Advertisement

- Sweden

- /

- Hospitality

- /

- OM:ACROUD

Why We're Not Concerned Yet About Acroud AB (publ)'s (STO:ACROUD) 31% Share Price Plunge

The Acroud AB (publ) (STO:ACROUD) share price has fared very poorly over the last month, falling by a substantial 31%. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 69% loss during that time.

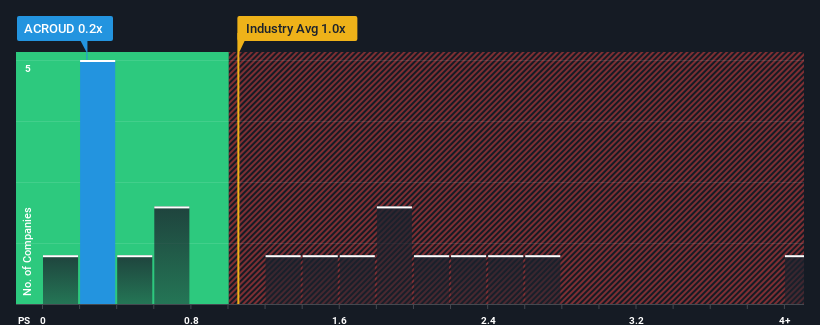

Even after such a large drop in price, you could still be forgiven for feeling indifferent about Acroud's P/S ratio of 0.2x, since the median price-to-sales (or "P/S") ratio for the Hospitality industry in Sweden is also close to 0.7x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for Acroud

How Has Acroud Performed Recently?

Recent times haven't been great for Acroud as its revenue has been rising slower than most other companies. It might be that many expect the uninspiring revenue performance to strengthen positively, which has kept the P/S ratio from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Want the full picture on analyst estimates for the company? Then our free report on Acroud will help you uncover what's on the horizon.Is There Some Revenue Growth Forecasted For Acroud?

In order to justify its P/S ratio, Acroud would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered a decent 6.7% gain to the company's revenues. The latest three year period has also seen an excellent 133% overall rise in revenue, aided somewhat by its short-term performance. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Turning to the outlook, the next year should generate growth of 12% as estimated by the one analyst watching the company. That's shaping up to be similar to the 14% growth forecast for the broader industry.

In light of this, it's understandable that Acroud's P/S sits in line with the majority of other companies. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

What We Can Learn From Acroud's P/S?

With its share price dropping off a cliff, the P/S for Acroud looks to be in line with the rest of the Hospitality industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

A Acroud's P/S seems about right to us given the knowledge that analysts are forecasting a revenue outlook that is similar to the Hospitality industry. Right now shareholders are comfortable with the P/S as they are quite confident future revenue won't throw up any surprises. All things considered, if the P/S and revenue estimates contain no major shocks, then it's hard to see the share price moving strongly in either direction in the near future.

You need to take note of risks, for example - Acroud has 2 warning signs (and 1 which is concerning) we think you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:ACROUD

Acroud

Engages in the development and operation of Software as a Service (SaaS) solutions in Sweden.

Adequate balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor