Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Formosa Petrochemical Corporation (TPE:6505) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Formosa Petrochemical

What Is Formosa Petrochemical's Debt?

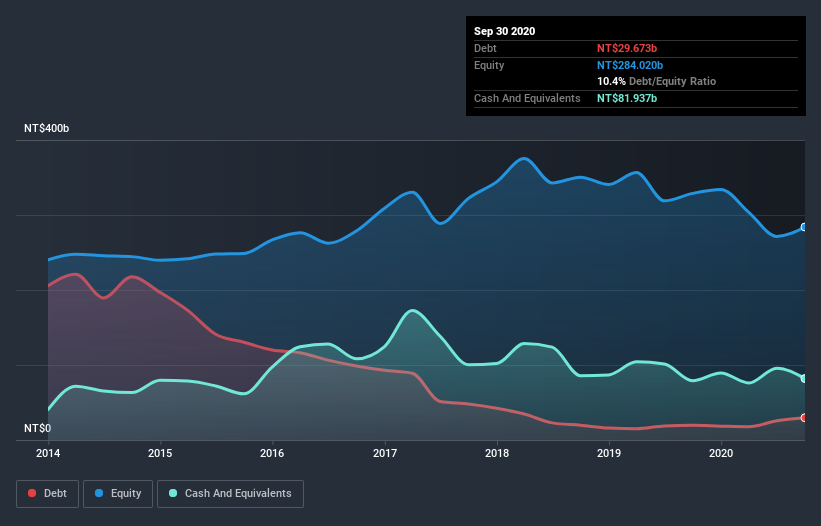

As you can see below, at the end of September 2020, Formosa Petrochemical had NT$29.7b of debt, up from NT$19.5b a year ago. Click the image for more detail. But on the other hand it also has NT$81.9b in cash, leading to a NT$52.3b net cash position.

A Look At Formosa Petrochemical's Liabilities

Zooming in on the latest balance sheet data, we can see that Formosa Petrochemical had liabilities of NT$24.9b due within 12 months and liabilities of NT$39.7b due beyond that. On the other hand, it had cash of NT$81.9b and NT$41.1b worth of receivables due within a year. So it can boast NT$58.4b more liquid assets than total liabilities.

This short term liquidity is a sign that Formosa Petrochemical could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, Formosa Petrochemical boasts net cash, so it's fair to say it does not have a heavy debt load!

It is just as well that Formosa Petrochemical's load is not too heavy, because its EBIT was down 100% over the last year. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Formosa Petrochemical's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Formosa Petrochemical has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, Formosa Petrochemical actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Formosa Petrochemical has net cash of NT$52.3b, as well as more liquid assets than liabilities. And it impressed us with free cash flow of NT$27b, being 106% of its EBIT. So we don't have any problem with Formosa Petrochemical's use of debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 2 warning signs for Formosa Petrochemical that you should be aware of before investing here.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade Formosa Petrochemical, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TWSE:6505

Formosa Petrochemical

Engages in the petrochemical business in Taiwan, Australia, South Korea, the Philippines, Singapore, Malaysia, Mainland China, and internationally.

Moderate growth potential with mediocre balance sheet.