Advertisement

There May Be Underlying Issues With The Quality Of Muza's (WSE:MZA) Earnings

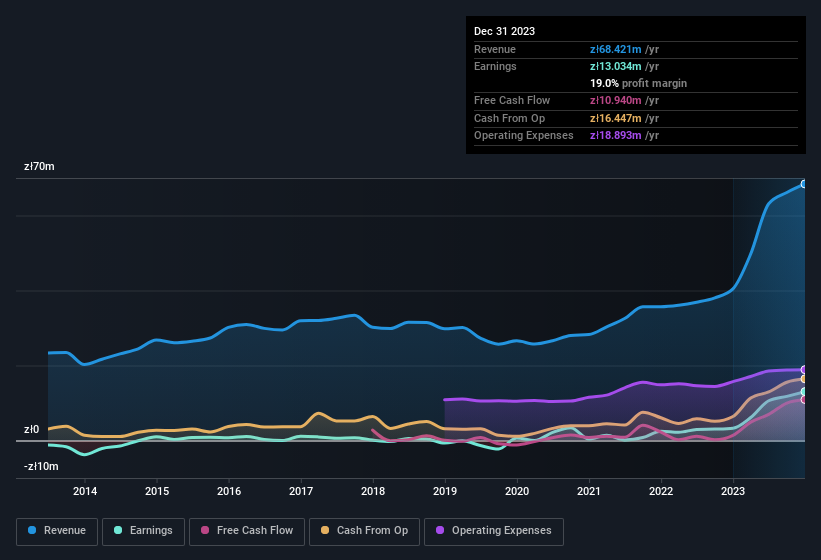

Despite posting some strong earnings, the market for Muza S.A.'s (WSE:MZA) stock hasn't moved much. Our analysis suggests that shareholders have noticed something concerning in the numbers.

See our latest analysis for Muza

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. As it happens, Muza issued 6.5% more new shares over the last year. As a result, its net income is now split between a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. Check out Muza's historical EPS growth by clicking on this link.

A Look At The Impact Of Muza's Dilution On Its Earnings Per Share (EPS)

As you can see above, Muza has been growing its net income over the last few years, with an annualized gain of 3,142% over three years. But EPS was only up 201% per year, in the exact same period. And at a glance the 297% gain in profit over the last year impresses. But in comparison, EPS only increased by 270% over the same period. Therefore, the dilution is having a noteworthy influence on shareholder returns.

In the long term, earnings per share growth should beget share price growth. So Muza shareholders will want to see that EPS figure continue to increase. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Muza.

Our Take On Muza's Profit Performance

Each Muza share now gets a meaningfully smaller slice of its overall profit, due to dilution of existing shareholders. Because of this, we think that it may be that Muza's statutory profits are better than its underlying earnings power. But on the bright side, its earnings per share have grown at an extremely impressive rate over the last three years. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. If you'd like to know more about Muza as a business, it's important to be aware of any risks it's facing. While conducting our analysis, we found that Muza has 3 warning signs and it would be unwise to ignore these.

This note has only looked at a single factor that sheds light on the nature of Muza's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:MZA

Muza

Muza S.A. publishes books in Poland. The company publishes various categories of books that include literature, crime, sensation, thriller, fiction, fantastic, non-fiction, social sciences and business, cuisine and diets, personal development, family and relationships, health, house and garden, fashion and beauty, hobby, guides, gadgets, audiobooks, history, biographies, and horror, as well as books for children and youth.

Flawless balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor