Advertisement

These 4 Measures Indicate That Kopparbergs Bryggeri (NGM:KOBR B) Is Using Debt Safely

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Kopparbergs Bryggeri AB (publ) (NGM:KOBR B) makes use of debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Kopparbergs Bryggeri

What Is Kopparbergs Bryggeri's Debt?

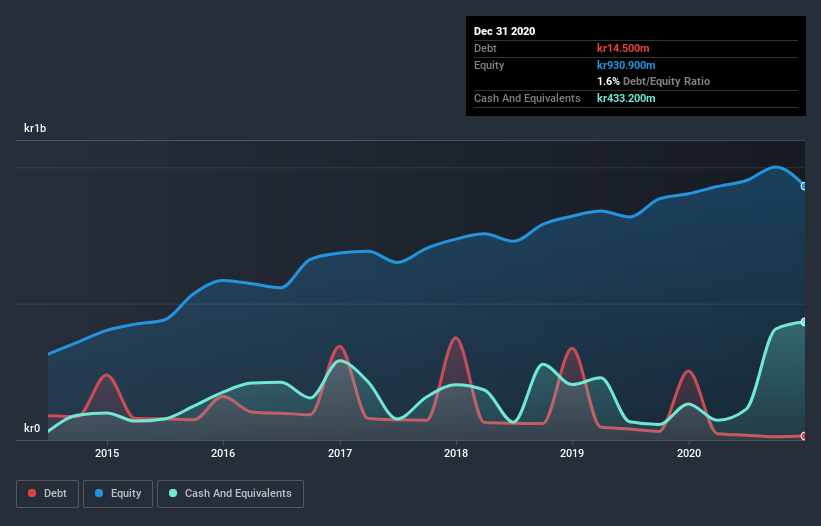

You can click the graphic below for the historical numbers, but it shows that Kopparbergs Bryggeri had kr14.5m of debt in December 2020, down from kr252.8m, one year before. But it also has kr433.2m in cash to offset that, meaning it has kr418.7m net cash.

How Strong Is Kopparbergs Bryggeri's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Kopparbergs Bryggeri had liabilities of kr927.4m due within 12 months and liabilities of kr47.5m due beyond that. Offsetting this, it had kr433.2m in cash and kr528.8m in receivables that were due within 12 months. So these liquid assets roughly match the total liabilities.

This state of affairs indicates that Kopparbergs Bryggeri's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the kr3.71b company is struggling for cash, we still think it's worth monitoring its balance sheet. Despite its noteworthy liabilities, Kopparbergs Bryggeri boasts net cash, so it's fair to say it does not have a heavy debt load!

The good news is that Kopparbergs Bryggeri has increased its EBIT by 8.9% over twelve months, which should ease any concerns about debt repayment. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Kopparbergs Bryggeri will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. Kopparbergs Bryggeri may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, Kopparbergs Bryggeri actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Kopparbergs Bryggeri has kr418.7m in net cash. The cherry on top was that in converted 105% of that EBIT to free cash flow, bringing in kr296m. So we don't think Kopparbergs Bryggeri's use of debt is risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 2 warning signs for Kopparbergs Bryggeri (1 is a bit unpleasant!) that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you’re looking to trade Kopparbergs Bryggeri, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Kopparbergs Bryggeri might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NGM:KOBR B

Kopparbergs Bryggeri

Manufactures, distributes, and sells beer, cider, wine, spirits, soft drinks, and water in Sweden and internationally.

Flawless balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor