Advertisement

- Taiwan

- /

- Food and Staples Retail

- /

- TPEX:5903

Does Taiwan FamilyMart (GTSM:5903) Have A Healthy Balance Sheet?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Taiwan FamilyMart Co., Ltd. (GTSM:5903) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Taiwan FamilyMart

What Is Taiwan FamilyMart's Net Debt?

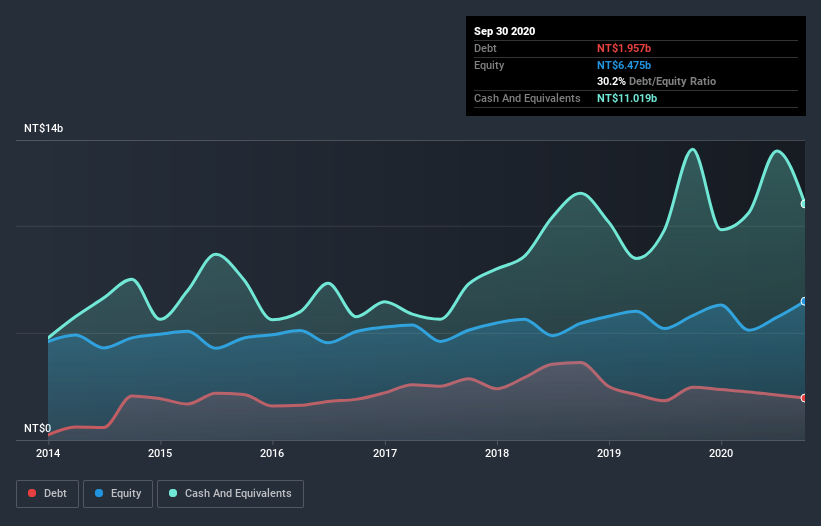

You can click the graphic below for the historical numbers, but it shows that Taiwan FamilyMart had NT$1.96b of debt in September 2020, down from NT$2.47b, one year before. But it also has NT$11.0b in cash to offset that, meaning it has NT$9.06b net cash.

How Strong Is Taiwan FamilyMart's Balance Sheet?

According to the last reported balance sheet, Taiwan FamilyMart had liabilities of NT$29.7b due within 12 months, and liabilities of NT$23.8b due beyond 12 months. On the other hand, it had cash of NT$11.0b and NT$2.22b worth of receivables due within a year. So it has liabilities totalling NT$40.2b more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of NT$58.5b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. While it does have liabilities worth noting, Taiwan FamilyMart also has more cash than debt, so we're pretty confident it can manage its debt safely.

On top of that, Taiwan FamilyMart grew its EBIT by 31% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Taiwan FamilyMart's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. Taiwan FamilyMart may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, Taiwan FamilyMart actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

Although Taiwan FamilyMart's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of NT$9.06b. And it impressed us with free cash flow of NT$4.8b, being 254% of its EBIT. So we don't think Taiwan FamilyMart's use of debt is risky. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Taiwan FamilyMart's earnings per share history for free.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

When trading Taiwan FamilyMart or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Taiwan FamilyMart might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TPEX:5903

Taiwan FamilyMart

Engages in operating and managing convenience stores in Taiwan and internationally.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor