Advertisement

The board of EQT AB (publ) (STO:EQT) has announced that it will be paying its dividend of €2.15 on the 4th of June, an increased payment from last year's comparable dividend. Although the dividend is now higher, the yield is only 1.5%, which is below the industry average.

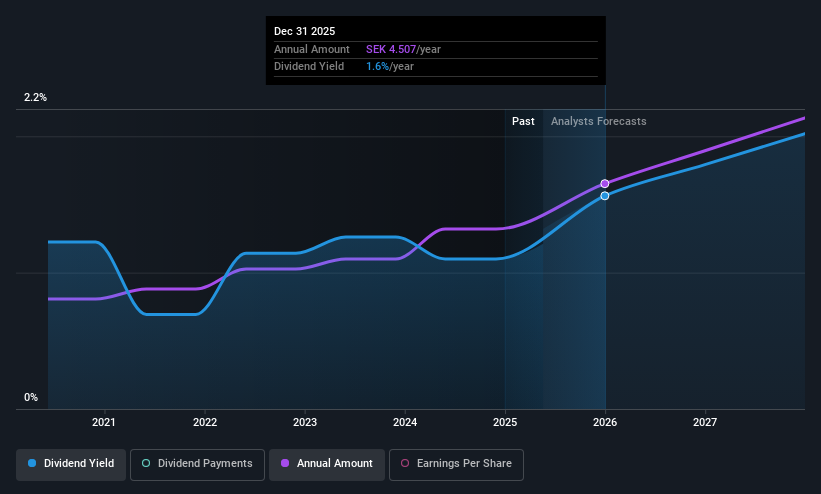

We check all companies for important risks. See what we found for EQT in our free report.EQT's Projections Indicate Future Payments May Be Unsustainable

Even a low dividend yield can be attractive if it is sustained for years on end. Based on the last dividend, EQT is earning enough to cover the payment, but then it makes up 103% of cash flows. While the company may be more focused on returning cash to shareholders than growing the business at this time, we think that a cash payout ratio this high might expose the dividend to being cut if the business ran into some challenges.

Earnings per share is forecast to rise by 148.7% over the next year. If the dividend continues on its recent course, the company could be paying out several times what it earns in the next 12 months, which could start applying pressure to the balance sheet.

View our latest analysis for EQT

EQT's Dividend Has Lacked Consistency

EQT has been paying dividends for a while, but the track record isn't stellar. This makes us cautious about the consistency of the dividend over a full economic cycle. Since 2020, the dividend has gone from €0.206 total annually to €0.386. This works out to be a compound annual growth rate (CAGR) of approximately 13% a year over that time. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. EQT has seen EPS rising for the last five years, at 30% per annum. EQT is clearly able to grow rapidly while still returning cash to shareholders, positioning it to become a strong dividend payer in the future.

Our Thoughts On EQT's Dividend

Overall, we always like to see the dividend being raised, but we don't think EQT will make a great income stock. While EQT is earning enough to cover the payments, the cash flows are lacking. Overall, we don't think this company has the makings of a good income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. Earnings growth generally bodes well for the future value of company dividend payments. See if the 13 EQT analysts we track are forecasting continued growth with our free report on analyst estimates for the company. Is EQT not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if EQT might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:EQT

EQT

A global private equity & venture capital firm specializing in private capital and real asset segments.

High growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor