Advertisement

- Sweden

- /

- Entertainment

- /

- OM:MAXENT B

Benign Growth For Maximum Entertainment AB (STO:MAXENT B) Underpins Stock's 29% Plummet

Unfortunately for some shareholders, the Maximum Entertainment AB (STO:MAXENT B) share price has dived 29% in the last thirty days, prolonging recent pain. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 60% loss during that time.

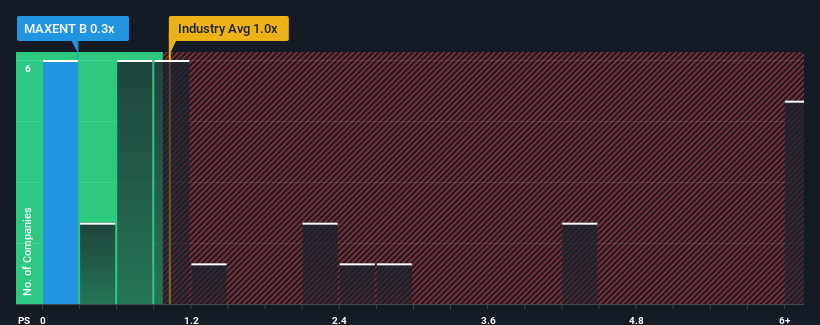

Following the heavy fall in price, it would be understandable if you think Maximum Entertainment is a stock with good investment prospects with a price-to-sales ratios (or "P/S") of 0.3x, considering almost half the companies in Sweden's Entertainment industry have P/S ratios above 1x. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Maximum Entertainment

How Has Maximum Entertainment Performed Recently?

Recent times haven't been great for Maximum Entertainment as its revenue has been rising slower than most other companies. It seems that many are expecting the uninspiring revenue performance to persist, which has repressed the growth of the P/S ratio. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Maximum Entertainment.Is There Any Revenue Growth Forecasted For Maximum Entertainment?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Maximum Entertainment's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 35%. The latest three year period has also seen an incredible overall rise in revenue, aided by its incredible short-term performance. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Turning to the outlook, the next year should bring diminished returns, with revenue decreasing 2.3% as estimated by the two analysts watching the company. With the industry predicted to deliver 14% growth, that's a disappointing outcome.

In light of this, it's understandable that Maximum Entertainment's P/S would sit below the majority of other companies. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Bottom Line On Maximum Entertainment's P/S

The southerly movements of Maximum Entertainment's shares means its P/S is now sitting at a pretty low level. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Maximum Entertainment's analyst forecasts revealed that its outlook for shrinking revenue is contributing to its low P/S. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

It is also worth noting that we have found 5 warning signs for Maximum Entertainment that you need to take into consideration.

If these risks are making you reconsider your opinion on Maximum Entertainment, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:MAXENT B

Maximum Entertainment

An entertainment company, engages in the development, publishing, transmedia, sale, and operation of video games in North America, Europe, Asia, and internationally.

Mediocre balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor