Advertisement

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Speaking of which, we noticed some great changes in Sinostar PEC Holdings' (SGX:C9Q) returns on capital, so let's have a look.

What is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Sinostar PEC Holdings:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

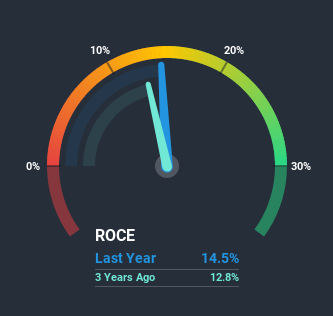

0.14 = CN¥233m ÷ (CN¥2.6b - CN¥987m) (Based on the trailing twelve months to September 2020).

So, Sinostar PEC Holdings has an ROCE of 14%. On its own, that's a standard return, however it's much better than the 6.5% generated by the Oil and Gas industry.

View our latest analysis for Sinostar PEC Holdings

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how Sinostar PEC Holdings has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

What Can We Tell From Sinostar PEC Holdings' ROCE Trend?

Sinostar PEC Holdings is displaying some positive trends. The data shows that returns on capital have increased substantially over the last five years to 14%. The amount of capital employed has increased too, by 199%. The increasing returns on a growing amount of capital is common amongst multi-baggers and that's why we're impressed.

For the record though, there was a noticeable increase in the company's current liabilities over the period, so we would attribute some of the ROCE growth to that. Effectively this means that suppliers or short-term creditors are now funding 38% of the business, which is more than it was five years ago. It's worth keeping an eye on this because as the percentage of current liabilities to total assets increases, some aspects of risk also increase.

The Bottom Line On Sinostar PEC Holdings' ROCE

A company that is growing its returns on capital and can consistently reinvest in itself is a highly sought after trait, and that's what Sinostar PEC Holdings has. And a remarkable 193% total return over the last five years tells us that investors are expecting more good things to come in the future. In light of that, we think it's worth looking further into this stock because if Sinostar PEC Holdings can keep these trends up, it could have a bright future ahead.

On a separate note, we've found 2 warning signs for Sinostar PEC Holdings you'll probably want to know about.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

When trading Sinostar PEC Holdings or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SGX:C9Q

Sinostar PEC Holdings

An investment holding company, produces and supplies petrochemical products in the People’s Republic of China.

Excellent balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor