Afry And Two More Swedish Exchange Stocks Considered Below Estimated Intrinsic Values

Reviewed by Simply Wall St

As global markets navigate through a period of heightened volatility and economic uncertainty, Sweden's stock market presents a unique landscape for investors seeking value. In particular, certain Swedish stocks appear to be trading below their estimated intrinsic values, offering potential opportunities in an otherwise cautious investment climate. This context sets the stage for exploring undervalued stocks such as Afry, which may benefit from strategic positioning amid current market conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Sweden

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| RVRC Holding (OM:RVRC) | SEK44.70 | SEK87.56 | 49% |

| Afry (OM:AFRY) | SEK199.20 | SEK396.20 | 49.7% |

| Nordic Waterproofing Holding (OM:NWG) | SEK160.60 | SEK307.64 | 47.8% |

| edyoutec (NGM:EDYOU) | SEK0.535 | SEK1.06 | 49.6% |

| Dometic Group (OM:DOM) | SEK69.05 | SEK130.59 | 47.1% |

| Nolato (OM:NOLA B) | SEK60.25 | SEK118.63 | 49.2% |

| Stille (OM:STIL) | SEK206.00 | SEK395.47 | 47.9% |

| Biotage (OM:BIOT) | SEK169.60 | SEK318.76 | 46.8% |

| Nordisk Bergteknik (OM:NORB B) | SEK16.88 | SEK31.00 | 45.6% |

| Image Systems (OM:IS) | SEK1.535 | SEK2.86 | 46.2% |

Here's a peek at a few of the choices from the screener.

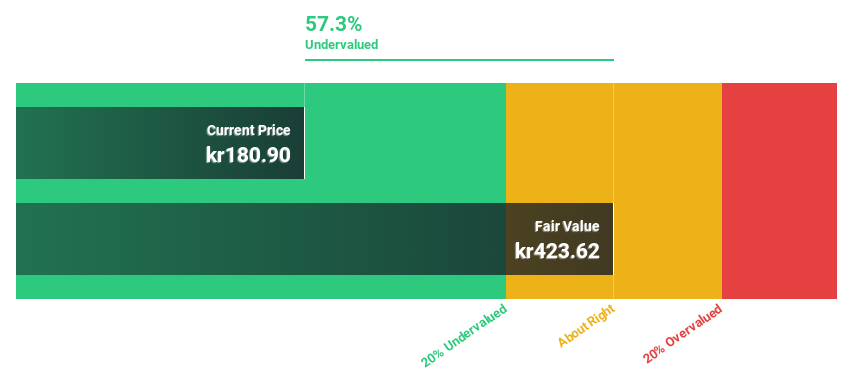

Afry (OM:AFRY)

Overview: Afry AB is a company that offers engineering, design, and advisory services across various sectors including infrastructure, industry, energy, and digitalization in regions such as North and South America, Finland, and Central Europe; it has a market capitalization of approximately SEK 22.56 billion.

Operations: Afry's revenue is derived from several key sectors: Infrastructure contributes SEK 10.26 billion, Process Industries add SEK 5.53 billion, Energy brings in SEK 3.59 billion, Management Consulting generates SEK 1.63 billion, and Industrial & Digital Solutions account for SEk 6.77 billion.

Estimated Discount To Fair Value: 49.7%

Afry, priced at SEK 199.2, is notably undervalued based on discounted cash flow analysis, with a fair value estimated at SEK 396.2, reflecting a nearly 50% discount. Despite slower revenue growth projections of 4.9% annually—above Sweden's average of 1.8%—its earnings are expected to surge by approximately 21% yearly, outpacing the Swedish market forecast of 14.7%. However, concerns linger over its unstable dividend history and modestly projected return on equity of about 12.4%.

- Our expertly prepared growth report on Afry implies its future financial outlook may be stronger than recent results.

- Get an in-depth perspective on Afry's balance sheet by reading our health report here.

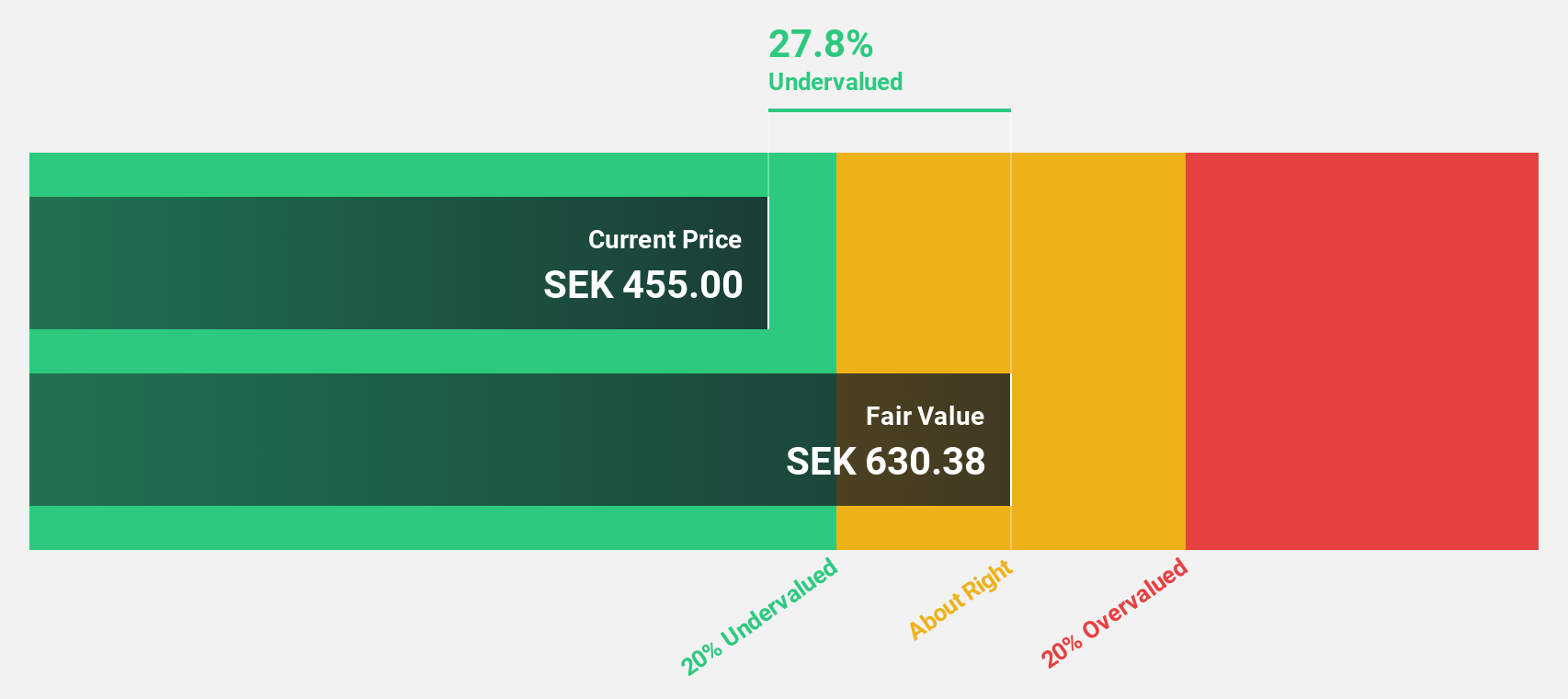

Mips (OM:MIPS)

Overview: Mips AB (publ) specializes in developing, manufacturing, and selling helmet-based safety systems across North America, Europe, Sweden, Asia, and Australia with a market capitalization of SEK 10.87 billion.

Operations: The company generates SEK 352 million in revenue from its sporting goods segment.

Estimated Discount To Fair Value: 21.6%

Mips, with a current price of SEK 410.2, appears undervalued by over 20% against a fair value estimate of SEK 523.1 based on discounted cash flow metrics. The company's earnings are expected to grow at an impressive rate of about 49.6% annually, significantly outpacing the Swedish market forecast of 14.7%. Despite recent declines in quarterly sales and net income, Mips maintains robust long-term revenue growth projections at around 30% per year and anticipates a high return on equity of approximately 33.8% in three years' time. However, its dividend coverage is weak, reflecting potential sustainability issues with its payout ratio.

- The growth report we've compiled suggests that Mips' future prospects could be on the up.

- Unlock comprehensive insights into our analysis of Mips stock in this financial health report.

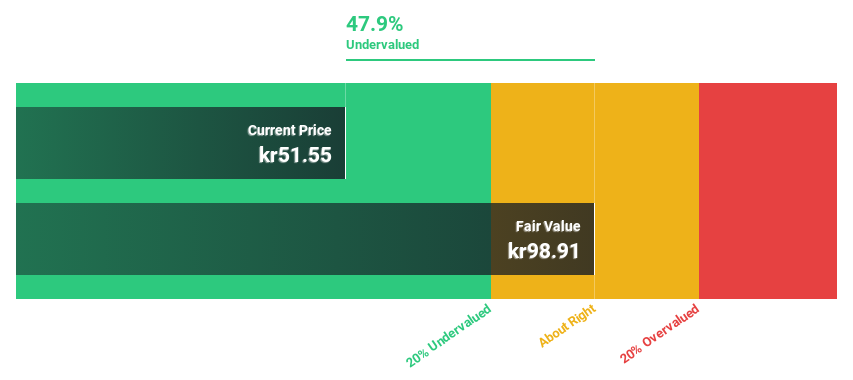

Nolato (OM:NOLA B)

Overview: Nolato AB is a global developer and manufacturer of plastic, silicone, and thermoplastic elastomer products serving various sectors including medical technology, pharmaceuticals, consumer electronics, and automotive, with a market capitalization of SEK 16.23 billion.

Operations: The revenue for the Medical Solutions segment is SEK 5.34 billion.

Estimated Discount To Fair Value: 49.2%

Nolato is currently priced at SEK 60.25, significantly below the DCF-derived fair value of SEK 118.63, indicating a substantial undervaluation. The company's earnings are projected to increase by 22.75% annually over the next three years, surpassing the Swedish market's growth rate of 14.7%. However, its forecasted revenue growth at 6.1% per year is modest compared to its earnings growth potential and the dividend coverage by free cash flows remains weak, casting some concerns on sustainability despite strong profitability indicators like a future ROE of 14.4%. Recent corporate activities include a dividend decrease and leadership changes which could impact future performance dynamics.

- According our earnings growth report, there's an indication that Nolato might be ready to expand.

- Dive into the specifics of Nolato here with our thorough financial health report.

Taking Advantage

- Explore the 46 names from our Undervalued Swedish Stocks Based On Cash Flows screener here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:MIPS

Mips

Develops, manufactures, and sells helmet-based safety systems in North America, Europe, Sweden, Asia, and Australia.

Exceptional growth potential with flawless balance sheet.