Advertisement

- Sweden

- /

- Medical Equipment

- /

- NGM:BIOWKS

Companies Like Bio-Works Technologies (STO:BIOWKS) Are In A Position To Invest In Growth

We can readily understand why investors are attracted to unprofitable companies. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But while history lauds those rare successes, those that fail are often forgotten; who remembers Pets.com?

Given this risk, we thought we'd take a look at whether Bio-Works Technologies (STO:BIOWKS) shareholders should be worried about its cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

See our latest analysis for Bio-Works Technologies

When Might Bio-Works Technologies Run Out Of Money?

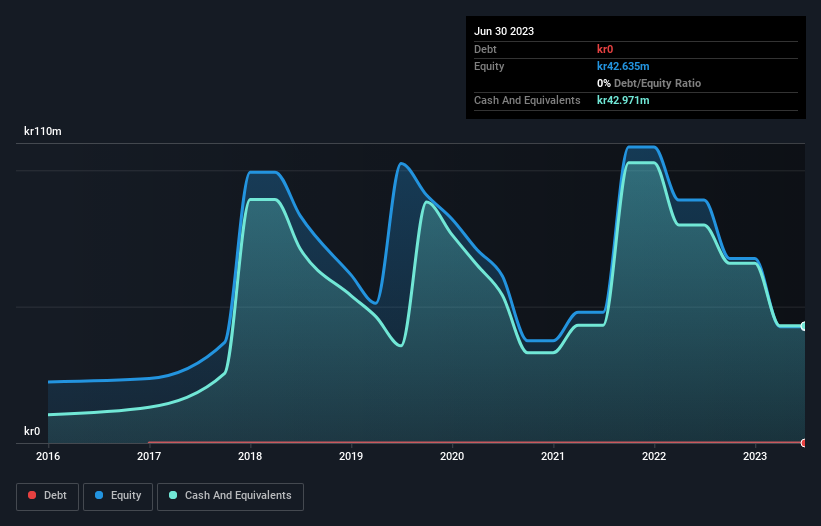

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. As at June 2023, Bio-Works Technologies had cash of kr43m and no debt. Importantly, its cash burn was kr41m over the trailing twelve months. Therefore, from June 2023 it had roughly 13 months of cash runway. Notably, one analyst forecasts that Bio-Works Technologies will break even (at a free cash flow level) in about 19 months. That means unless the company reduces its cash burn quickly, it may well look to raise more cash. You can see how its cash balance has changed over time in the image below.

How Well Is Bio-Works Technologies Growing?

Bio-Works Technologies reduced its cash burn by 18% during the last year, which points to some degree of discipline. On top of that, operating revenue was up 42%, making for a heartening combination We think it is growing rather well, upon reflection. Clearly, however, the crucial factor is whether the company will grow its business going forward. So you might want to take a peek at how much the company is expected to grow in the next few years.

How Hard Would It Be For Bio-Works Technologies To Raise More Cash For Growth?

Bio-Works Technologies seems to be in a fairly good position, in terms of cash burn, but we still think it's worthwhile considering how easily it could raise more money if it wanted to. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of kr350m, Bio-Works Technologies' kr41m in cash burn equates to about 12% of its market value. Given that situation, it's fair to say the company wouldn't have much trouble raising more cash for growth, but shareholders would be somewhat diluted.

So, Should We Worry About Bio-Works Technologies' Cash Burn?

As you can probably tell by now, we're not too worried about Bio-Works Technologies' cash burn. For example, we think its revenue growth suggests that the company is on a good path. Its weak point is its cash runway, but even that wasn't too bad! It's clearly very positive to see that at least one analyst is forecasting the company will break even fairly soon. Looking at all the measures in this article, together, we're not worried about its rate of cash burn; the company seems well on top of its medium-term spending needs. Taking an in-depth view of risks, we've identified 3 warning signs for Bio-Works Technologies that you should be aware of before investing.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

Valuation is complex, but we're here to simplify it.

Discover if Bio-Works Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NGM:BIOWKS

Bio-Works Technologies

A biotechnology company, engages in the research, development, manufacture, and supply of agarose-based separation products to purify proteins, enzymes, antibodies, peptides, and other biomolecules primarily in Sweden.

Medium-low risk with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor