Advertisement

- United States

- /

- Electrical

- /

- NasdaqGS:POWL

Will AI-Driven Utility Growth Offset Powell Industries’ (POWL) Slower Order Intake Over Time?

Simply Wall St

Reviewed by Sasha Jovanovic

- Powell Industries recently reported its fourth quarter and full-year earnings for Fiscal 2025, with quarterly sales of US$297.98 million and net income of US$51.42 million, both higher than the prior year.

- An interesting detail is that the company’s Electric Utility segment, supported by increasing AI data center investments, grew significantly over the past year, balancing a drop in quarterly order intake.

- We’ll explore how robust Electric Utility growth, despite declining new orders, could shape the company’s investment outlook going forward.

These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Powell Industries Investment Narrative Recap

To be a Powell Industries shareholder today, you need confidence that robust demand in electric utility infrastructure, especially thanks to AI-driven data center investments, will offset recent weakness in order intake and help sustain both revenue and profit momentum. The latest earnings show continued strength in the Electric Utility segment, but the pronounced drop in quarterly orders introduces a material risk: if underlying demand continues to slow, it could quickly challenge current margin strength and investor expectations for growth.

Among recent company announcements, the acquisition of Remsdaq Ltd. stands out. This move should broaden Powell’s capabilities in electrical automation and SCADA solutions, directly tying into investor hopes for accelerating revenue and margin growth as the utility sector remains an important catalyst for future performance.

Yet in contrast, investors should also be aware that recent margin gains have benefited from one-off events that may not recur, and when new order flow slows, sustained high margins could be harder to maintain...

Read the full narrative on Powell Industries (it's free!)

Powell Industries is projected to reach $1.3 billion in revenue and $169.4 million in earnings by 2028. This outlook assumes annual revenue growth of 5.7%, but earnings are expected to decrease by $6 million from the current $175.4 million.

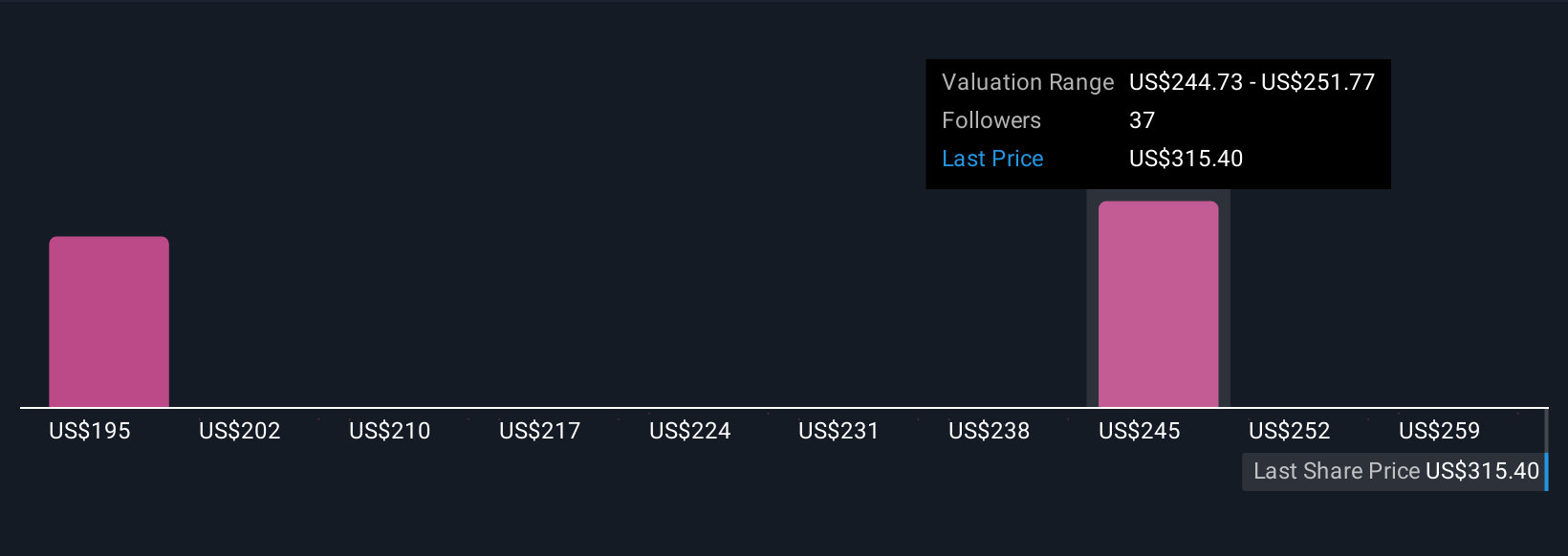

Uncover how Powell Industries' forecasts yield a $269.26 fair value, a 5% downside to its current price.

Exploring Other Perspectives

Simply Wall St Community members supplied four fair value estimates for Powell Industries ranging from US$191.56 to US$269.26 per share. Several see upside, but with the risk of margin normalization as one of the biggest watchpoints, your view can differ sharply from the consensus.

Explore 4 other fair value estimates on Powell Industries - why the stock might be worth as much as $269.26!

Build Your Own Powell Industries Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Powell Industries research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Powell Industries research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Powell Industries' overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:POWL

Powell Industries

Designs, develops, manufactures, sells, and services custom-engineered equipment and systems.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor