Advertisement

- Sweden

- /

- Telecom Services and Carriers

- /

- OM:TELIA

Dividend Investors: Don't Be Too Quick To Buy Telia Company AB (publ) (STO:TELIA) For Its Upcoming Dividend

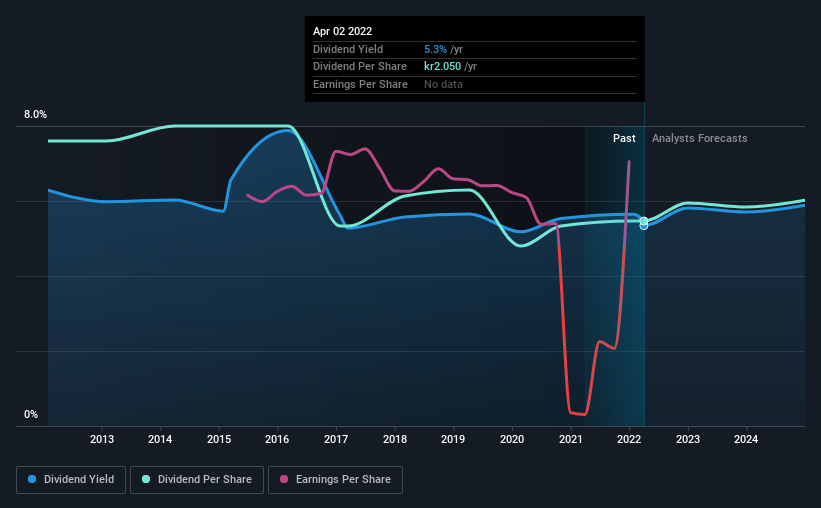

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Telia Company AB (publ) (STO:TELIA) is about to trade ex-dividend in the next 3 days. The ex-dividend date occurs one day before the record date which is the day on which shareholders need to be on the company's books in order to receive a dividend. It is important to be aware of the ex-dividend date because any trade on the stock needs to have been settled on or before the record date. This means that investors who purchase Telia Company's shares on or after the 7th of April will not receive the dividend, which will be paid on the 13th of April.

The company's next dividend payment will be kr1.00 per share. Last year, in total, the company distributed kr2.05 to shareholders. Based on the last year's worth of payments, Telia Company has a trailing yield of 5.3% on the current stock price of SEK38.38. If you buy this business for its dividend, you should have an idea of whether Telia Company's dividend is reliable and sustainable. We need to see whether the dividend is covered by earnings and if it's growing.

Check out our latest analysis for Telia Company

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Telia Company paid out more than half (73%) of its earnings last year, which is a regular payout ratio for most companies. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Over the last year it paid out 70% of its free cash flow as dividends, within the usual range for most companies.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. If earnings fall far enough, the company could be forced to cut its dividend. So we're not too excited that Telia Company's earnings are down 2.3% a year over the past five years.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Telia Company's dividend payments per share have declined at 3.2% per year on average over the past 10 years, which is uninspiring. It's never nice to see earnings and dividends falling, but at least management has cut the dividend rather than potentially risk the company's health in an attempt to maintain it.

To Sum It Up

From a dividend perspective, should investors buy or avoid Telia Company? While earnings per share are shrinking, it's encouraging to see that at least Telia Company's dividend appears sustainable, with earnings and cashflow payout ratios that are within reasonable bounds. It's not the most attractive proposition from a dividend perspective, and we'd probably give this one a miss for now.

Having said that, if you're looking at this stock without much concern for the dividend, you should still be familiar of the risks involved with Telia Company. To help with this, we've discovered 4 warning signs for Telia Company (1 is concerning!) that you ought to be aware of before buying the shares.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Telia Company might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:TELIA

Telia Company

Provides communication services to businesses, individuals, families, and communities in Sweden, Finland, Norway, Denmark, Lithuania, Estonia, and Latvia.

Solid track record second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor