Advertisement

- Sweden

- /

- Hospitality

- /

- OM:ACROUD

Acroud AB (publ) (STO:ACROUD) Looks Inexpensive But Perhaps Not Attractive Enough

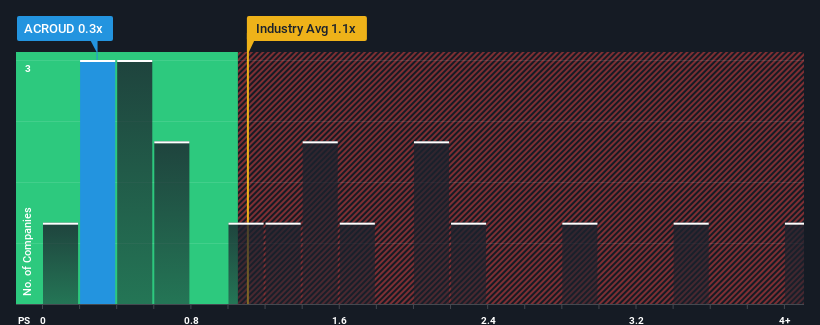

When you see that almost half of the companies in the Hospitality industry in Sweden have price-to-sales ratios (or "P/S") above 0.9x, Acroud AB (publ) (STO:ACROUD) looks to be giving off some buy signals with its 0.3x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

View our latest analysis for Acroud

What Does Acroud's Recent Performance Look Like?

With revenue growth that's superior to most other companies of late, Acroud has been doing relatively well. One possibility is that the P/S ratio is low because investors think this strong revenue performance might be less impressive moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Keen to find out how analysts think Acroud's future stacks up against the industry? In that case, our free report is a great place to start.Is There Any Revenue Growth Forecasted For Acroud?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Acroud's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 27% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 238% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenue over that time.

Turning to the outlook, the next three years should generate growth of 3.8% per annum as estimated by the only analyst watching the company. That's shaping up to be materially lower than the 80% each year growth forecast for the broader industry.

With this information, we can see why Acroud is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Acroud maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. It's hard to see the share price rising strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 3 warning signs for Acroud that you should be aware of.

If these risks are making you reconsider your opinion on Acroud, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:ACROUD

Acroud

Engages in the development and operation of Software as a Service (SaaS) solutions in Sweden.

Adequate balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor