Advertisement

- Taiwan

- /

- Trade Distributors

- /

- TWSE:1725

Yuan Jen Enterprises Co.,Ltd.'s (TWSE:1725) 26% Price Boost Is Out Of Tune With Earnings

Despite an already strong run, Yuan Jen Enterprises Co.,Ltd. (TWSE:1725) shares have been powering on, with a gain of 26% in the last thirty days. The last 30 days bring the annual gain to a very sharp 61%.

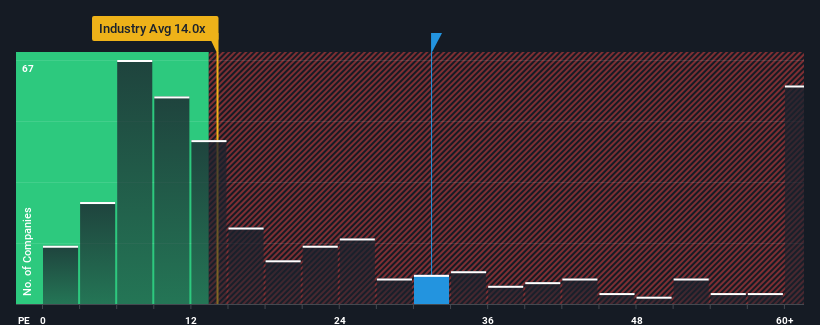

Since its price has surged higher, given around half the companies in Taiwan have price-to-earnings ratios (or "P/E's") below 23x, you may consider Yuan Jen EnterprisesLtd as a stock to potentially avoid with its 31.4x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

For instance, Yuan Jen EnterprisesLtd's receding earnings in recent times would have to be some food for thought. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Yuan Jen EnterprisesLtd

Is There Enough Growth For Yuan Jen EnterprisesLtd?

The only time you'd be truly comfortable seeing a P/E as high as Yuan Jen EnterprisesLtd's is when the company's growth is on track to outshine the market.

Retrospectively, the last year delivered a frustrating 21% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 20% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

In contrast to the company, the rest of the market is expected to grow by 25% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

In light of this, it's alarming that Yuan Jen EnterprisesLtd's P/E sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the recent negative growth rates.

What We Can Learn From Yuan Jen EnterprisesLtd's P/E?

Yuan Jen EnterprisesLtd shares have received a push in the right direction, but its P/E is elevated too. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Yuan Jen EnterprisesLtd currently trades on a much higher than expected P/E since its recent earnings have been in decline over the medium-term. When we see earnings heading backwards and underperforming the market forecasts, we suspect the share price is at risk of declining, sending the high P/E lower. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

You should always think about risks. Case in point, we've spotted 2 warning signs for Yuan Jen EnterprisesLtd you should be aware of, and 1 of them doesn't sit too well with us.

Of course, you might also be able to find a better stock than Yuan Jen EnterprisesLtd. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:1725

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor