As global markets experience varied shifts, with European indices showing modest gains amid hopes of economic stimulus and interest rate cuts, the Swedish market remains a focal point for investors seeking growth opportunities. In this context, insider ownership can be an important indicator of confidence in a company's potential, making it a key factor to consider when evaluating growth stocks in Sweden.

Top 10 Growth Companies With High Insider Ownership In Sweden

| Name | Insider Ownership | Earnings Growth |

| CTT Systems (OM:CTT) | 16.9% | 24.8% |

| Truecaller (OM:TRUE B) | 29.7% | 21.7% |

| Magle Chemoswed Holding (OM:MAGLE) | 14.9% | 72.2% |

| Biovica International (OM:BIOVIC B) | 18.3% | 78.5% |

| BioArctic (OM:BIOA B) | 34% | 98.4% |

| Yubico (OM:YUBICO) | 37.5% | 42.2% |

| KebNi (OM:KEBNI B) | 36.3% | 86.1% |

| InCoax Networks (OM:INCOAX) | 20.1% | 115.5% |

| C-Rad (OM:CRAD B) | 16.1% | 33.9% |

| OrganoClick (OM:ORGC) | 23.1% | 109.0% |

Let's review some notable picks from our screened stocks.

EQT (OM:EQT)

Simply Wall St Growth Rating: ★★★★★☆

Overview: EQT AB (publ) is a global private equity firm focusing on private capital and real asset segments, with a market cap of SEK392.56 billion.

Operations: The company's revenue is primarily derived from the Private Capital segment at €1.28 billion and the Real Assets segment at €878.70 million, with an additional contribution of €37.20 million from the Central segment.

Insider Ownership: 12.3%

EQT's projected revenue growth of 15.7% annually surpasses the Swedish market average, while its earnings are expected to grow significantly at 33.7% per year. Despite no substantial insider buying recently, EQT insiders have been more active in purchasing than selling shares over the past three months. The company is actively involved in M&A activities, including bids for Singapore Post's Australian assets and exploring a sale of its Banking Circle stake valued over $2 billion.

- Click here to discover the nuances of EQT with our detailed analytical future growth report.

- Upon reviewing our latest valuation report, EQT's share price might be too optimistic.

Sectra (OM:SECT B)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Sectra AB (publ) offers medical IT and cybersecurity solutions across Sweden, the United Kingdom, the Netherlands, and other parts of Europe with a market cap of approximately SEK56.14 billion.

Operations: The company's revenue is primarily derived from its Imaging IT Solutions segment, which accounts for SEK2.67 billion, followed by Secure Communications at SEK388.55 million and Business Innovation contributing SEK90.77 million.

Insider Ownership: 30.3%

Sectra's earnings are forecast to grow significantly at 21.2% annually, outpacing the Swedish market average. Revenue growth is also expected to exceed the market, although not at a high rate. Recent first-quarter results showed increased sales and net income year-over-year. While insider transactions have been minimal recently, more shares were bought than sold in the past three months. Sectra's new agreement with MaineGeneral Health highlights its expanding presence in medical imaging IT and cybersecurity solutions.

- Click here and access our complete growth analysis report to understand the dynamics of Sectra.

- According our valuation report, there's an indication that Sectra's share price might be on the expensive side.

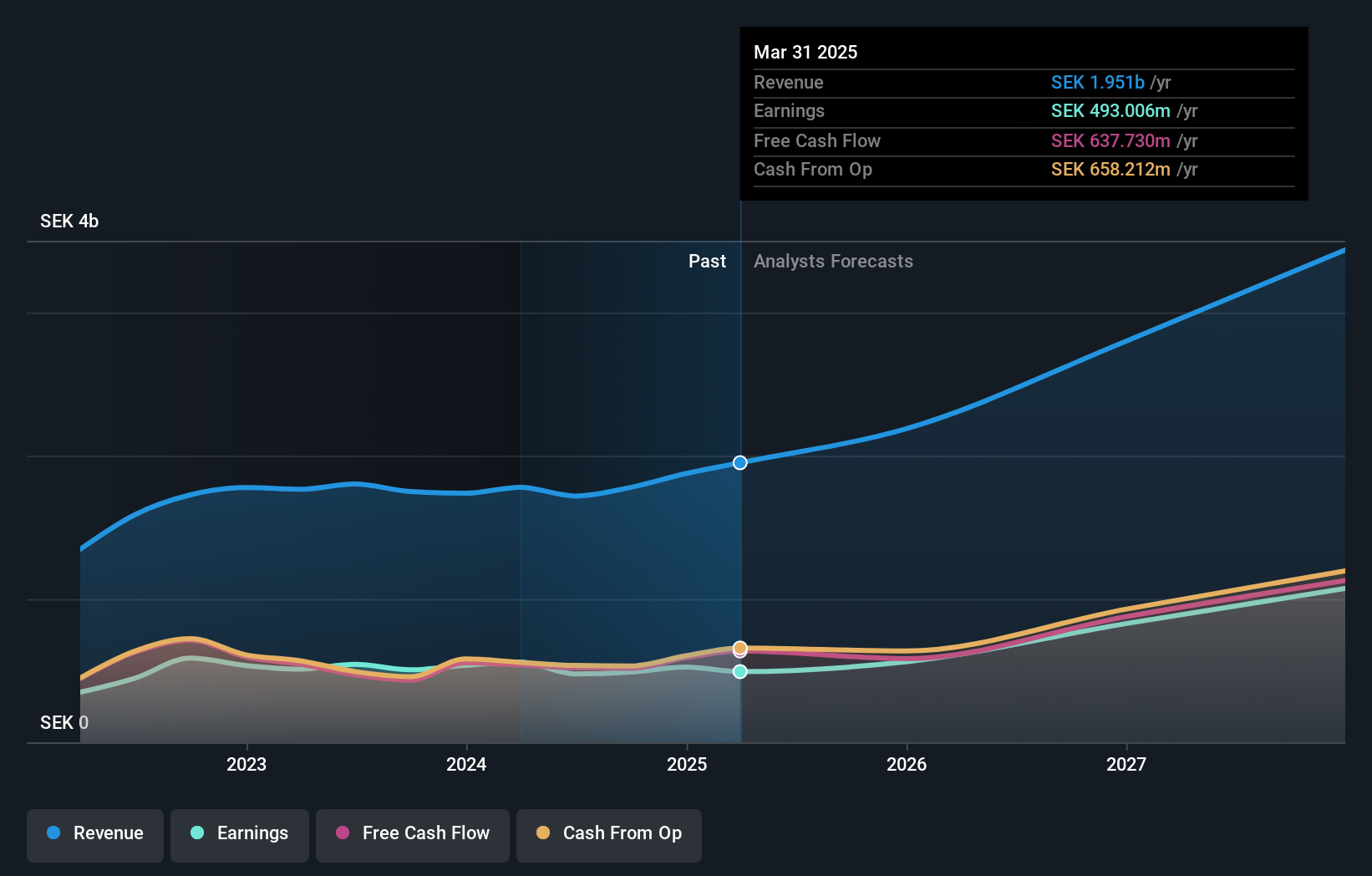

Truecaller (OM:TRUE B)

Simply Wall St Growth Rating: ★★★★★★

Overview: Truecaller AB (publ) develops and publishes mobile caller ID applications for individuals and businesses across India, the Middle East, Africa, and internationally, with a market cap of approximately SEK15.48 billion.

Operations: The company generates revenue from its communications software segment, amounting to SEK1.72 billion.

Insider Ownership: 29.7%

Truecaller is poised for robust growth, with earnings projected to increase significantly at 21.7% annually, surpassing the Swedish market average. Revenue is also expected to grow rapidly at 20.4% per year. Despite a recent decline in quarterly sales and net income, Truecaller remains undervalued by nearly half according to estimates of its fair value. Recent strategic partnerships and leadership appointments aim to bolster its position in key markets like India, enhancing regulatory compliance and customer communication solutions.

- Click to explore a detailed breakdown of our findings in Truecaller's earnings growth report.

- Our comprehensive valuation report raises the possibility that Truecaller is priced lower than what may be justified by its financials.

Seize The Opportunity

- Access the full spectrum of 81 Fast Growing Swedish Companies With High Insider Ownership by clicking on this link.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Truecaller might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:TRUE B

Truecaller

Develops and publishes mobile caller ID applications for individuals and business in India, the Middle East, Africa, and internationally.

Exceptional growth potential with flawless balance sheet.