- Sweden

- /

- Capital Markets

- /

- OM:EQT

3 Swedish Growth Companies With High Insider Ownership Growing Revenues At 19%

Reviewed by Simply Wall St

As the pan-European STOXX Europe 600 Index experiences modest gains amid hopes for quicker interest rate cuts by the European Central Bank, Sweden's market landscape remains a focal point for investors seeking growth opportunities. In this context, Swedish growth companies with high insider ownership are particularly appealing, as they often indicate strong confidence from those closest to the business and can offer resilience in fluctuating economic conditions.

Top 10 Growth Companies With High Insider Ownership In Sweden

| Name | Insider Ownership | Earnings Growth |

| CTT Systems (OM:CTT) | 16.9% | 24.8% |

| Truecaller (OM:TRUE B) | 29.7% | 21.7% |

| Magle Chemoswed Holding (OM:MAGLE) | 14.9% | 72.2% |

| Biovica International (OM:BIOVIC B) | 18.3% | 78.5% |

| BioArctic (OM:BIOA B) | 34% | 98.4% |

| Yubico (OM:YUBICO) | 37.5% | 42.2% |

| KebNi (OM:KEBNI B) | 36.3% | 86.1% |

| InCoax Networks (OM:INCOAX) | 20.1% | 115.5% |

| C-Rad (OM:CRAD B) | 16.1% | 33.9% |

| OrganoClick (OM:ORGC) | 23.1% | 109.0% |

Let's explore several standout options from the results in the screener.

EQT (OM:EQT)

Simply Wall St Growth Rating: ★★★★★☆

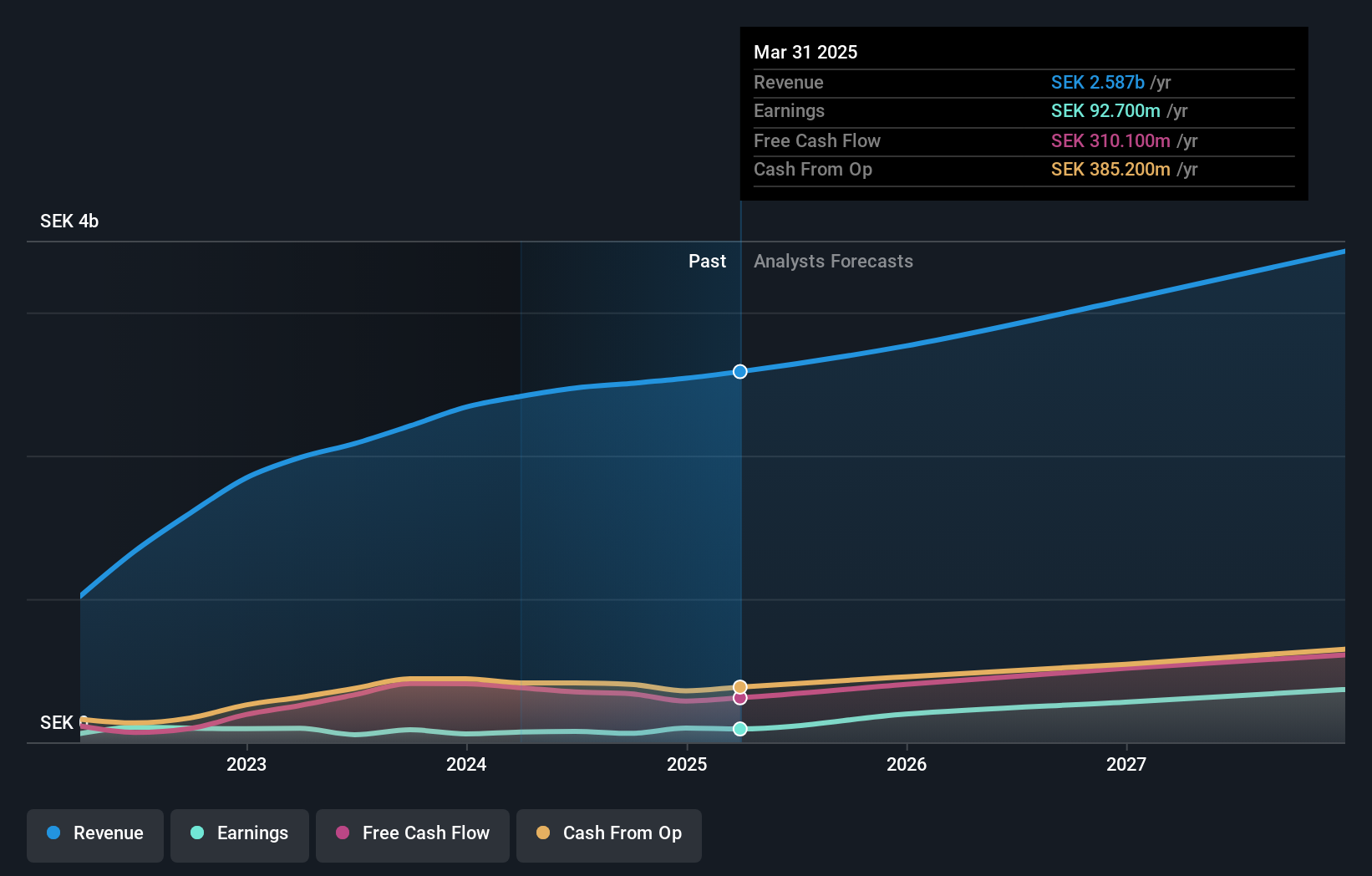

Overview: EQT AB (publ) is a global private equity firm focused on private capital and real asset segments, with a market cap of approximately SEK392.56 billion.

Operations: The company generates revenue through its segments, with €1.28 billion from Private Capital, €878.70 million from Real Assets, and €37.20 million from Central operations.

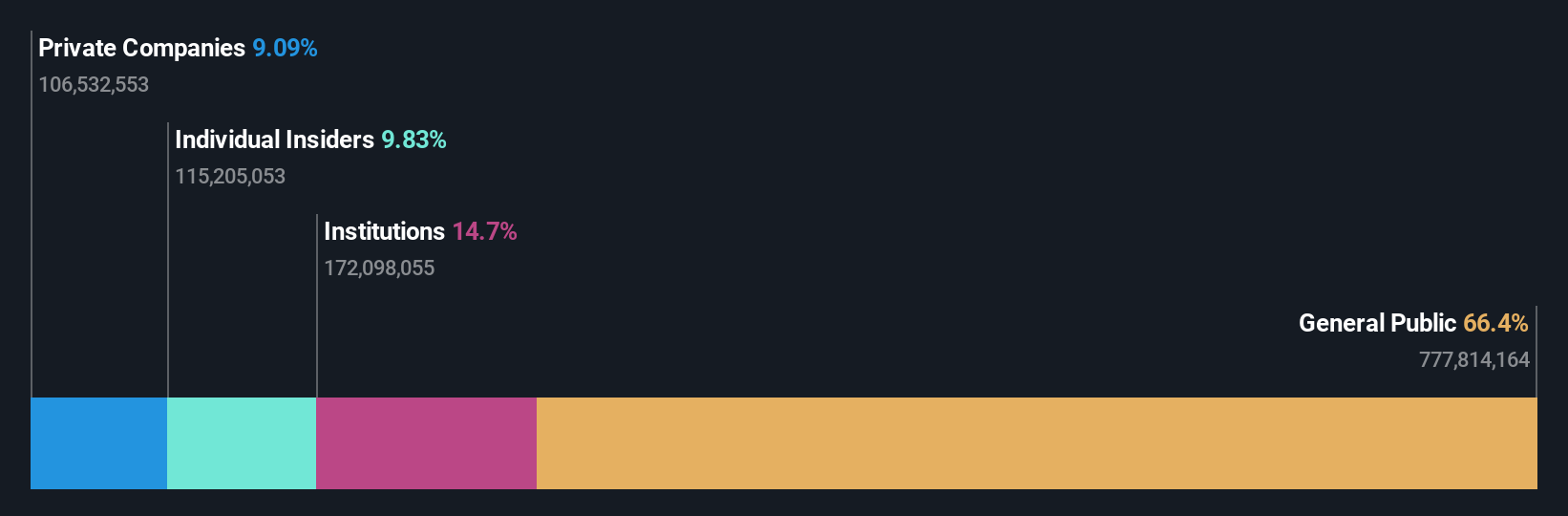

Insider Ownership: 12.3%

Revenue Growth Forecast: 15.7% p.a.

EQT AB showcases a strong growth trajectory with earnings forecasted to grow significantly at 33.7% annually, outpacing the Swedish market. Despite substantial insider selling in recent months, the company maintains high insider ownership which can align management interests with shareholders. Recent strategic moves include exploring acquisitions and divestitures, such as vying for Singapore Post's Australian assets and considering a sale of Banking Circle, indicating active portfolio management aimed at enhancing value creation.

- Navigate through the intricacies of EQT with our comprehensive analyst estimates report here.

- In light of our recent valuation report, it seems possible that EQT is trading beyond its estimated value.

Swedencare (OM:SECARE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Swedencare AB (publ) develops, manufactures, markets, and sells animal healthcare products for cats, dogs, and horses across Sweden, the United Kingdom, Europe, North America, Asia, and internationally with a market cap of SEK6.39 billion.

Operations: The company's revenue segments include SEK383.90 million from Europe, SEK591.10 million from Production, and SEK1.70 billion from North America.

Insider Ownership: 12.2%

Revenue Growth Forecast: 11.1% p.a.

Swedencare demonstrates robust growth potential with earnings forecasted to grow significantly at 55.7% annually, surpassing the Swedish market's growth rate. Recent financial results show improved profitability, with net income rising to SEK 51 million for the first half of 2024. The company has seen substantial insider buying in recent months, indicating confidence in its future prospects. However, revenue growth is expected to be moderate at 11.1% annually, below the high-growth threshold of 20%.

- Click here to discover the nuances of Swedencare with our detailed analytical future growth report.

- Our comprehensive valuation report raises the possibility that Swedencare is priced higher than what may be justified by its financials.

Swedish Logistic Property (OM:SLP B)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Swedish Logistic Property AB is a real estate company focused on acquiring, developing, and managing logistics properties in Sweden, with a market cap of SEK9.95 billion.

Operations: Swedish Logistic Property AB generates its revenue from acquiring, developing, and managing logistics properties within Sweden.

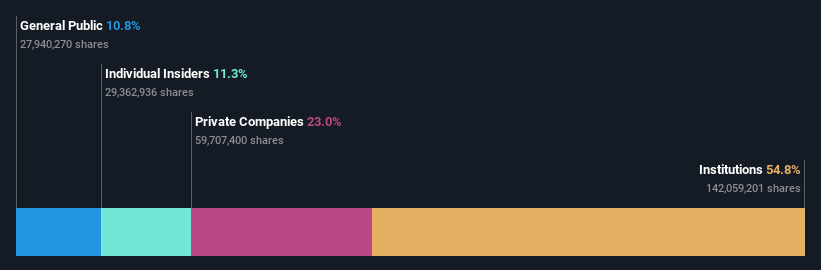

Insider Ownership: 11.3%

Revenue Growth Forecast: 19.5% p.a.

Swedish Logistic Property exhibits solid growth potential, with earnings forecasted to grow significantly at 28% annually, outpacing the Swedish market. Despite a recent dip in quarterly net income to SEK 70 million, nine-month results show improved profitability at SEK 397 million. The company trades at a favorable price-to-earnings ratio of 23.5x compared to industry peers and has expanded its portfolio by acquiring logistics properties valued at SEK 128.3 million through a share-financed transaction.

- Click to explore a detailed breakdown of our findings in Swedish Logistic Property's earnings growth report.

- Our valuation report here indicates Swedish Logistic Property may be undervalued.

Summing It All Up

- Access the full spectrum of 81 Fast Growing Swedish Companies With High Insider Ownership by clicking on this link.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if EQT might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:EQT

EQT

A global private equity firm specializing in private capital and real asset segments.

High growth potential with excellent balance sheet.