Advertisement

- Taiwan

- /

- Auto Components

- /

- TWSE:2101

Nankang Rubber Tire Corp.,Ltd.'s (TWSE:2101) Business Is Yet to Catch Up With Its Share Price

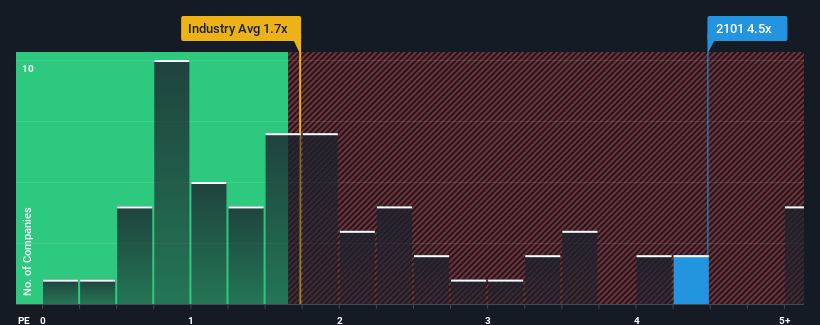

When close to half the companies in the Auto Components industry in Taiwan have price-to-sales ratios (or "P/S") below 1.7x, you may consider Nankang Rubber Tire Corp.,Ltd. (TWSE:2101) as a stock to avoid entirely with its 4.5x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

Check out our latest analysis for Nankang Rubber TireLtd

What Does Nankang Rubber TireLtd's P/S Mean For Shareholders?

Revenue has risen firmly for Nankang Rubber TireLtd recently, which is pleasing to see. One possibility is that the P/S ratio is high because investors think this respectable revenue growth will be enough to outperform the broader industry in the near future. If not, then existing shareholders may be a little nervous about the viability of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Nankang Rubber TireLtd's earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For Nankang Rubber TireLtd?

The only time you'd be truly comfortable seeing a P/S as steep as Nankang Rubber TireLtd's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered an exceptional 19% gain to the company's top line. However, this wasn't enough as the latest three year period has seen the company endure a nasty 12% drop in revenue in aggregate. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Weighing that medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 7.2% shows it's an unpleasant look.

In light of this, it's alarming that Nankang Rubber TireLtd's P/S sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

The Bottom Line On Nankang Rubber TireLtd's P/S

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Nankang Rubber TireLtd revealed its shrinking revenue over the medium-term isn't resulting in a P/S as low as we expected, given the industry is set to grow. When we see revenue heading backwards and underperforming the industry forecasts, we feel the possibility of the share price declining is very real, bringing the P/S back into the realm of reasonability. Should recent medium-term revenue trends persist, it would pose a significant risk to existing shareholders' investments and prospective investors will have a hard time accepting the current value of the stock.

Plus, you should also learn about these 2 warning signs we've spotted with Nankang Rubber TireLtd.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Nankang Rubber TireLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:2101

Nankang Rubber TireLtd

Manufactures and sells tires and various rubber supplies in Taiwan, China, America, Europe, Asia, and internationally.

Mediocre balance sheet not a dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor