Revenue Downgrade: Here's What Analysts Forecast For Enzymatica AB (STO:ENZY)

One thing we could say about the analysts on Enzymatica AB (STO:ENZY) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. Revenue estimates were cut sharply as analysts signalled a weaker outlook - perhaps a sign that investors should temper their expectations as well. Shares are up 8.8% to kr10.36 in the past week. We'd be curious to see if the downgrade is enough to reverse investor sentiment on the business.

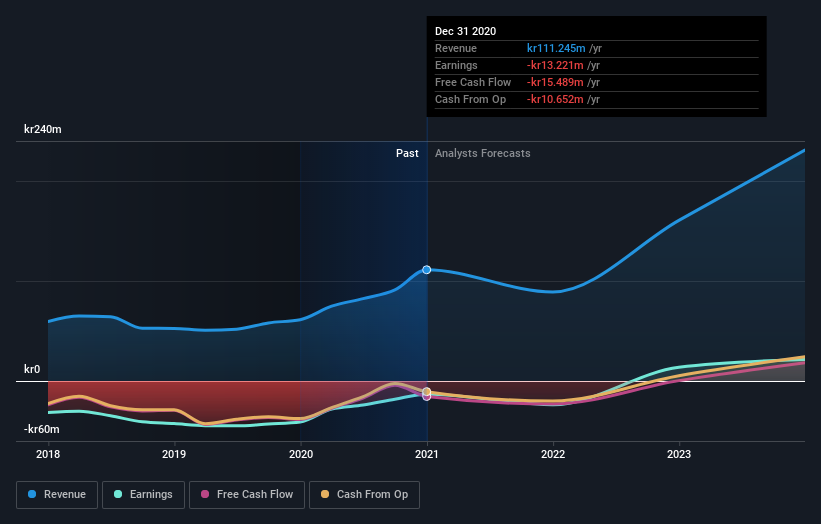

Following the latest downgrade, the current consensus, from the twin analysts covering Enzymatica, is for revenues of kr89m in 2021, which would reflect a not inconsiderable 20% reduction in Enzymatica's sales over the past 12 months. Prior to the latest estimates, the analysts were forecasting revenues of kr104m in 2021. The consensus view seems to have become more pessimistic on Enzymatica, noting the measurable cut to revenue estimates in this update.

Check out our latest analysis for Enzymatica

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 26% by the end of 2021. This indicates a significant reduction from annual growth of 22% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 26% annually for the foreseeable future. It's pretty clear that Enzymatica's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that analysts cut their revenue estimates for this year. They're also anticipating slower revenue growth than the wider market. Often, one downgrade can set off a daisy-chain of cuts, especially if an industry is in decline. So we wouldn't be surprised if the market became a lot more cautious on Enzymatica after today.

Want to learn more? We have estimates for Enzymatica from its twin analysts out until 2023, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you’re looking to trade Enzymatica, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Enzymatica might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OM:ENZY

Enzymatica

A life science company, develops and sells products that treat and alleviate infections and symptoms in the upper respiratory tract.

Excellent balance sheet moderate.