Advertisement

- Portugal

- /

- Electric Utilities

- /

- ENXTLS:EDP

EDP, S.A.'s (ELI:EDP) CEO Will Probably Find It Hard To See A Huge Raise This Year

Key Insights

- EDP to hold its Annual General Meeting on 10th of April

- Total pay for CEO Miguel d' Andrade includes €1.11m salary

- Total compensation is similar to the industry average

- EDP's three-year loss to shareholders was 18% while its EPS grew by 5.0% over the past three years

In the past three years, the share price of EDP, S.A. (ELI:EDP) has struggled to grow and now shareholders are sitting on a loss. However, what is unusual is that EPS growth has been positive, suggesting that the share price has diverged from fundamentals. The AGM coming up on the 10th of April could be an opportunity for shareholders to bring these concerns to the board's attention. They could also try to influence management and firm direction through voting on resolutions such as executive remuneration and other company matters. We think shareholders might be reluctant to increase compensation for the CEO at the moment, according to our analysis below.

View our latest analysis for EDP

Comparing EDP, S.A.'s CEO Compensation With The Industry

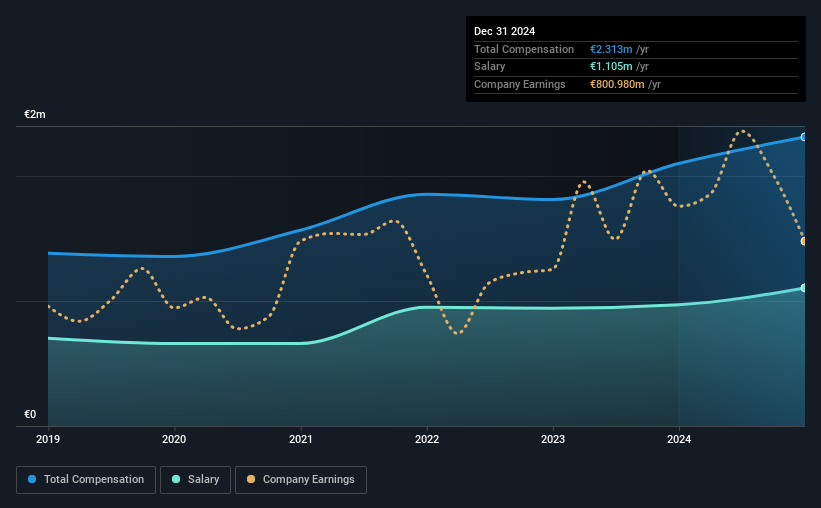

According to our data, EDP, S.A. has a market capitalization of €14b, and paid its CEO total annual compensation worth €2.3m over the year to December 2024. Notably, that's an increase of 10% over the year before. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at €1.1m.

On comparing similar companies in the Portugal Electric Utilities industry with market capitalizations above €7.3b, we found that the median total CEO compensation was €2.1m. This suggests that EDP remunerates its CEO largely in line with the industry average. What's more, Miguel d' Andrade holds €1.6m worth of shares in the company in their own name.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | €1.1m | €970k | 48% |

| Other | €1.2m | €1.1m | 52% |

| Total Compensation | €2.3m | €2.1m | 100% |

Talking in terms of the industry, salary represented approximately 52% of total compensation out of all the companies we analyzed, while other remuneration made up 48% of the pie. There isn't a significant difference between EDP and the broader market, in terms of salary allocation in the overall compensation package. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at EDP, S.A.'s Growth Numbers

EDP, S.A.'s earnings per share (EPS) grew 5.0% per year over the last three years. It saw its revenue drop 7.6% over the last year.

We would prefer it if there was revenue growth, but it is good to see a modest EPS growth at least. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings. .

Has EDP, S.A. Been A Good Investment?

Given the total shareholder loss of 18% over three years, many shareholders in EDP, S.A. are probably rather dissatisfied, to say the least. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

The fact that shareholders are sitting on a loss on the value of their shares in the past few years is certainly disconcerting. The fact that the stock price hasn't grown along with earnings may indicate that other issues may be affecting that stock. Shareholders would probably be keen to find out what are the other factors could be weighing down the stock. At the upcoming AGM, shareholders will get the opportunity to discuss any issues with the board, including those related to CEO remuneration and assess if the board's plan will likely improve performance in the future.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We've identified 2 warning signs for EDP that investors should be aware of in a dynamic business environment.

Important note: EDP is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if EDP might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTLS:EDP

EDP

Engages in the generation, transmission, distribution, and supply of electricity in Portugal, Spain, France, Poland, Romania, Italy, Belgium, the United Kingdom, Greece, Colombia, Brazil, North America, and internationally.

Second-rate dividend payer with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor