Stock Analysis

Exploring Swedish Exchange Stocks With Intrinsic Value Discounts Up To 48.6%

Reviewed by Simply Wall St

Amid a backdrop of fluctuating global markets, Sweden's stock exchange presents a unique landscape for investors seeking value. With intrinsic value discounts reaching up to 48.6%, certain Swedish stocks appear poised for consideration, especially in a climate where discerning investment opportunities is crucial due to mixed economic signals worldwide. In this context, identifying stocks that are undervalued relative to their intrinsic worth could be particularly compelling, offering potential resilience or growth as market dynamics evolve.

Top 10 Undervalued Stocks Based On Cash Flows In Sweden

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| RVRC Holding (OM:RVRC) | SEK46.00 | SEK87.22 | 47.3% |

| Gränges (OM:GRNG) | SEK139.40 | SEK258.76 | 46.1% |

| Afry (OM:AFRY) | SEK198.40 | SEK382.28 | 48.1% |

| RaySearch Laboratories (OM:RAY B) | SEK143.40 | SEK278.89 | 48.6% |

| Nolato (OM:NOLA B) | SEK60.45 | SEK115.76 | 47.8% |

| Dometic Group (OM:DOM) | SEK70.40 | SEK130.21 | 45.9% |

| Sinch (OM:SINCH) | SEK23.29 | SEK43.46 | 46.4% |

| Flexion Mobile (OM:FLEXM) | SEK8.94 | SEK16.31 | 45.2% |

| Nordisk Bergteknik (OM:NORB B) | SEK16.80 | SEK30.78 | 45.4% |

| Image Systems (OM:IS) | SEK1.47 | SEK2.84 | 48.3% |

Let's take a closer look at a couple of our picks from the screened companies.

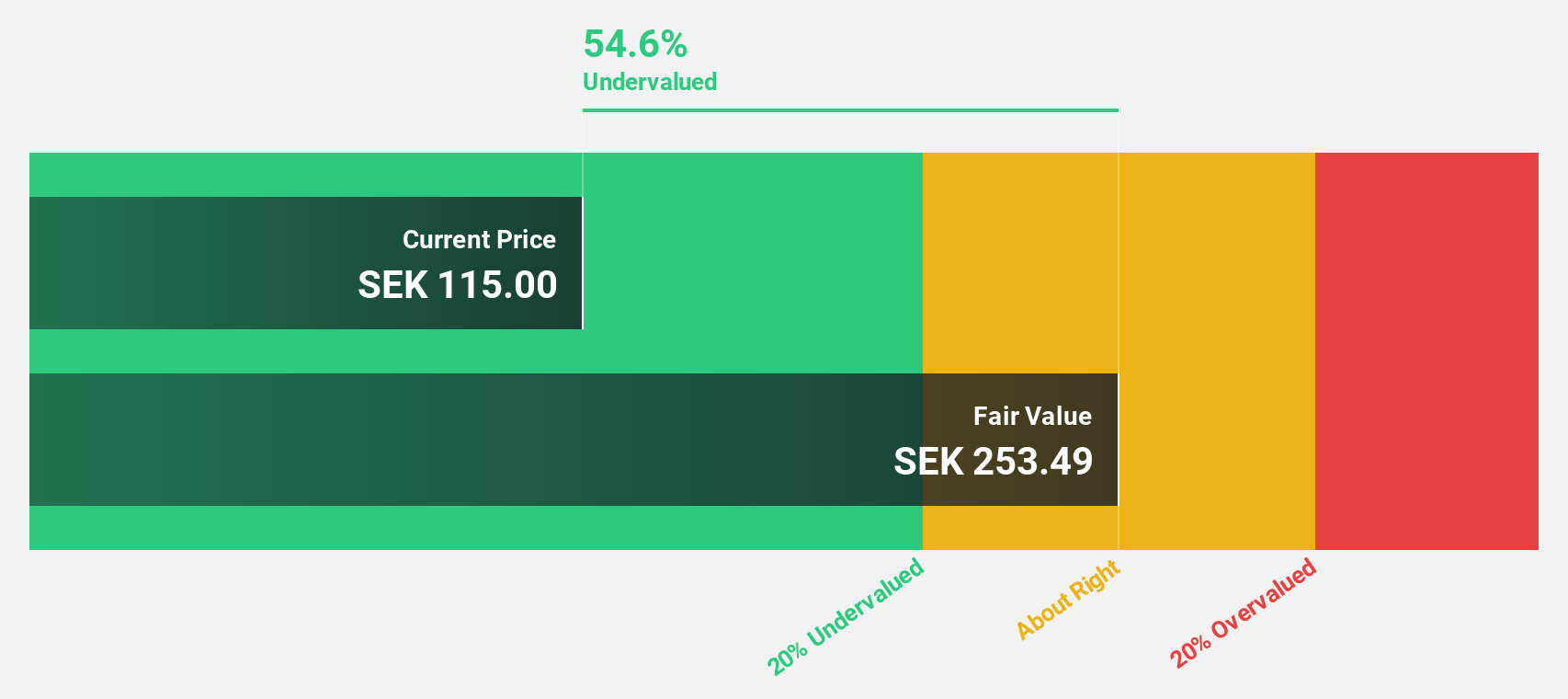

Ependion (OM:EPEN)

Overview: Ependion AB, along with its subsidiaries, specializes in offering digital solutions for secure control, management, visualization, and data communication, with a market capitalization of approximately SEK 3.46 billion.

Operations: The company specializes in digital solutions, focusing on secure control, management, visualization, and data communication.

Estimated Discount To Fair Value: 42%

Ependion, priced at SEK119, significantly under its fair value of SEK205.07, shows a promising investment profile based on cash flows. Despite a high debt level, it's expected to outperform with earnings growth forecasted at 22.8% annually over the next three years—higher than the Swedish market average. Recent financials reveal a dip in sales and net income for the first half of 2024; however, its strategic moves like significant orders from Siemens for Indian Railways indicate potential revenue streams ahead.

- Our expertly prepared growth report on Ependion implies its future financial outlook may be stronger than recent results.

- Delve into the full analysis health report here for a deeper understanding of Ependion.

Humble Group (OM:HUMBLE)

Overview: Humble Group AB operates in the refinement, development, and distribution of fast-moving consumer goods both in Sweden and internationally, with a market capitalization of approximately SEK 4.29 billion.

Operations: The company generates revenue through four primary segments: Future Snacking (SEK 935 million), Sustainable Care (SEK 2.24 billion), Quality Nutrition (SEK 1.51 billion), and Nordic Distribution (SEK 2.62 billion).

Estimated Discount To Fair Value: 39.7%

Humble Group, priced at SEK9.68, is significantly below the estimated fair value of SEK16.06, suggesting strong undervaluation based on cash flows. While its revenue growth forecast at 11% per year is robust compared to the Swedish market's 1.7%, its projected profitability and earnings growth are also promising, with earnings expected to increase substantially annually. However, a low forecasted return on equity of 8.7% tempers this optimism slightly. Recent credit facility expansions totaling SEK300 million could support further growth or operational flexibility.

- Our growth report here indicates Humble Group may be poised for an improving outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Humble Group.

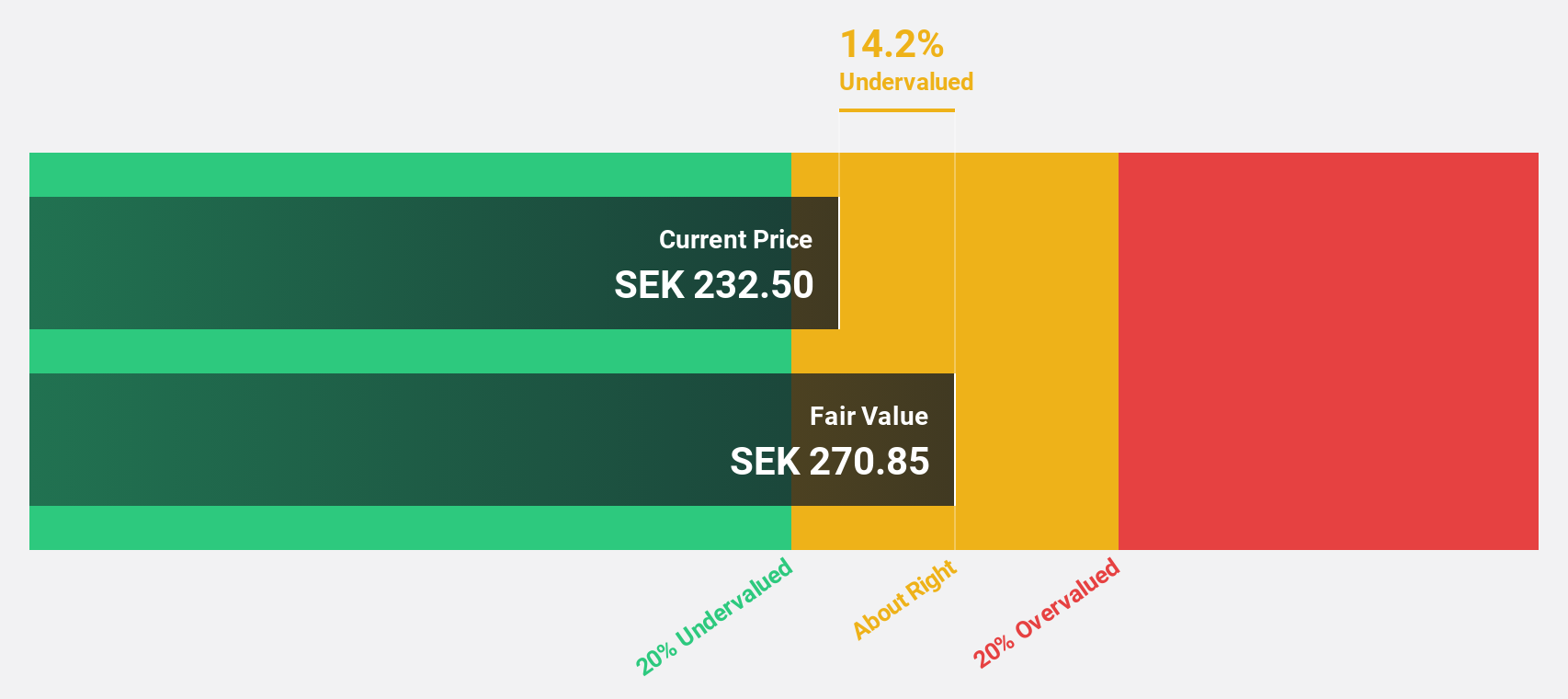

RaySearch Laboratories (OM:RAY B)

Overview: RaySearch Laboratories AB is a medical technology company specializing in software solutions for cancer care across the Americas, Europe, Africa, the Asia-Pacific, and the Middle East, with a market capitalization of approximately SEK 4.92 billion.

Operations: The company generates its revenue primarily from healthcare software, totaling SEK 1.05 billion.

Estimated Discount To Fair Value: 48.6%

RaySearch Laboratories, with a current price of SEK143.4, is significantly undervalued against a fair value estimate of SEK278.89, reflecting a 48.6% discount. The company's earnings have surged by 356.9% over the past year and are expected to grow by 33.62% annually, outpacing the Swedish market forecast of 15.2%. Recent innovations like RayStation® 2024B enhance clinical workflow automation, potentially boosting future revenue streams which are projected to increase by 10.6% annually.

- In light of our recent growth report, it seems possible that RaySearch Laboratories' financial performance will exceed current levels.

- Take a closer look at RaySearch Laboratories' balance sheet health here in our report.

Taking Advantage

- Click here to access our complete index of 49 Undervalued Swedish Stocks Based On Cash Flows.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Ependion is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:EPEN

Ependion

Provides digital solutions for secure control, management, visualization, and data communication.

Undervalued with reasonable growth potential.