- Qatar

- /

- Oil and Gas

- /

- DSM:QGTS

Returns At Qatar Gas Transport Company Limited (Nakilat) (QPSC) (DSM:QGTS) Appear To Be Weighed Down

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. In light of that, when we looked at Qatar Gas Transport Company Limited (Nakilat) (QPSC) (DSM:QGTS) and its ROCE trend, we weren't exactly thrilled.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Qatar Gas Transport Company Limited (Nakilat) (QPSC) is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

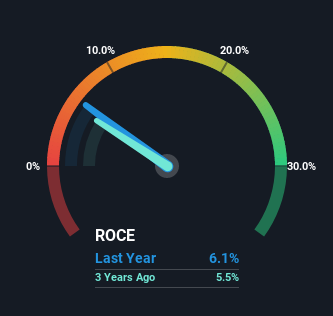

0.061 = ر.ق1.8b ÷ (ر.ق32b - ر.ق2.7b) (Based on the trailing twelve months to March 2023).

So, Qatar Gas Transport Company Limited (Nakilat) (QPSC) has an ROCE of 6.1%. Ultimately, that's a low return and it under-performs the Oil and Gas industry average of 11%.

View our latest analysis for Qatar Gas Transport Company Limited (Nakilat) (QPSC)

Above you can see how the current ROCE for Qatar Gas Transport Company Limited (Nakilat) (QPSC) compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

SWOT Analysis for Qatar Gas Transport Company Limited (Nakilat) (QPSC)

- Dividends are covered by earnings and cash flows.

- Earnings growth over the past year underperformed the Oil and Gas industry.

- Interest payments on debt are not well covered.

- Dividend is low compared to the top 25% of dividend payers in the Oil and Gas market.

- Expensive based on P/E ratio and estimated fair value.

- Annual earnings are forecast to grow for the next 3 years.

- Debt is not well covered by operating cash flow.

- Annual earnings are forecast to grow slower than the Qatari market.

What Can We Tell From Qatar Gas Transport Company Limited (Nakilat) (QPSC)'s ROCE Trend?

There hasn't been much to report for Qatar Gas Transport Company Limited (Nakilat) (QPSC)'s returns and its level of capital employed because both metrics have been steady for the past five years. It's not uncommon to see this when looking at a mature and stable business that isn't re-investing its earnings because it has likely passed that phase of the business cycle. So don't be surprised if Qatar Gas Transport Company Limited (Nakilat) (QPSC) doesn't end up being a multi-bagger in a few years time. With fewer investment opportunities, it makes sense that Qatar Gas Transport Company Limited (Nakilat) (QPSC) has been paying out a decent 54% of its earnings to shareholders. Unless businesses have highly compelling growth opportunities, they'll typically return some money to shareholders.

The Bottom Line On Qatar Gas Transport Company Limited (Nakilat) (QPSC)'s ROCE

In a nutshell, Qatar Gas Transport Company Limited (Nakilat) (QPSC) has been trudging along with the same returns from the same amount of capital over the last five years. Investors must think there's better things to come because the stock has knocked it out of the park, delivering a 194% gain to shareholders who have held over the last five years. But if the trajectory of these underlying trends continue, we think the likelihood of it being a multi-bagger from here isn't high.

If you want to continue researching Qatar Gas Transport Company Limited (Nakilat) (QPSC), you might be interested to know about the 1 warning sign that our analysis has discovered.

While Qatar Gas Transport Company Limited (Nakilat) (QPSC) may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're here to simplify it.

Discover if Qatar Gas Transport Company Limited (Nakilat) (QPSC) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DSM:QGTS

Qatar Gas Transport Company Limited (Nakilat) (QPSC)

Operates as a shipping and maritime company in Qatar.

Solid track record second-rate dividend payer.