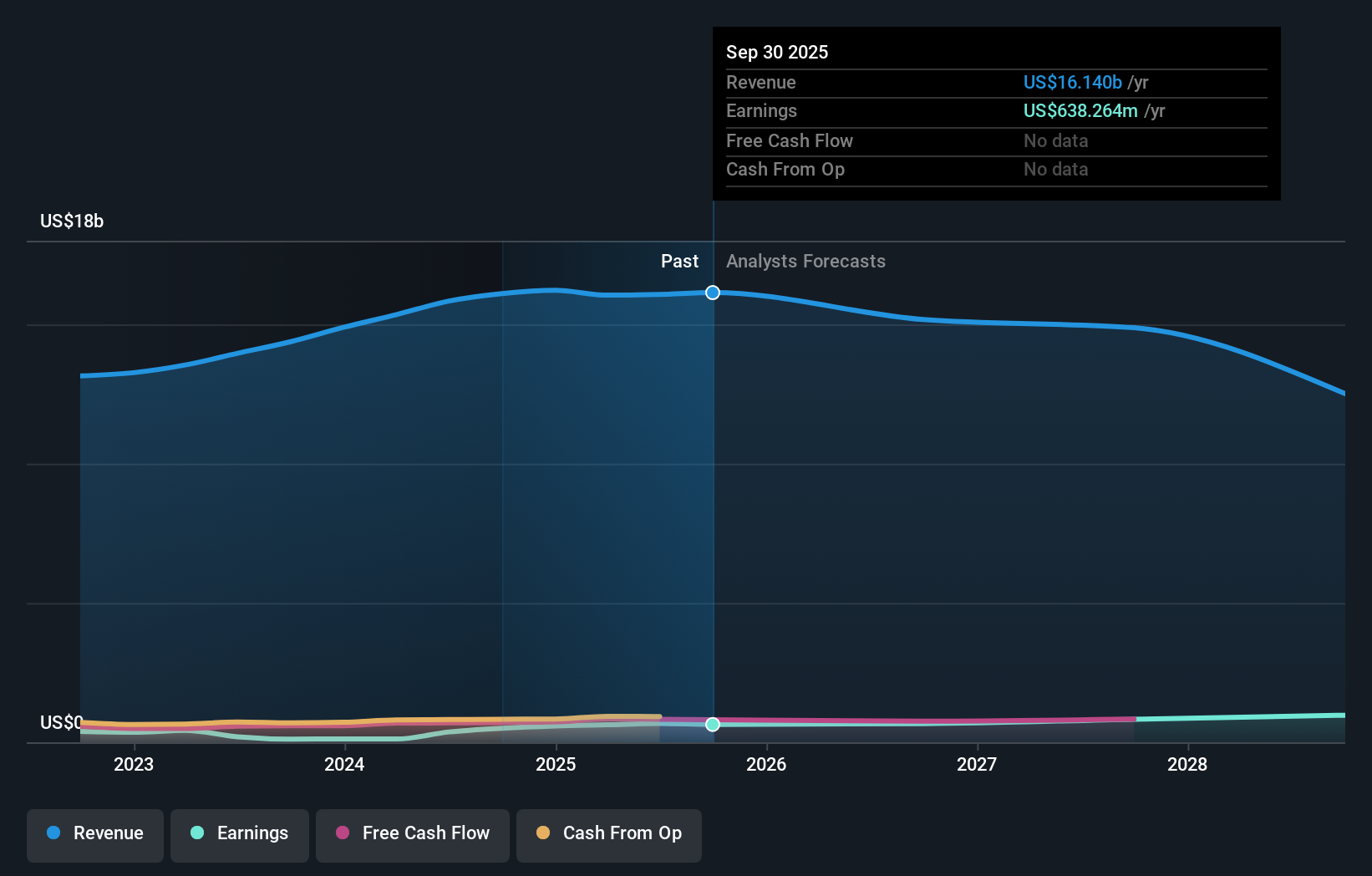

Following the latest downgrade, the seven analysts covering AECOM provided consensus estimates of US$15b revenue in 2026, which would reflect a measurable 6.0% decline on its sales over the past 12 months. Per-share earnings are expected to increase 8.6% to US$5.24. Previously, the analysts had been modelling revenues of US$17b and earnings per share (EPS) of US$5.71 in 2026. Indeed, we can see that analyst sentiment has declined measurably after the new consensus came out, with a measurable cut to revenue estimates and a minor downgrade to EPS estimates to boot.

View our latest analysis for AECOM

Despite the cuts to forecast earnings, there was no real change to the US$143 price target, showing that the analysts don't think the changes have a meaningful impact on its intrinsic value.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We would highlight that sales are expected to reverse, with a forecast 6.0% annualised revenue decline to the end of 2026. That is a notable change from historical growth of 5.1% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 9.1% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - AECOM is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. Overall, given the drastic downgrade to this year's forecasts, we'd be feeling a little more wary of AECOM going forwards.

A high debt burden combined with a downgrade of this magnitude always gives us some reason for concern, especially if these forecasts are just the first sign of a business downturn. See why we're concerned about AECOM's balance sheet by visiting our risks dashboard for free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:ACM

AECOM

Provides professional infrastructure consulting services for governments, businesses, and organizations internationally.

Solid track record and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor