Stock Analysis

Three SGX Stocks Estimated To Trade At Discounts Between 42.5% And 45.3%

Reviewed by Simply Wall St

As the global financial landscape evolves, Singapore's market is uniquely positioned to capitalize on emerging trends such as the tokenisation of trade finance assets. This shift towards digital assets highlights a broader transformation in investment opportunities and market dynamics. In this context, identifying stocks that are potentially undervalued becomes crucial, as they may offer significant growth potential amidst these transformative economic conditions.

Top 5 Undervalued Stocks Based On Cash Flows In Singapore

| Name | Current Price | Fair Value (Est) | Discount (Est) |

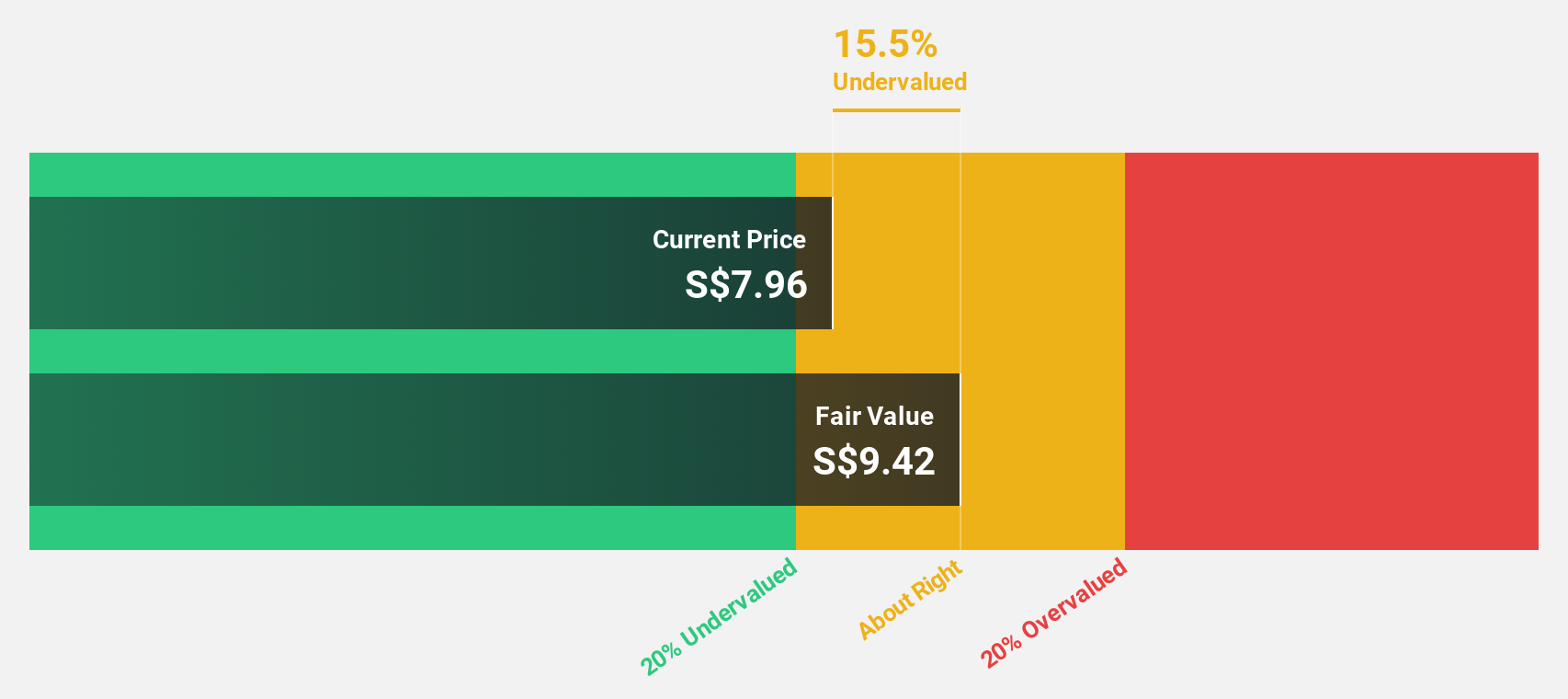

| Singapore Technologies Engineering (SGX:S63) | SGD4.33 | SGD7.92 | 45.3% |

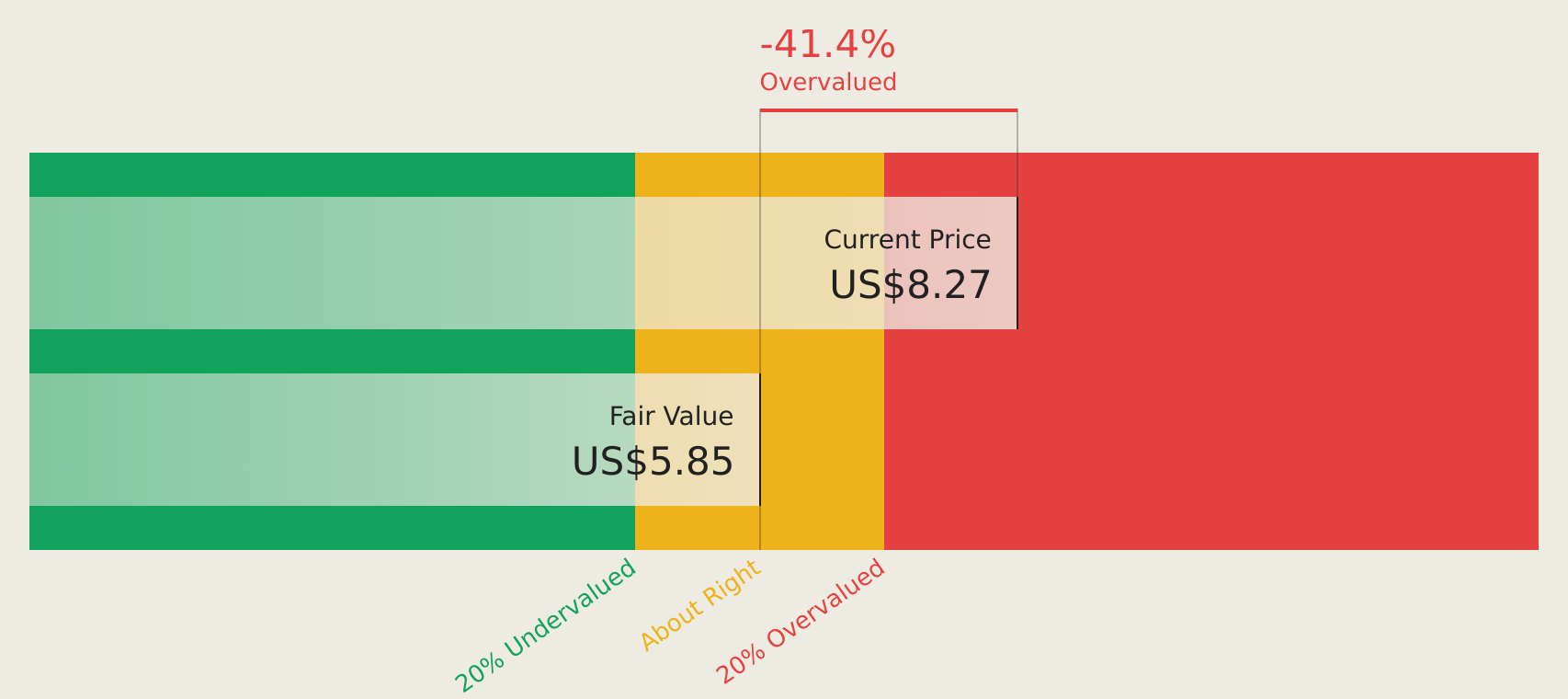

| Hongkong Land Holdings (SGX:H78) | US$3.25 | US$5.66 | 42.5% |

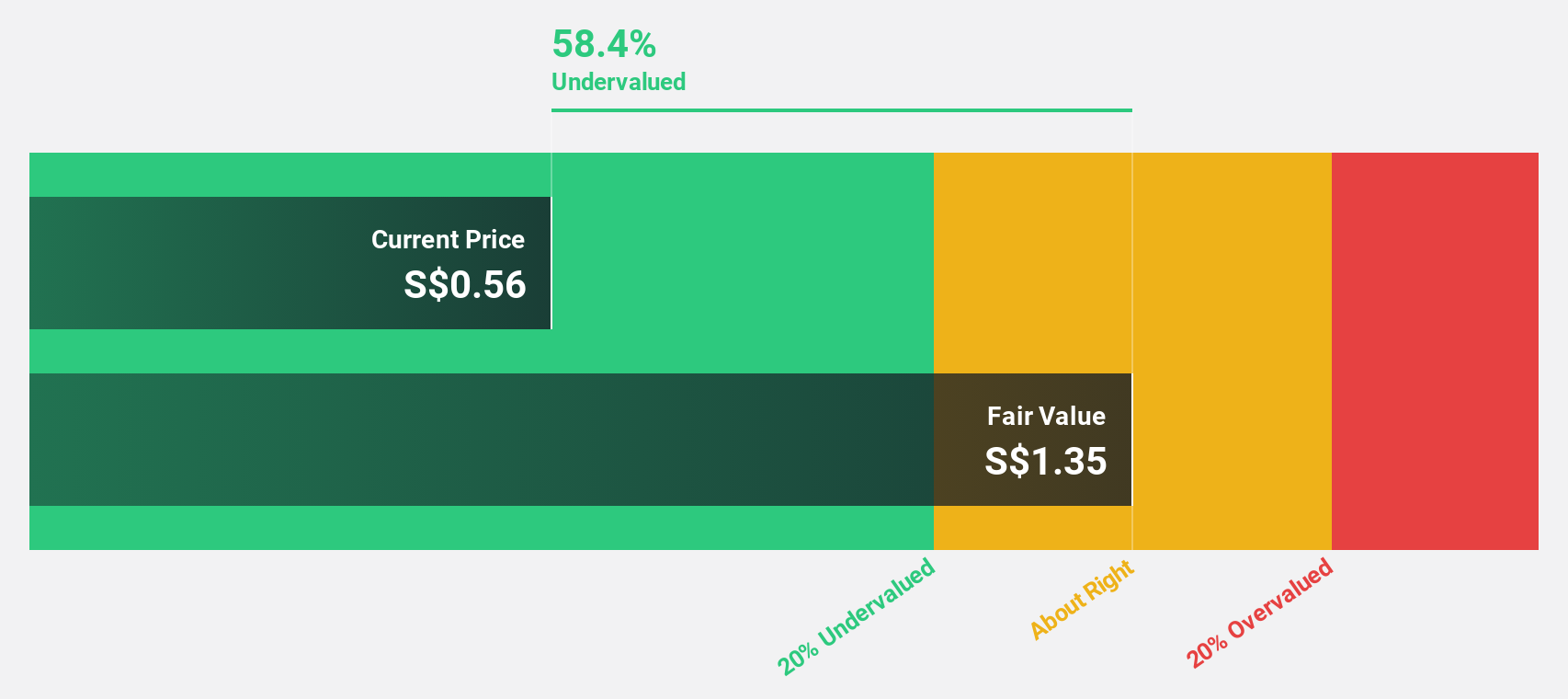

| Digital Core REIT (SGX:DCRU) | US$0.56 | US$1.11 | 49.4% |

| Frasers Logistics & Commercial Trust (SGX:BUOU) | SGD0.955 | SGD1.62 | 41.2% |

| Seatrium (SGX:5E2) | SGD1.39 | SGD2.32 | 40.2% |

| Nanofilm Technologies International (SGX:MZH) | SGD0.745 | SGD1.34 | 44.6% |

Here's a peek at a few of the choices from the screener

Hongkong Land Holdings (SGX:H78)

Overview: Hongkong Land Holdings Limited operates in the investment, development, and management of properties across Hong Kong, Macau, Mainland China, Southeast Asia, and other international locations with a market cap of $7.17 billion.

Operations: The company generates revenue from two main segments: Investment Properties, which brought in $1.08 billion, and Development Properties, contributing $0.76 billion.

Estimated Discount To Fair Value: 42.5%

Hongkong Land Holdings, trading at S$3.25, significantly below the estimated fair value of S$5.66, appears undervalued based on cash flows. Despite a low forecasted return on equity of 2.4% in three years and dividends not well covered by earnings, the company is expected to turn profitable with projected earnings growth notably higher than market average. Recent data indicates stable underlying profit and a strong performance from its luxury retail portfolio and Singapore office properties.

- According our earnings growth report, there's an indication that Hongkong Land Holdings might be ready to expand.

- Dive into the specifics of Hongkong Land Holdings here with our thorough financial health report.

Nanofilm Technologies International (SGX:MZH)

Overview: Nanofilm Technologies International Limited offers nanotechnology solutions across Singapore, China, Japan, and Vietnam with a market capitalization of approximately SGD 485 million.

Operations: The company generates revenue from four primary segments: Sydrogen (SGD 1.05 million), Nanofabrication (SGD 16.05 million), Advanced Materials (SGD 141.54 million), and Industrial Equipment (SGD 37.17 million).

Estimated Discount To Fair Value: 44.6%

Nanofilm Technologies International, priced at SGD0.75, is considerably below the estimated fair value of SGD1.34, suggesting undervaluation based on discounted cash flow analysis. Despite a modest return on equity forecast at 9% in three years, the company is poised for significant earnings growth annually at 50.7%, outpacing the Singapore market average significantly. However, it's important to note a substantial decline in profit margins from 18.5% last year to 1.8% this year. Recent corporate guidance indicates optimism for fiscal year 2024 with expected increases in revenue and profits.

- Our earnings growth report unveils the potential for significant increases in Nanofilm Technologies International's future results.

- Get an in-depth perspective on Nanofilm Technologies International's balance sheet by reading our health report here.

Singapore Technologies Engineering (SGX:S63)

Overview: Singapore Technologies Engineering Ltd is a global technology, defense, and engineering group with a market capitalization of SGD 13.50 billion.

Operations: The company's revenue is divided among Commercial Aerospace (SGD 3.97 billion), Urban Solutions & Satcom (SGD 1.98 billion), and Defence & Public Security (SGD 4.29 billion).

Estimated Discount To Fair Value: 45.3%

Singapore Technologies Engineering, with a current price of SGD4.33, is trading at a substantial discount to its estimated fair value of SGD7.92, indicating potential undervaluation based on cash flows. While the company's earnings are expected to grow by 11.6% annually, outperforming the Singapore market forecast of 9%, it maintains a high debt level and an unstable dividend track record. Recent activities include initiating a share repurchase program and affirming dividends, reflecting confidence in financial management despite some concerns over its financial position.

- Our comprehensive growth report raises the possibility that Singapore Technologies Engineering is poised for substantial financial growth.

- Click here to discover the nuances of Singapore Technologies Engineering with our detailed financial health report.

Make It Happen

- Click through to start exploring the rest of the 3 Undervalued SGX Stocks Based On Cash Flows now.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Nanofilm Technologies International is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:MZH

Nanofilm Technologies International

Provides nanotechnology solutions in Singapore, China, Japan, and Vietnam.

Flawless balance sheet with reasonable growth potential.