Stock Analysis

As global markets navigate through a landscape marked by trade tensions and shifting investment trends towards value and small-cap shares, investors are continually adapting their strategies to align with the evolving economic environment. In this context, growth companies with high insider ownership can offer unique advantages, as these insiders often have a deep commitment to the company's long-term success, which may be particularly appealing during uncertain market conditions.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Medley (TSE:4480) | 34% | 28.7% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 36.4% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 13.6% | 26.8% |

| Global Tax Free (KOSDAQ:A204620) | 18.1% | 72.4% |

| Seojin SystemLtd (KOSDAQ:A178320) | 29.8% | 58.7% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.4% | 60.9% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

| UTI (KOSDAQ:A179900) | 33.1% | 122.7% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 74.3% |

| HANA Micron (KOSDAQ:A067310) | 20% | 96.6% |

Let's review some notable picks from our screened stocks.

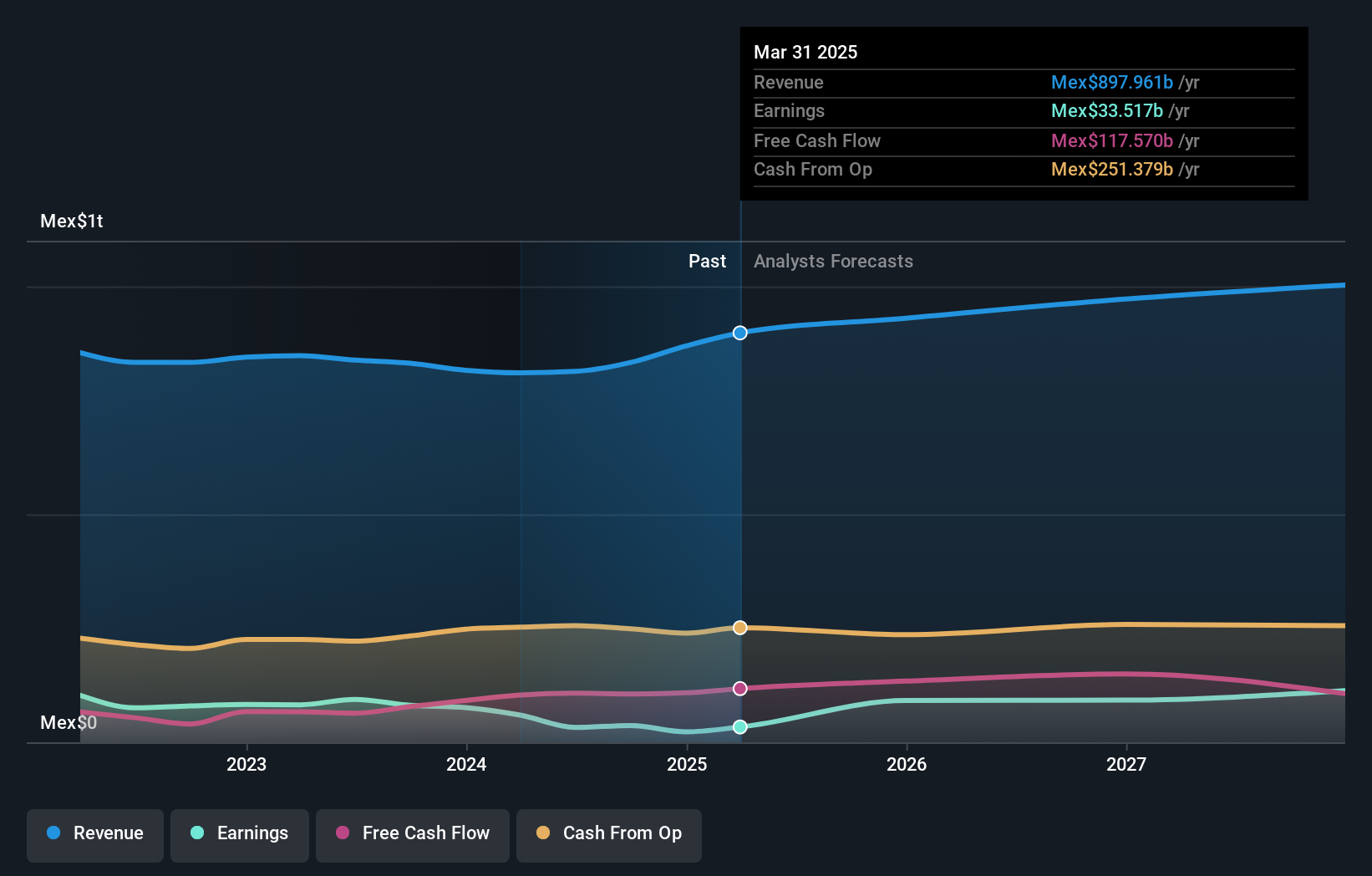

América Móvil. de (BMV:AMX B)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: América Móvil, S.A.B. de C.V. is a telecommunications service provider operating across Latin America and globally, with a market capitalization of approximately MX$969.22 billion.

Operations: The primary revenue source for the company is cellular services, generating MX$813.38 billion.

Insider Ownership: 22.4%

América Móvil has recently faced challenges, with a significant net loss in Q2 2024 contrasting sharply against the previous year's profit. Despite these setbacks, the company is actively buying back shares, having completed repurchases worth MXN 460.37 billion since 2001. Financial forecasts suggest robust long-term earnings growth significantly above market expectations, although revenue growth projections remain modest compared to the broader Mexican market. The firm's financial strategy reflects a mix of aggressive shareholder returns and cautious revenue expansion strategies.

- Delve into the full analysis future growth report here for a deeper understanding of América Móvil. de.

- Our comprehensive valuation report raises the possibility that América Móvil. de is priced lower than what may be justified by its financials.

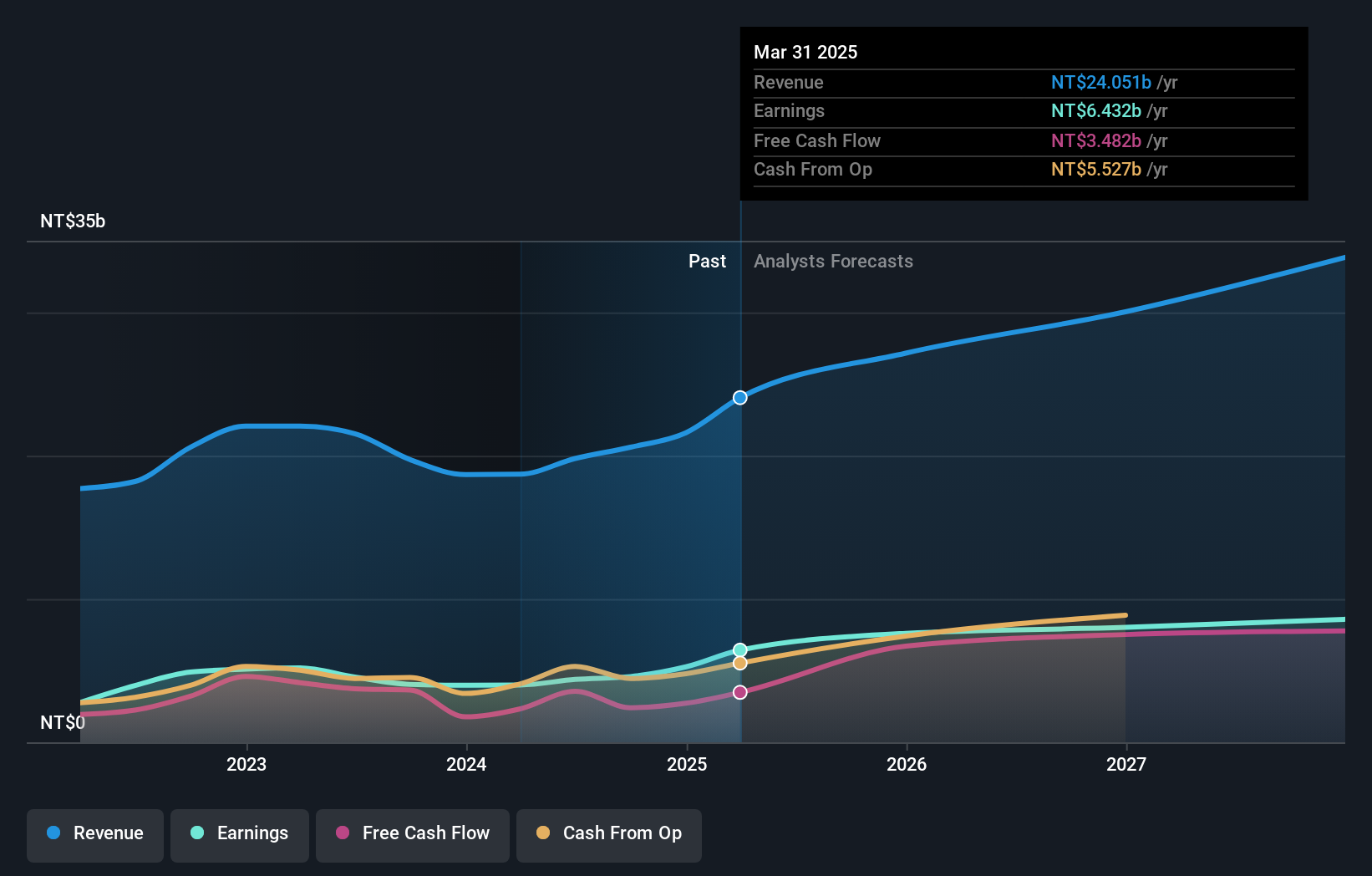

Kinik (TWSE:1560)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Kinik Company, operating both domestically and internationally, specializes in the production and sale of abrasives, cutting tools, and reclaimed wafers, with a market capitalization of NT$48.63 billion.

Operations: The company generates revenue from two primary segments: NT$3.23 billion from the electronics sector and NT$3.19 billion from traditional sectors.

Insider Ownership: 17.5%

Kinik, with its recent robust earnings growth and substantial dividend payouts (TWD 580.08 million), underscores its potential in the high insider ownership segment. The company's earnings surged to TWD 256.69 million in Q1 2024, outpacing last year's figures significantly. Analysts project Kinik’s annual profit to grow by 32.3%, well above Taiwan's market average, complemented by a strong forecast return on equity of 22.6% in three years, indicating efficient management and promising financial health despite trading at a significant discount to its estimated fair value.

- Dive into the specifics of Kinik here with our thorough growth forecast report.

- According our valuation report, there's an indication that Kinik's share price might be on the expensive side.

Chroma ATE (TWSE:2360)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Chroma ATE Inc. is a Taiwan-based company engaged in the design, manufacture, and maintenance of various electronic testing systems and equipment, with operations extending from Taiwan to China, the United States, and other global markets. The company has a market capitalization of approximately NT$130.08 billion.

Operations: Chroma ATE's revenue is primarily derived from its Measuring Instruments Business, which generated NT$28.49 billion, and its Automated Transport Engineering segment, contributing NT$1.57 billion.

Insider Ownership: 14.5%

Chroma ATE, trading 11.6% below its estimated fair value, showcases strong insider ownership dynamics favorable for growth-focused investors. Despite a highly volatile share price recently, the company's earnings are expected to grow by 19.7% annually, outpacing the Taiwan market's average. However, its dividend coverage is weak with only 2.15% not well supported by free cash flows. Recent engagements at multiple tech conferences underscore its active market presence and commitment to growth amidst competitive pressures.

- Take a closer look at Chroma ATE's potential here in our earnings growth report.

- In light of our recent valuation report, it seems possible that Chroma ATE is trading beyond its estimated value.

Taking Advantage

- Delve into our full catalog of 1452 Fast Growing Companies With High Insider Ownership here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Kinik might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:1560

Kinik

Produces and sells various abrasives, cutting tools, and reclaimed wafers in Taiwan and internationally.

High growth potential with excellent balance sheet and pays a dividend.