Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Bergs Timber AB (publ) (STO:BRG B) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Bergs Timber

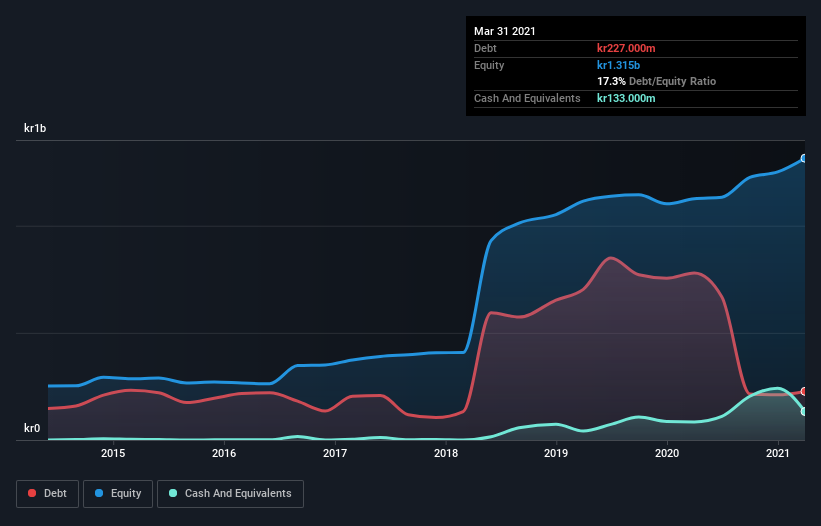

What Is Bergs Timber's Debt?

You can click the graphic below for the historical numbers, but it shows that Bergs Timber had kr226.0m of debt in March 2021, down from kr779.0m, one year before. However, it does have kr133.0m in cash offsetting this, leading to net debt of about kr93.0m.

How Strong Is Bergs Timber's Balance Sheet?

We can see from the most recent balance sheet that Bergs Timber had liabilities of kr316.0m falling due within a year, and liabilities of kr196.0m due beyond that. Offsetting these obligations, it had cash of kr133.0m as well as receivables valued at kr372.0m due within 12 months. So these liquid assets roughly match the total liabilities.

Having regard to Bergs Timber's size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the kr1.92b company is short on cash, but still worth keeping an eye on the balance sheet.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Looking at its net debt to EBITDA of 0.38 and interest cover of 4.6 times, it seems to us that Bergs Timber is probably using debt in a pretty reasonable way. So we'd recommend keeping a close eye on the impact financing costs are having on the business. Notably, Bergs Timber's EBIT launched higher than Elon Musk, gaining a whopping 785% on last year. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Bergs Timber's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Bergs Timber recorded free cash flow worth 55% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

The good news is that Bergs Timber's demonstrated ability to grow its EBIT delights us like a fluffy puppy does a toddler. But truth be told we feel its interest cover does undermine this impression a bit. Looking at the bigger picture, we think Bergs Timber's use of debt seems quite reasonable and we're not concerned about it. After all, sensible leverage can boost returns on equity. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example Bergs Timber has 3 warning signs (and 1 which is concerning) we think you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you’re looking to trade Bergs Timber, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Bergs Timber might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OM:BRG B

Bergs Timber

Bergs Timber AB (publ) engages in development, production, and marketing of processed wood products in Sweden, Latvia, the United Kingdom, and internationally.

Undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor