Advertisement

- Qatar

- /

- Food and Staples Retail

- /

- DSM:MERS

Al Meera Consumer Goods Company Q.P.S.C.'s (DSM:MERS) Shares May Have Run Too Fast Too Soon

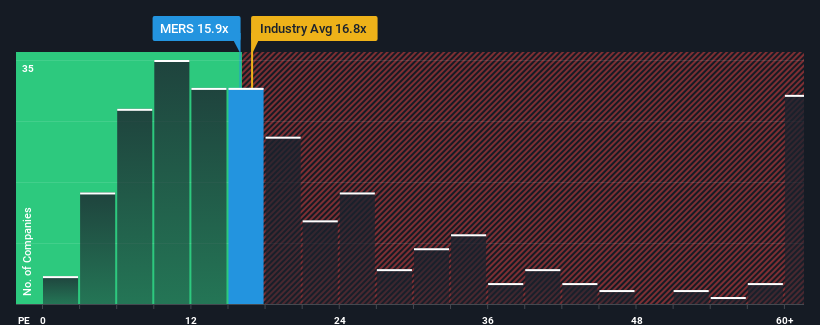

When close to half the companies in Qatar have price-to-earnings ratios (or "P/E's") below 12x, you may consider Al Meera Consumer Goods Company Q.P.S.C. (DSM:MERS) as a stock to potentially avoid with its 15.9x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

While the market has experienced earnings growth lately, Al Meera Consumer Goods Company Q.P.S.C's earnings have gone into reverse gear, which is not great. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Al Meera Consumer Goods Company Q.P.S.C

Does Growth Match The High P/E?

There's an inherent assumption that a company should outperform the market for P/E ratios like Al Meera Consumer Goods Company Q.P.S.C's to be considered reasonable.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 7.9%. As a result, earnings from three years ago have also fallen 13% overall. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Turning to the outlook, the next three years should generate growth of 9.4% each year as estimated by the two analysts watching the company. That's shaping up to be similar to the 7.7% each year growth forecast for the broader market.

With this information, we find it interesting that Al Meera Consumer Goods Company Q.P.S.C is trading at a high P/E compared to the market. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. Although, additional gains will be difficult to achieve as this level of earnings growth is likely to weigh down the share price eventually.

The Key Takeaway

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Al Meera Consumer Goods Company Q.P.S.C's analyst forecasts revealed that its market-matching earnings outlook isn't impacting its high P/E as much as we would have predicted. Right now we are uncomfortable with the relatively high share price as the predicted future earnings aren't likely to support such positive sentiment for long. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

It is also worth noting that we have found 1 warning sign for Al Meera Consumer Goods Company Q.P.S.C that you need to take into consideration.

Of course, you might also be able to find a better stock than Al Meera Consumer Goods Company Q.P.S.C. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DSM:MERS

Al Meera Consumer Goods Company Q.P.S.C

Engages in the wholesale and retail trade of various types of consumer goods commodities in Qatar and the Sultanate of Oman.

Mediocre balance sheet with concerning outlook.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|3.6% undervalued

TI

Community Contributor