- Sweden

- /

- Communications

- /

- OM:HMS

3 Swedish Growth Stocks With High Insider Ownership And 56% Earnings Growth

Reviewed by Simply Wall St

As global markets continue to navigate mixed economic signals and varied earnings reports, Sweden's stock market has shown resilience, reflecting broader trends in Europe. Amidst this backdrop, identifying growth companies with high insider ownership can be a strategic approach for investors seeking to align with management interests and capitalize on potential earnings growth.

Top 10 Growth Companies With High Insider Ownership In Sweden

| Name | Insider Ownership | Earnings Growth |

| CTT Systems (OM:CTT) | 16.9% | 24.8% |

| Magle Chemoswed Holding (OM:MAGLE) | 14.9% | 72.2% |

| Biovica International (OM:BIOVIC B) | 18.7% | 73.8% |

| BioArctic (OM:BIOA B) | 34% | 103.4% |

| InCoax Networks (OM:INCOAX) | 18.1% | 104.9% |

| KebNi (OM:KEBNI B) | 37.8% | 90.4% |

| Yubico (OM:YUBICO) | 37.5% | 43.8% |

| Calliditas Therapeutics (OM:CALTX) | 11.6% | 52.9% |

| SaveLend Group (OM:YIELD) | 23.3% | 103.4% |

| edyoutec (NGM:EDYOU) | 14.6% | 63.1% |

Underneath we present a selection of stocks filtered out by our screen.

EQT (OM:EQT)

Simply Wall St Growth Rating: ★★★★★☆

Overview: EQT AB (publ) is a global private equity firm specializing in private capital and real asset segments, with a market cap of SEK403.24 billion.

Operations: The company's revenue segments include €37.20 million from Central, €878.70 million from Real Assets, and €1.28 billion from Private Capital.

Insider Ownership: 31%

Earnings Growth Forecast: 56.7% p.a.

EQT AB, a prominent private equity firm in Sweden, has shown significant growth potential and high insider ownership. Recently, EQT announced a share repurchase program authorized to buy back up to 63.93 million shares, enhancing shareholder value and adjusting capital structure. The company reported strong earnings for H1 2024 with revenue of €1.23 billion and net income of €282 million. Additionally, EQT is actively involved in high-profile M&A activities including potential acquisitions of Lighthouse Learnings and BSV Group, indicating robust expansion strategies.

- Click here and access our complete growth analysis report to understand the dynamics of EQT.

- Our valuation report unveils the possibility EQT's shares may be trading at a premium.

Fortnox (OM:FNOX)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Fortnox AB (publ) offers financial and administrative software solutions for small and medium-sized businesses, accounting firms, and organizations, with a market cap of SEK40.60 billion.

Operations: Revenue segments (in millions of SEK): Businesses: 378, Marketplaces: 160, Core Products: 734, Accounting Firms: 352, Financial Services: 249. Fortnox's revenue is derived from businesses (SEK378M), marketplaces (SEK160M), core products (SEK734M), accounting firms (SEK352M), and financial services (SEK249M).

Insider Ownership: 21%

Earnings Growth Forecast: 22.6% p.a.

Fortnox, a Swedish growth company with high insider ownership, reported robust earnings for Q2 2024 with sales of SEK 515 million and net income of SEK 164 million. The company's earnings are forecast to grow significantly at 22.6% per year, outpacing the Swedish market's average. Despite trading below its estimated fair value by 13%, Fortnox has not seen substantial insider buying recently. Revenue is expected to grow at a solid rate of 19.8% annually over the next three years.

- Click here to discover the nuances of Fortnox with our detailed analytical future growth report.

- According our valuation report, there's an indication that Fortnox's share price might be on the expensive side.

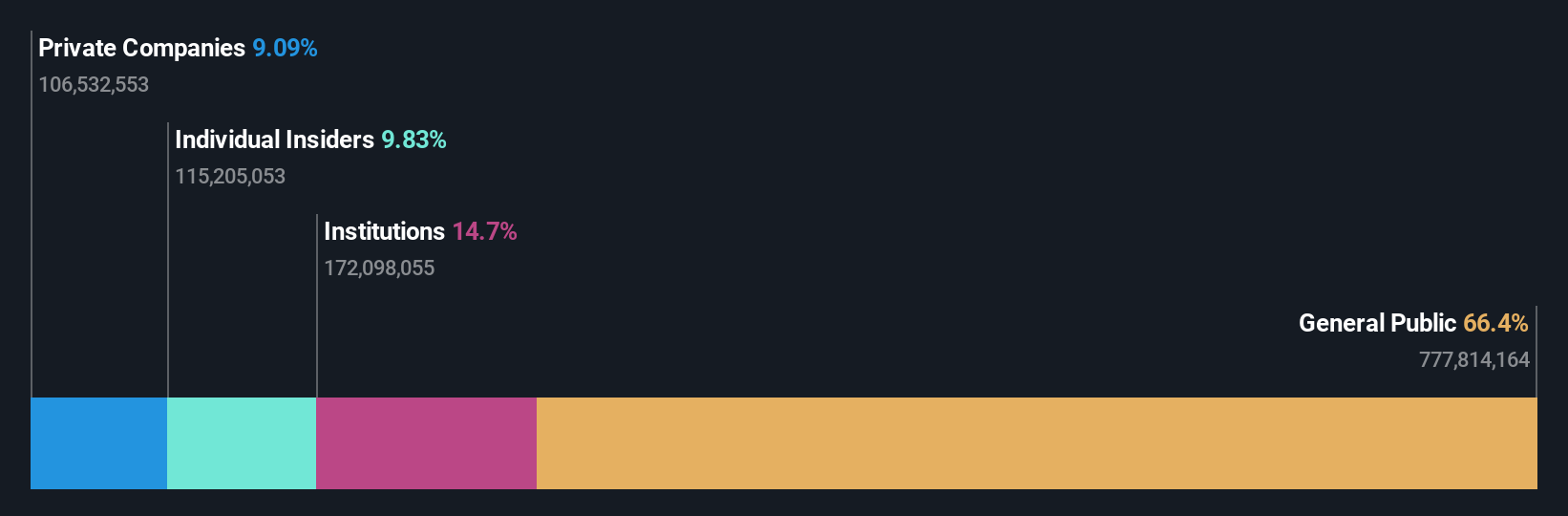

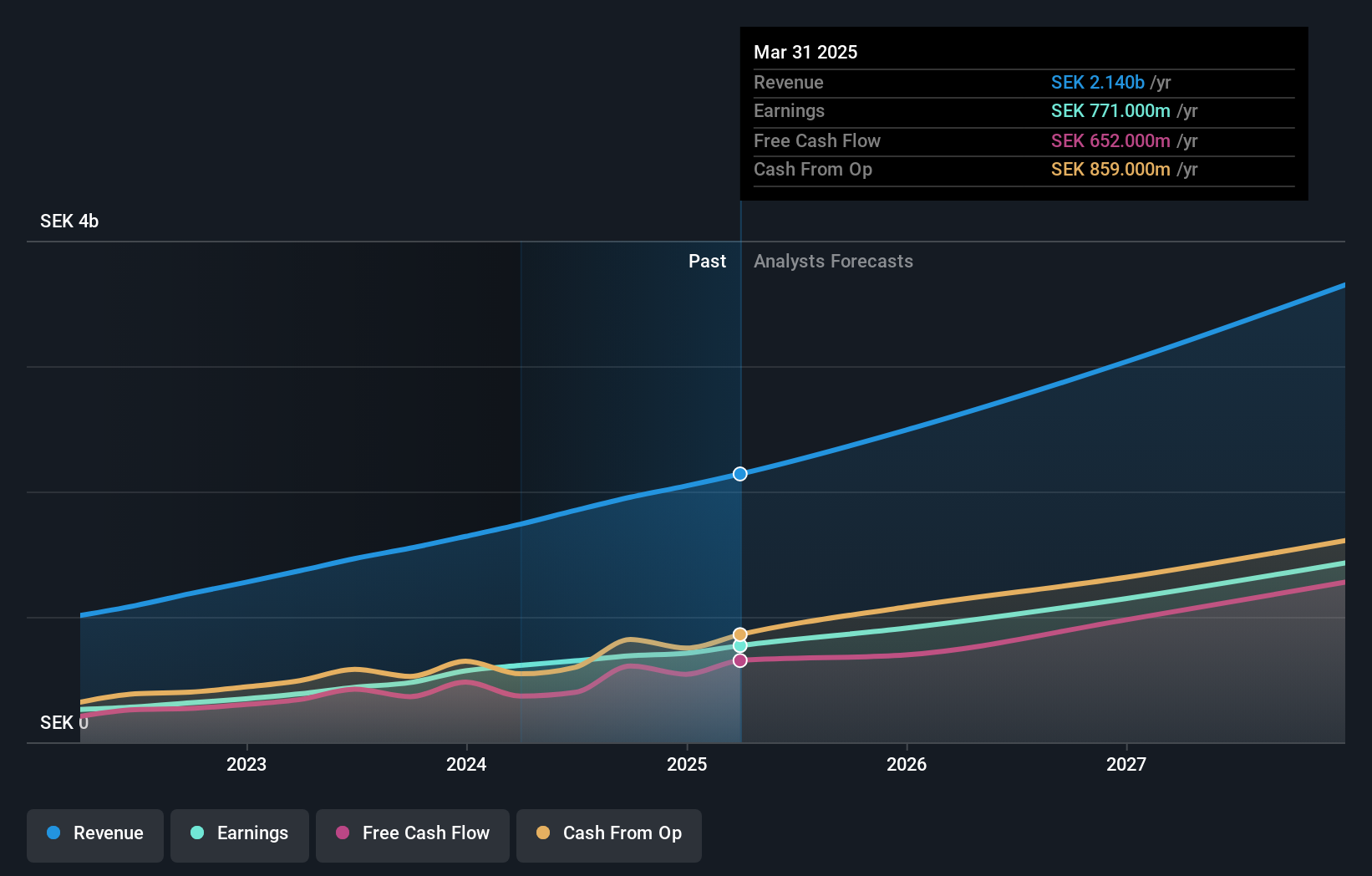

HMS Networks (OM:HMS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: HMS Networks AB (publ) provides products that enable industrial equipment to communicate and share information globally, with a market cap of SEK20.54 billion.

Operations: HMS Networks AB (publ) generates SEK3.01 billion from its Wireless Communications Equipment segment.

Insider Ownership: 12.6%

Earnings Growth Forecast: 26.3% p.a.

HMS Networks, with substantial insider ownership, reported Q2 2024 sales of SEK 845 million, up from SEK 703 million a year ago. However, net income dropped to SEK 34 million from SEK 116 million. Despite the decline in profit margins and recent shareholder dilution, HMS's earnings are forecast to grow significantly at over 26% per year. Insiders have been buying more shares than selling recently, indicating confidence in future growth prospects.

- Delve into the full analysis future growth report here for a deeper understanding of HMS Networks.

- Our comprehensive valuation report raises the possibility that HMS Networks is priced higher than what may be justified by its financials.

Key Takeaways

- Navigate through the entire inventory of 91 Fast Growing Swedish Companies With High Insider Ownership here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if HMS Networks might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:HMS

HMS Networks

Engages in the provision of products that enable industrial equipment to communicate and share information worldwide.

Reasonable growth potential with mediocre balance sheet.