Advertisement

- Singapore

- /

- Medical Equipment

- /

- SGX:AP4

Why It Might Not Make Sense To Buy Riverstone Holdings Limited (SGX:AP4) For Its Upcoming Dividend

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Riverstone Holdings Limited (SGX:AP4) is about to trade ex-dividend in the next four days. The ex-dividend date is two business days before a company's record date in most cases, which is the date on which the company determines which shareholders are entitled to receive a dividend. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade can take two business days or more to settle. Thus, you can purchase Riverstone Holdings' shares before the 16th of September in order to receive the dividend, which the company will pay on the 3rd of October.

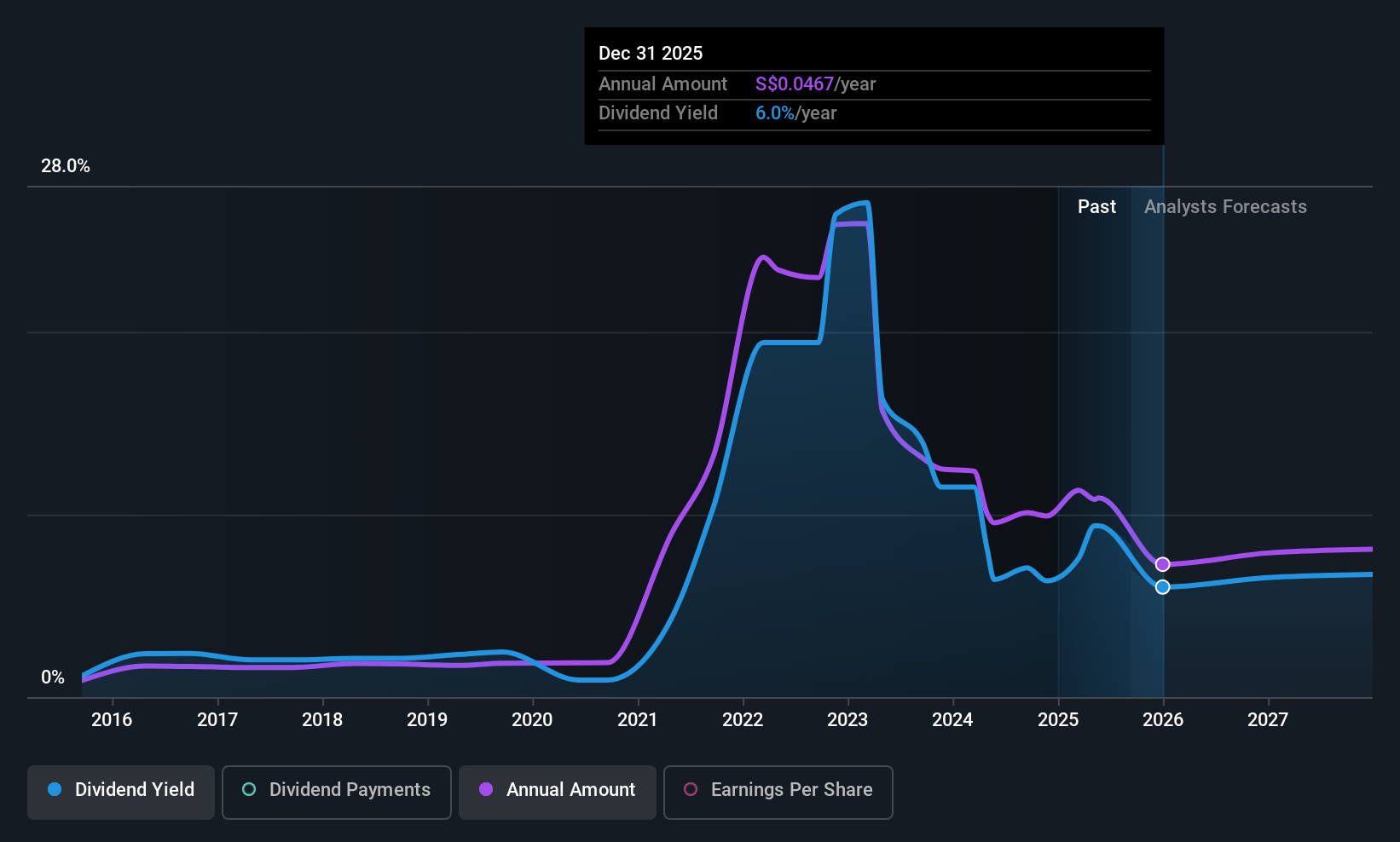

The company's next dividend payment will be RM00.025 per share. Last year, in total, the company distributed RM0.23 to shareholders. Calculating the last year's worth of payments shows that Riverstone Holdings has a trailing yield of 8.4% on the current share price of S$0.775. If you buy this business for its dividend, you should have an idea of whether Riverstone Holdings's dividend is reliable and sustainable. So we need to investigate whether Riverstone Holdings can afford its dividend, and if the dividend could grow.

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Last year Riverstone Holdings paid out 106% of its profits as dividends to shareholders, suggesting the dividend is not well covered by earnings. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Over the past year it paid out 128% of its free cash flow as dividends, which is uncomfortably high. It's hard to consistently pay out more cash than you generate without either borrowing or using company cash, so we'd wonder how the company justifies this payout level.

Riverstone Holdings does have a large net cash position on the balance sheet, which could fund large dividends for a time, if the company so chose. Still, smart investors know that it is better to assess dividends relative to the cash and profit generated by the business. Paying dividends out of cash on the balance sheet is not long-term sustainable.

Cash is slightly more important than profit from a dividend perspective, but given Riverstone Holdings's payments were not well covered by either earnings or cash flow, we are concerned about the sustainability of this dividend.

See our latest analysis for Riverstone Holdings

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings fall far enough, the company could be forced to cut its dividend. Fortunately for readers, Riverstone Holdings's earnings per share have been growing at 13% a year for the past five years. We're a bit put out by the fact that Riverstone Holdings paid out virtually all of its earnings and cashflow as dividends over the last year. Earnings are growing at a decent clip, so this payout ratio may prove sustainable, but it's not great to see.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Since the start of our data, 10 years ago, Riverstone Holdings has lifted its dividend by approximately 29% a year on average. It's great to see earnings per share growing rapidly over several years, and dividends per share growing right along with it.

To Sum It Up

Is Riverstone Holdings an attractive dividend stock, or better left on the shelf? While it's nice to see earnings per share growing, we're curious about how Riverstone Holdings intends to continue growing, or maintain the dividend in a downturn given that it's paying out such a high percentage of its earnings and cashflow. With the way things are shaping up from a dividend perspective, we'd be inclined to steer clear of Riverstone Holdings.

Having said that, if you're looking at this stock without much concern for the dividend, you should still be familiar of the risks involved with Riverstone Holdings. For example - Riverstone Holdings has 1 warning sign we think you should be aware of.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:AP4

Riverstone Holdings

An investment holding company, engages in the manufacture and distribution of cleanroom and healthcare gloves in Malaysia, Thailand, and China.

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor