Advertisement

- Saudi Arabia

- /

- Gas Utilities

- /

- SASE:9516

Slowing Rates Of Return At Natural Gas Distribution (TADAWUL:9516) Leave Little Room For Excitement

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Although, when we looked at Natural Gas Distribution (TADAWUL:9516), it didn't seem to tick all of these boxes.

Return On Capital Employed (ROCE): What Is It?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Natural Gas Distribution:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.065 = ر.س4.2m ÷ (ر.س94m - ر.س30m) (Based on the trailing twelve months to June 2023).

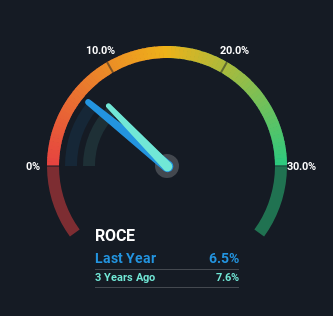

So, Natural Gas Distribution has an ROCE of 6.5%. In absolute terms, that's a low return and it also under-performs the Gas Utilities industry average of 8.3%.

Check out our latest analysis for Natural Gas Distribution

Historical performance is a great place to start when researching a stock so above you can see the gauge for Natural Gas Distribution's ROCE against it's prior returns. If you want to delve into the historical earnings, revenue and cash flow of Natural Gas Distribution, check out these free graphs here.

What Can We Tell From Natural Gas Distribution's ROCE Trend?

Things have been pretty stable at Natural Gas Distribution, with its capital employed and returns on that capital staying somewhat the same for the last five years. This tells us the company isn't reinvesting in itself, so it's plausible that it's past the growth phase. So don't be surprised if Natural Gas Distribution doesn't end up being a multi-bagger in a few years time.

On another note, while the change in ROCE trend might not scream for attention, it's interesting that the current liabilities have actually gone up over the last five years. This is intriguing because if current liabilities hadn't increased to 32% of total assets, this reported ROCE would probably be less than6.5% because total capital employed would be higher.The 6.5% ROCE could be even lower if current liabilities weren't 32% of total assets, because the the formula would show a larger base of total capital employed. With that in mind, just be wary if this ratio increases in the future, because if it gets particularly high, this brings with it some new elements of risk.

Our Take On Natural Gas Distribution's ROCE

We can conclude that in regards to Natural Gas Distribution's returns on capital employed and the trends, there isn't much change to report on. And in the last year, the stock has given away 24% so the market doesn't look too hopeful on these trends strengthening any time soon. In any case, the stock doesn't have these traits of a multi-bagger discussed above, so if that's what you're looking for, we think you'd have more luck elsewhere.

Natural Gas Distribution does come with some risks though, we found 3 warning signs in our investment analysis, and 2 of those are significant...

While Natural Gas Distribution isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Valuation is complex, but we're here to simplify it.

Discover if Natural Gas Distribution might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:9516

Natural Gas Distribution

Distributes natural gas through pipelines in Saudi Arabia.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor