Advertisement

- Taiwan

- /

- Semiconductors

- /

- TWSE:3450

Elite Advanced Laser Corporation's (TWSE:3450) Shares Climb 30% But Its Business Is Yet to Catch Up

Despite an already strong run, Elite Advanced Laser Corporation (TWSE:3450) shares have been powering on, with a gain of 30% in the last thirty days. The last 30 days were the cherry on top of the stock's 457% gain in the last year, which is nothing short of spectacular.

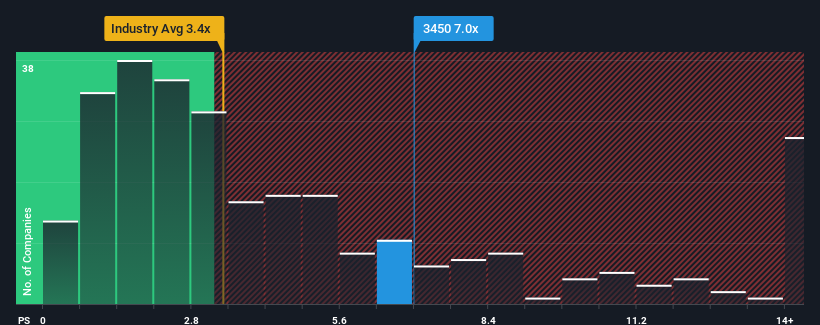

After such a large jump in price, when almost half of the companies in Taiwan's Semiconductor industry have price-to-sales ratios (or "P/S") below 3.4x, you may consider Elite Advanced Laser as a stock not worth researching with its 7x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

Check out our latest analysis for Elite Advanced Laser

How Has Elite Advanced Laser Performed Recently?

Recent revenue growth for Elite Advanced Laser has been in line with the industry. Perhaps the market is expecting future revenue performance to improve, justifying the currently elevated P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on analyst estimates for the company? Then our free report on Elite Advanced Laser will help you uncover what's on the horizon.How Is Elite Advanced Laser's Revenue Growth Trending?

In order to justify its P/S ratio, Elite Advanced Laser would need to produce outstanding growth that's well in excess of the industry.

Retrospectively, the last year delivered an exceptional 19% gain to the company's top line. However, this wasn't enough as the latest three year period has seen the company endure a nasty 7.2% drop in revenue in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Shifting to the future, estimates from the one analyst covering the company suggest revenue should grow by 115% over the next year. With the industry predicted to deliver 15,030% growth, the company is positioned for a weaker revenue result.

With this in consideration, we believe it doesn't make sense that Elite Advanced Laser's P/S is outpacing its industry peers. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of revenue growth is likely to weigh heavily on the share price eventually.

The Key Takeaway

Shares in Elite Advanced Laser have seen a strong upwards swing lately, which has really helped boost its P/S figure. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

It comes as a surprise to see Elite Advanced Laser trade at such a high P/S given the revenue forecasts look less than stellar. When we see a weak revenue outlook, we suspect the share price faces a much greater risk of declining, bringing back down the P/S figures. At these price levels, investors should remain cautious, particularly if things don't improve.

Before you settle on your opinion, we've discovered 1 warning sign for Elite Advanced Laser that you should be aware of.

If these risks are making you reconsider your opinion on Elite Advanced Laser, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Elite Advanced Laser might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:3450

Elite Advanced Laser

Provides electronic manufacturing services in Taiwan.

High growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor