Advertisement

- Taiwan

- /

- Auto Components

- /

- TWSE:1319

Why Investors Shouldn't Be Surprised By Tong Yang Industry Co., Ltd.'s (TWSE:1319) Low P/E

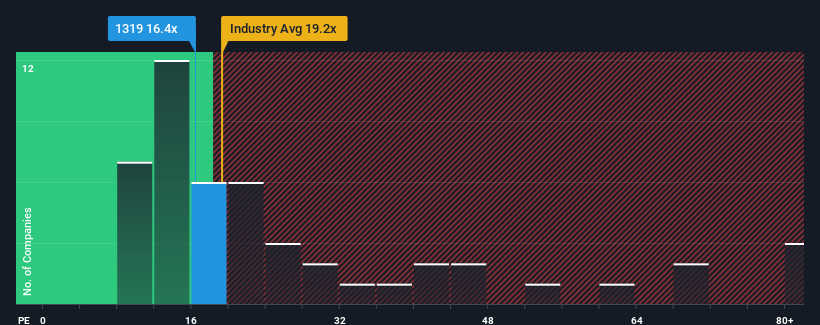

With a price-to-earnings (or "P/E") ratio of 16.4x Tong Yang Industry Co., Ltd. (TWSE:1319) may be sending bullish signals at the moment, given that almost half of all companies in Taiwan have P/E ratios greater than 24x and even P/E's higher than 43x are not unusual. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Recent times have been pleasing for Tong Yang Industry as its earnings have risen in spite of the market's earnings going into reverse. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Tong Yang Industry

How Is Tong Yang Industry's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as low as Tong Yang Industry's is when the company's growth is on track to lag the market.

If we review the last year of earnings growth, the company posted a terrific increase of 58%. The strong recent performance means it was also able to grow EPS by 433% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the four analysts covering the company suggest earnings should grow by 8.7% per year over the next three years. With the market predicted to deliver 13% growth per annum, the company is positioned for a weaker earnings result.

In light of this, it's understandable that Tong Yang Industry's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Bottom Line On Tong Yang Industry's P/E

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Tong Yang Industry maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Before you settle on your opinion, we've discovered 1 warning sign for Tong Yang Industry that you should be aware of.

If you're unsure about the strength of Tong Yang Industry's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Tong Yang Industry might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:1319

Tong Yang Industry

Engages in the manufacture and sale of parts, components, and models for automobile in Taiwan, China, the United States, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor