Advertisement

As we step into 2025, the global market landscape presents a mixed picture with major indices like the S&P 500 and Nasdaq Composite closing out a strong year despite recent volatility, while economic indicators such as the Chicago PMI highlight ongoing challenges in manufacturing. Against this backdrop of fluctuating market sentiment and economic signals, identifying promising small-cap stocks requires a keen eye for companies that demonstrate resilience and potential for growth amidst broader market shifts.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Resource Alam Indonesia | 2.66% | 30.36% | 43.87% | ★★★★★★ |

| Mandiri Herindo Adiperkasa | NA | 20.72% | 11.08% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Prima Andalan Mandiri | 0.94% | 20.24% | 15.28% | ★★★★★★ |

| Bank Ganesha | NA | 25.03% | 70.72% | ★★★★★★ |

| ASRock Rack Incorporation | NA | 45.76% | 269.05% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Bakrie & Brothers | 22.66% | 7.78% | 13.50% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Bhakti Multi Artha | 45.21% | 32.37% | -16.43% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

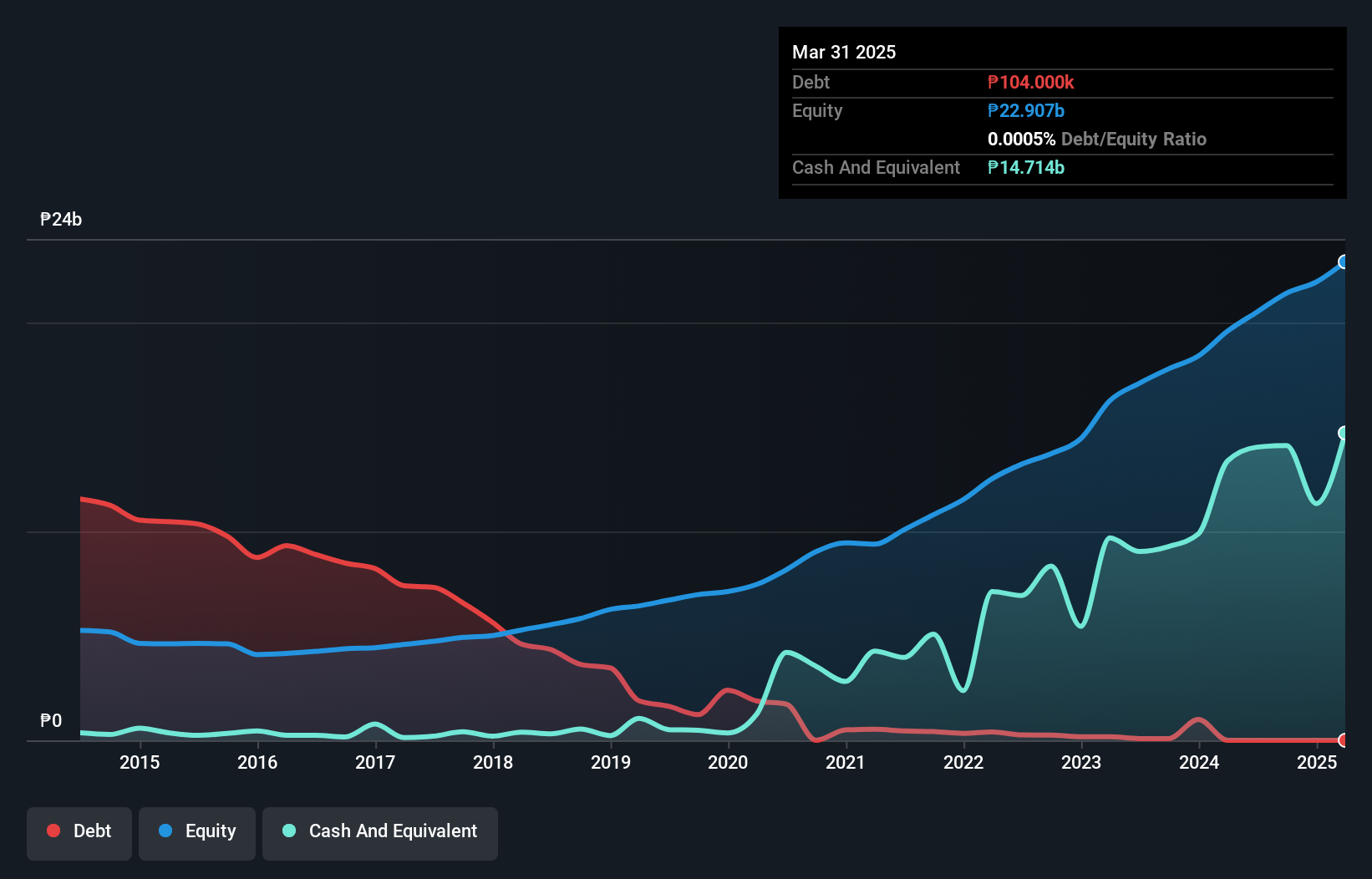

Ginebra San Miguel (PSE:GSMI)

Simply Wall St Value Rating: ★★★★★★

Overview: Ginebra San Miguel Inc., along with its subsidiaries, is involved in the production and distribution of alcoholic beverages both in the Philippines and globally, with a market capitalization of approximately ₱79.48 billion.

Operations: Ginebra San Miguel generates revenue primarily from its alcoholic beverages segment, amounting to ₱60.28 billion.

Ginebra San Miguel, a notable player in the beverage sector, showcases strong financial health with no debt and high-quality earnings. Over the past five years, its earnings have grown by 28% annually, although recent growth of 5.2% lagged behind the industry average of 10.8%. Trading at a significant discount of 61% below its estimated fair value, it appears undervalued. Recent quarterly sales hit PHP 15.57 billion compared to PHP 13.51 billion last year, while net income rose to PHP 1.77 billion from PHP 1.41 billion a year ago, indicating robust performance despite competitive pressures.

- Click here and access our complete health analysis report to understand the dynamics of Ginebra San Miguel.

Understand Ginebra San Miguel's track record by examining our Past report.

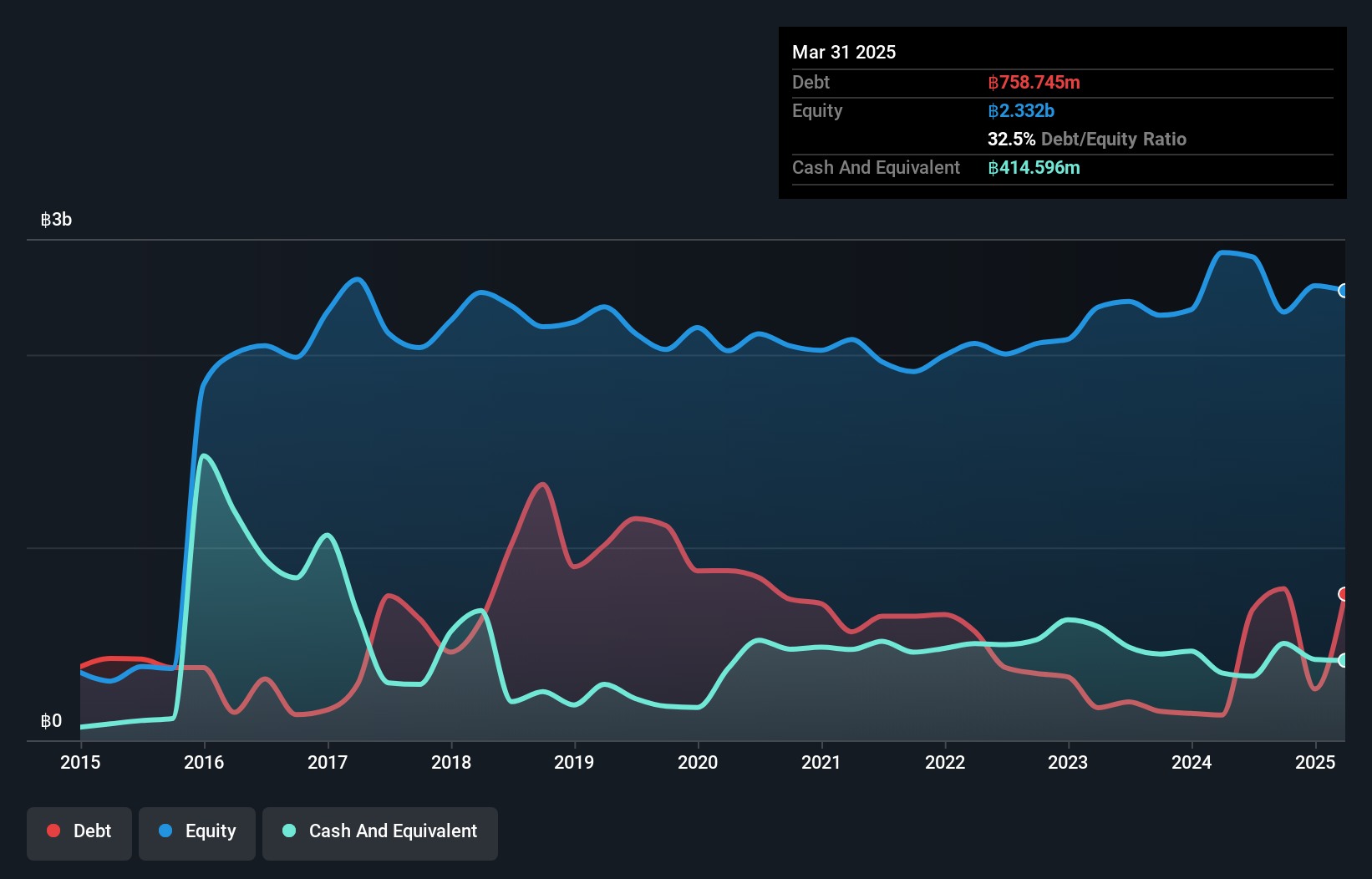

Taokaenoi Food & Marketing (SET:TKN)

Simply Wall St Value Rating: ★★★★★★

Overview: Taokaenoi Food & Marketing Public Company Limited specializes in producing and distributing various seaweed snacks, with a market cap of THB11.59 billion.

Operations: The primary revenue stream for Taokaenoi comes from its snack segment, generating THB5.85 billion. The retailer and restaurant segment contributes THB107.40 million to the overall revenue.

Taokaenoi Food & Marketing is carving its niche with a robust financial foundation, marked by a satisfactory net debt to equity ratio of 12.8% and EBIT covering interest payments 55 times over. Their earnings have impressively grown at 29.3% annually over the past five years, even though recent earnings growth of 24% trailed the broader food industry’s pace. Trading significantly below estimated fair value by 68%, this company seems undervalued in the market's eyes. A share repurchase program aims to manage excess liquidity and enhance shareholder returns, reflecting strategic financial management amidst evolving market conditions.

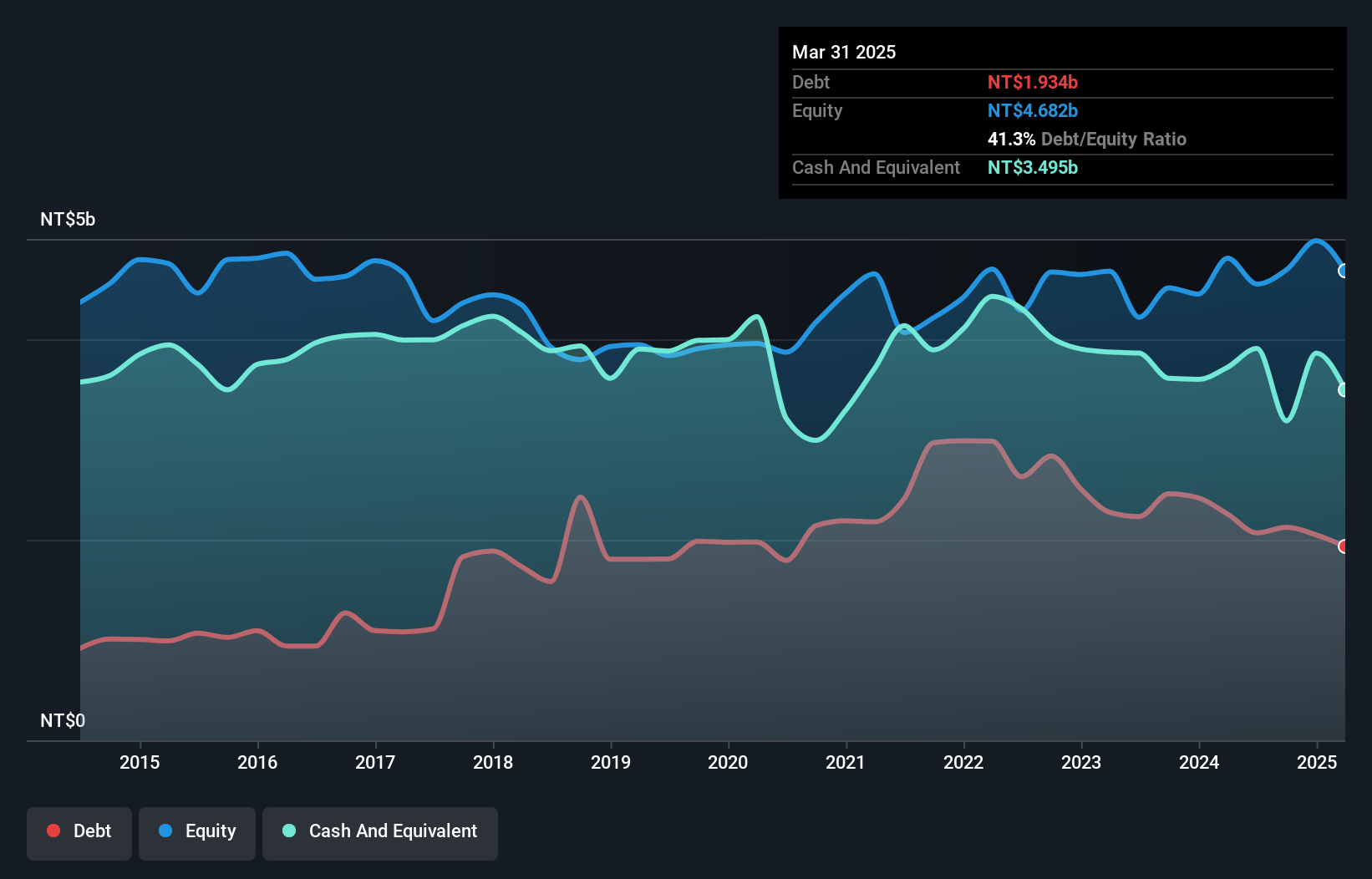

Nishoku Technology (TWSE:3679)

Simply Wall St Value Rating: ★★★★★★

Overview: Nishoku Technology Inc. designs and manufactures plastic injection molds with operations spanning Taiwan, the rest of Asia, the United States, Europe, and other international markets, and has a market cap of NT$8.70 billion.

Operations: Nishoku Technology generates revenue primarily from the provision of electronic components and related products, amounting to NT$4.03 billion. The company's financial performance can be further analyzed by examining its gross profit margin or net profit margin trends over time.

Nishoku Technology shines as a promising contender in the small-cap arena, boasting high-quality earnings and a favorable price-to-earnings ratio of 15.3x, below the TW market average. The company's debt management is commendable, with its debt-to-equity ratio improving from 50.8% to 45.3% over five years, and it holds more cash than total debt—a strong financial position indeed. Although earnings growth at 13.3% didn't surpass the machinery industry's pace of 14.6%, Nishoku's consistent profitability ensures a stable cash runway. Recent quarterly sales reached TWD 1,119 million compared to last year's TWD 931 million, highlighting robust revenue momentum despite a dip in net income from TWD 177 million to TWD 99 million for the same period.

- Navigate through the intricacies of Nishoku Technology with our comprehensive health report here.

Gain insights into Nishoku Technology's past trends and performance with our Past report.

Summing It All Up

- Dive into all 4666 of the Undiscovered Gems With Strong Fundamentals we have identified here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nishoku Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:3679

Nishoku Technology

Designs and manufactures plastic injection molds in Taiwan, rest of Asia, the United States, Europe, and internationally.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor