- New Zealand

- /

- Software

- /

- NZSE:TSK

Earnings Update: Plexure Group Limited (NZSE:PX1) Just Reported And Analysts Are Trimming Their Forecasts

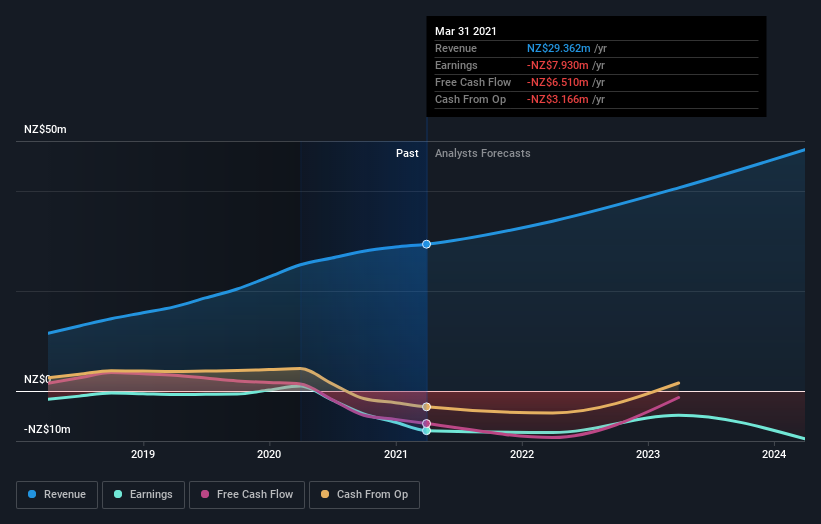

It's been a mediocre week for Plexure Group Limited (NZSE:PX1) shareholders, with the stock dropping 11% to NZ$0.68 in the week since its latest yearly results. Revenues were in line with expectations, at NZ$29m, while statutory losses ballooned to NZ$0.052 per share. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

View our latest analysis for Plexure Group

Following the latest results, Plexure Group's dual analysts are now forecasting revenues of NZ$34.0m in 2022. This would be a decent 16% improvement in sales compared to the last 12 months. Losses are supposed to decline, shrinking 14% from last year to NZ$0.045. Before this earnings announcement, the analysts had been modelling revenues of NZ$36.0m and losses of NZ$0.035 per share in 2022. So it's pretty clear the analysts have mixed opinions on Plexure Group after this update; revenues were downgraded and per-share losses expected to increase.

There was no major change to the consensus price target of NZ$1.52, signalling that the business is performing roughly in line with expectations, despite lower earnings per share forecasts.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that Plexure Group's revenue growth will slow down substantially, with revenues to the end of 2022 expected to display 16% growth on an annualised basis. This is compared to a historical growth rate of 34% over the past five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 17% annually. Factoring in the forecast slowdown in growth, it looks like Plexure Group is forecast to grow at about the same rate as the wider industry.

The Bottom Line

The most important thing to note is the forecast of increased losses next year, suggesting all may not be well at Plexure Group. They also downgraded their revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Plexure Group going out as far as 2024, and you can see them free on our platform here.

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 5 warning signs with Plexure Group (at least 1 which is concerning) , and understanding them should be part of your investment process.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if TASK Group Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NZSE:TSK

TASK Group Holdings

Engages in the development and sale of software applications primarily for the hospitality sector.

Flawless balance sheet and undervalued.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)