Advertisement

Norion Bank (OM:NORION): Assessing Valuation After SEK 500m Share Buyback Announcement

Simply Wall St

Reviewed by Simply Wall St

Norion Bank (OM:NORION) has announced a new share buyback program, with plans to repurchase up to SEK 500 million of its shares. This move is intended to return surplus capital to shareholders and optimize the bank’s capital structure.

See our latest analysis for Norion Bank.

Norion Bank’s share price has displayed remarkable momentum, climbing 2.75% in the last day and an impressive 86.58% year-to-date. Investors who have held shares for three years have seen a total shareholder return of 166%. With the buyback program now in play, the positive sentiment that has driven recent gains could receive another boost as the bank continues to refine its capital strategy.

If this kind of capital move has you wondering what other opportunities might be out there, it’s a great time to broaden your search and discover fast growing stocks with high insider ownership

But with Norion Bank’s shares already up sharply this year and now trading just above analyst targets, the key question becomes whether there is real value left to unlock or if future growth is fully priced in.

Price-to-Earnings of 9.8x: Is it justified?

Norion Bank is trading at a price-to-earnings (P/E) ratio of 9.8, putting its valuation below the peer average and suggesting the shares may be attractively priced against similar banks. With a last close price of SEK 70.9 and the P/E multiple below the typical sector benchmark, the market appears to be giving Norion little credit for its recent profit growth.

The price-to-earnings ratio reflects how much investors are paying for each unit of annual earnings. For banks like Norion, this ratio is crucial because it speaks to how the market values both current profitability and expectations for future earnings growth. A lower P/E can sometimes signal investor caution about ongoing earnings momentum.

Compared to other European banks, Norion’s P/E of 9.8x is just below the industry average of 9.9x. It also trades well below the peer group average of 13.7x. Notably, regression-based fair value analysis suggests a fair P/E for Norion would be 10.4x, indicating the share price could have room to rise if investor sentiment strengthens.

Explore the SWS fair ratio for Norion Bank

Result: Price-to-Earnings of 9.8x (UNDERVALUED)

However, slower net income growth or a pullback in investor sentiment could present challenges to the current valuation and affect Norion Bank’s share price trajectory.

Find out about the key risks to this Norion Bank narrative.

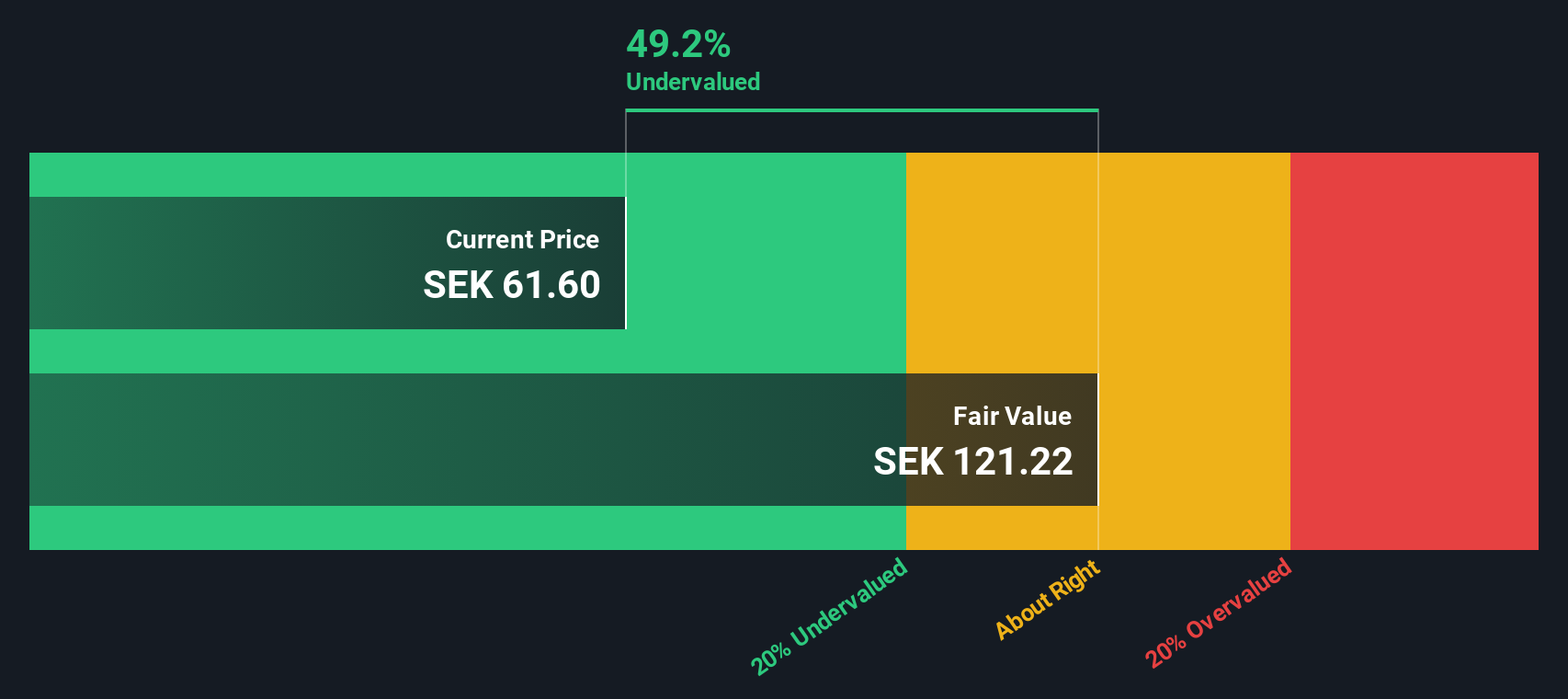

Another View: SWS DCF Model Suggests More Upside

Looking at Norion Bank from a different angle, our SWS DCF model estimates the bank’s fair value at SEK 121.09 per share, far above the recent market price. This method measures expected future cash flows and signals Norion could be deeply undervalued if the model’s assumptions prove reliable. Can the bank’s fundamentals really support such a large gap, or is the market right to stay cautious?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Norion Bank for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 840 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Norion Bank Narrative

If you want to put the numbers to the test yourself or shape your own conclusions, you can build your own analysis in just a few minutes with Do it your way

A great starting point for your Norion Bank research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Ready to power up your portfolio? Don’t let great opportunities slip through your fingers. Use the Simply Wall Street Screener to spot unique investments others might overlook.

- Unlock the potential of quantum computing by checking out these 28 quantum computing stocks. See which companies are driving innovation beyond traditional tech boundaries.

- Boost your income with these 22 dividend stocks with yields > 3%, featuring stocks offering attractive yields well above 3% for steady returns.

- Tap into tomorrow’s breakthroughs by focusing on these 26 AI penny stocks, which are harnessing artificial intelligence and reshaping entire industries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Norion Bank might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:NORION

Norion Bank

Provides financial solutions for medium-sized corporates and real estate companies, merchants, and private individuals in Sweden, Germany, Norway, Denmark, Finland, and internationally.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor