Advertisement

Why SpectrumOne's (STO:SPEONE) Healthy Earnings Aren’t As Good As They Seem

The healthy profit announcement from SpectrumOne AB (publ) (STO:SPEONE ) didn't seem to impress investors. We did some digging and found some worrying factors that they might be paying attention to.

View our latest analysis for SpectrumOne

A Closer Look At SpectrumOne's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. This ratio tells us how much of a company's profit is not backed by free cashflow.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

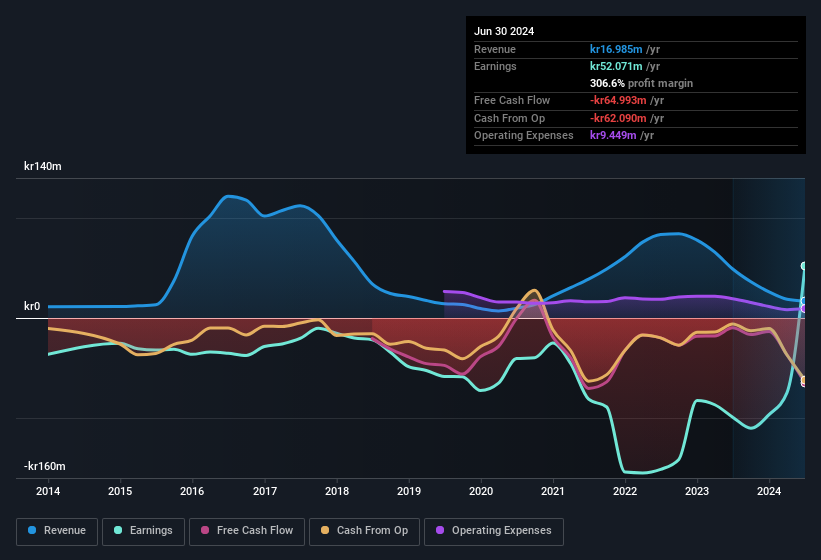

For the year to June 2024, SpectrumOne had an accrual ratio of 1.35. Statistically speaking, that's a real negative for future earnings. To wit, the company did not generate one whit of free cashflow in that time. Even though it reported a profit of kr52.1m, a look at free cash flow indicates it actually burnt through kr65m in the last year. Coming off the back of negative free cash flow last year, we imagine some shareholders might wonder if its cash burn of kr65m, this year, indicates high risk. Having said that, there is more to the story. We can see that unusual items have impacted its statutory profit, and therefore the accrual ratio. The good news for shareholders is that SpectrumOne's accrual ratio was much better last year, so this year's poor reading might simply be a case of a short term mismatch between profit and FCF. As a result, some shareholders may be looking for stronger cash conversion in the current year.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of SpectrumOne.

How Do Unusual Items Influence Profit?

The fact that the company had unusual items boosting profit by kr6.1m, in the last year, probably goes some way to explain why its accrual ratio was so weak. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's as you'd expect, given these boosts are described as 'unusual'. Assuming those unusual items don't show up again in the current year, we'd thus expect profit to be weaker next year (in the absence of business growth, that is).

Our Take On SpectrumOne's Profit Performance

Summing up, SpectrumOne received a nice boost to profit from unusual items, but could not match its paper profit with free cash flow. Considering all this we'd argue SpectrumOne's profits probably give an overly generous impression of its sustainable level of profitability. If you'd like to know more about SpectrumOne as a business, it's important to be aware of any risks it's facing. Every company has risks, and we've spotted 4 warning signs for SpectrumOne (of which 1 makes us a bit uncomfortable!) you should know about.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:SPEONE

SpectrumOne

A technology company, provides z`data management, analytics, and communications platform suites to append and analyze customer data in Sweden.

Good value with slight risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor