Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Episil-Precision Inc. (TPE:3016) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Episil-Precision

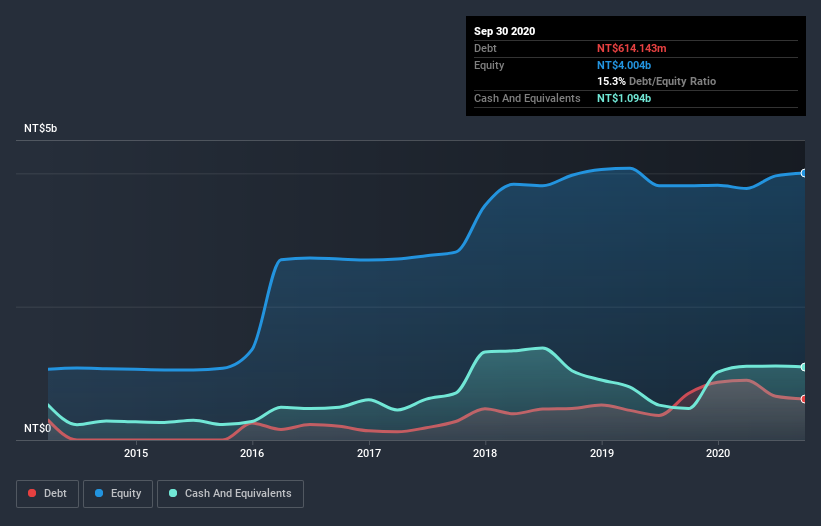

What Is Episil-Precision's Debt?

As you can see below, Episil-Precision had NT$614.1m of debt at September 2020, down from NT$697.4m a year prior. But it also has NT$1.09b in cash to offset that, meaning it has NT$480.0m net cash.

How Strong Is Episil-Precision's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Episil-Precision had liabilities of NT$980.8m due within 12 months and liabilities of NT$876.3m due beyond that. On the other hand, it had cash of NT$1.09b and NT$1.09b worth of receivables due within a year. So it can boast NT$331.1m more liquid assets than total liabilities.

This state of affairs indicates that Episil-Precision's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the NT$19.9b company is struggling for cash, we still think it's worth monitoring its balance sheet. Succinctly put, Episil-Precision boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Episil-Precision will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Episil-Precision made a loss at the EBIT level, and saw its revenue drop to NT$4.0b, which is a fall of 3.7%. We would much prefer see growth.

So How Risky Is Episil-Precision?

While Episil-Precision lost money on an earnings before interest and tax (EBIT) level, it actually generated positive free cash flow NT$517m. So although it is loss-making, it doesn't seem to have too much near-term balance sheet risk, keeping in mind the net cash. With mediocre revenue growth in the last year, we're don't find the investment opportunity particularly compelling. When we look at a riskier company, we like to check how their profits (or losses) are trending over time. Today, we're providing readers this interactive graph showing how Episil-Precision's profit, revenue, and operating cashflow have changed over the last few years.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade Episil-Precision, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Episil-Precision might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:3016

Episil-Precision

Engages in the development, manufacturing, and sale of silicon epitaxy wafers and compound semiconductor epitaxial wafers in Taiwan, Japan, China, and internationally.

Excellent balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.0% undervalued

TI

Community Contributor