Advertisement

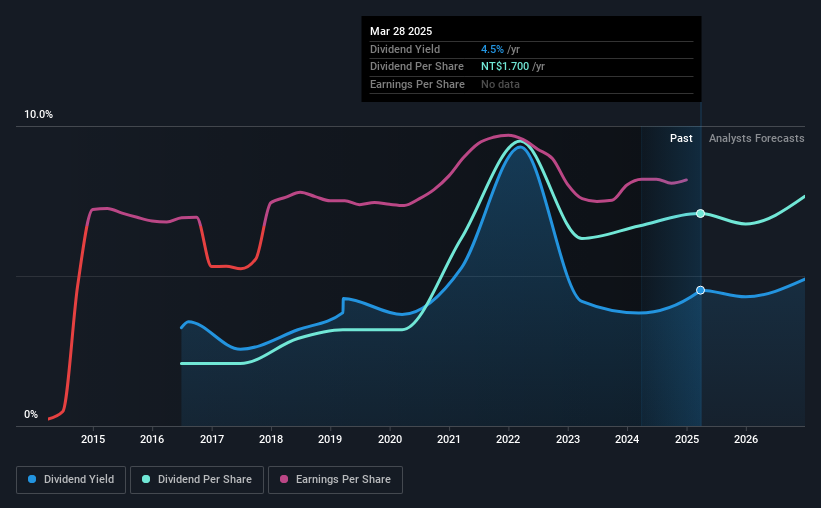

The board of Acer Incorporated (TWSE:2353) has announced that it will be paying its dividend of NT$1.70 on the 24th of July, an increased payment from last year's comparable dividend. This takes the dividend yield to 4.5%, which shareholders will be pleased with.

Acer's Payment Could Potentially Have Solid Earnings Coverage

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Prior to this announcement, Acer's dividend was making up a very large proportion of earnings, and the company was also not generating any cash flow to offset this. Generally, we think that this would be a risky long term practice.

Over the next year, EPS is forecast to expand by 47.3%. Assuming the dividend continues along the course it has been charting recently, our estimates show the payout ratio being 73% which brings it into quite a comfortable range.

See our latest analysis for Acer

Acer's Dividend Has Lacked Consistency

It's comforting to see that Acer has been paying a dividend for a number of years now, however it has been cut at least once in that time. This suggests that the dividend might not be the most reliable. Since 2016, the dividend has gone from NT$0.50 total annually to NT$1.70. This works out to be a compound annual growth rate (CAGR) of approximately 15% a year over that time. It is great to see strong growth in the dividend payments, but cuts are concerning as it may indicate the payout policy is too ambitious.

Acer Might Find It Hard To Grow Its Dividend

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. It's encouraging to see that Acer has been growing its earnings per share at 16% a year over the past five years. Past earnings growth has been decent, but unless this is one of those rare businesses that can grow without additional capital investment or marketing spend, we'd generally expect the higher payout ratio to limit its future growth prospects.

The Dividend Could Prove To Be Unreliable

In summary, while it's always good to see the dividend being raised, we don't think Acer's payments are rock solid. In general, the distributions are a little bit higher than we would like, but we can't ignore the fact the quickly growing earnings gives this stock great potential in the future. This company is not in the top tier of income providing stocks.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. For instance, we've picked out 2 warning signs for Acer that investors should take into consideration. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:2353

Acer

Research, designs, markets, and sells computers and display products Taiwan and internationally.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor