Kiwi Property Group (NZSE:KPG) has seen steady gains over the past month, with shares up more than 3%. Investors are watching to see if this momentum continues, especially after the stock’s strong year-to-date performance.

Momentum appears to be building for Kiwi Property Group, with a solid year-to-date share price return of nearly 19% and a robust one-year total shareholder return topping 23%. Recent price strength suggests investors are growing more optimistic about the company's outlook while also weighing shifting risks and market conditions.

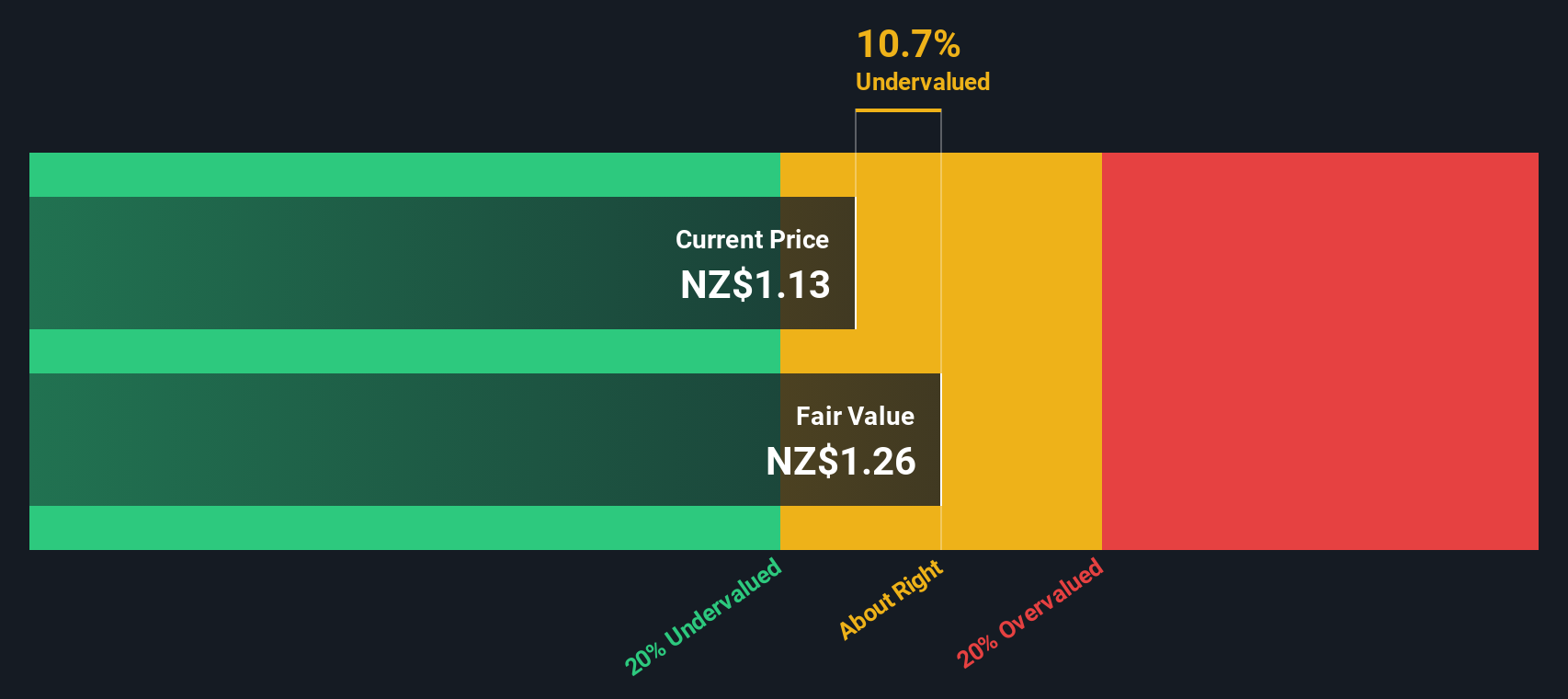

But after such a strong run over the past year, investors may be wondering whether Kiwi Property Group is still undervalued or if its recent gains already reflect all its growth prospects. Is there a genuine buying opportunity here, or has the market already priced in what lies ahead?

Advertisement

Most Popular Narrative: 7.7% Overvalued

Despite the recent price surge, the most-widely followed narrative sees Kiwi Property Group’s estimated fair value trailing its last close. The market’s optimism faces a reality check from future projections that frame current pricing in a new light.

The completion of Stage 1 earthworks at Drury and the designation as a listed project under Fast-Track Legislation highlight development progress, which could significantly impact future revenue growth as infrastructure improves. The resilience in leasing spreads and asset valuation increases, driven by strong lease renewal activity and market demand for quality mixed-use developments, indicates potential future revenue and earnings growth.

Want to know which bold financial projections are driving this call? The narrative hinges on major shifts in profit margins and a future profit multiple that challenges market norms. What is behind such a confident target? Dive in to see what the consensus believes will shape Kiwi Property Group’s next five years.

However, declining retail spending in New Zealand and recent cuts in occupancy rates could present challenges to the bullish case for Kiwi Property Group's earnings growth.

Another View: Discounted Cash Flow Offers a Different Take

While analysts see Kiwi Property Group as slightly overvalued based on earnings potential, our SWS DCF model suggests a more optimistic outlook. According to this cash flow approach, the company actually trades about 13% below its fair value. So which method paints a truer picture of value?

If you have a different perspective or like to dig into the numbers yourself, it's easy to shape your own view in just a few clicks with Do it your way.

A great starting point for your Kiwi Property Group research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Take your portfolio to the next level by tapping into new opportunities you might not have considered. These categories are moving fast, so don't let them pass you by:

Tap into emerging fields by checking out these 24 AI penny stocks to see which companies are pioneering artificial intelligence advancements.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kiwi Property Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.