Advertisement

PGG Wrightson Limited (NZSE:PGW) has announced that it will pay a dividend of NZ$0.1882 per share on the 3rd of October. This means that the annual payment will be 6.8% of the current stock price, which is in line with the average for the industry.

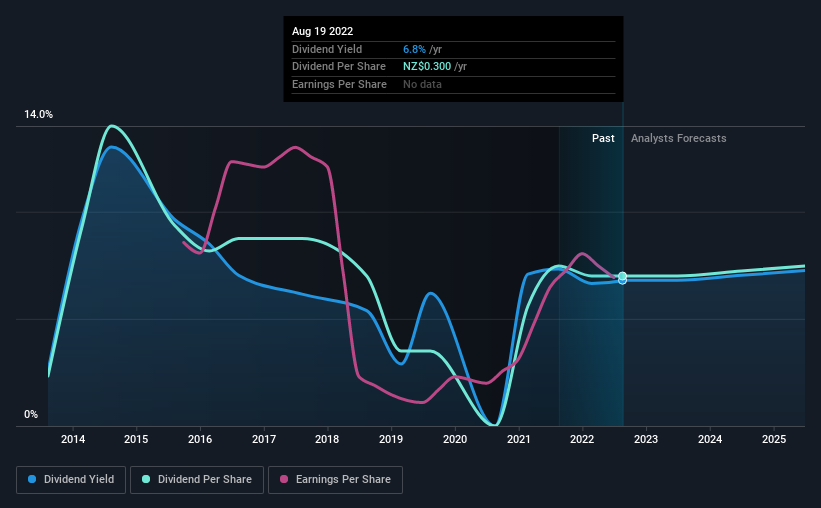

View our latest analysis for PGG Wrightson

PGG Wrightson's Earnings Easily Cover The Distributions

Solid dividend yields are great, but they only really help us if the payment is sustainable. Prior to this announcement, PGG Wrightson's dividend was making up a very large proportion of earnings and perhaps more concerning was that it was 152% of cash flows. Paying out such a high proportion of cash flows can expose the business to needing to cut the dividend if the business runs into some challenges.

Over the next year, EPS is forecast to expand by 4.1%. Assuming the dividend continues along recent trends, our estimates say the payout ratio could reach 95% - on the higher side, but we wouldn't necessarily say this is unsustainable.

PGG Wrightson's Dividend Has Lacked Consistency

It's comforting to see that PGG Wrightson has been paying a dividend for a number of years now, however it has been cut at least once in that time. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. The annual payment during the last 9 years was NZ$0.10 in 2013, and the most recent fiscal year payment was NZ$0.30. This implies that the company grew its distributions at a yearly rate of about 13% over that duration. Despite the rapid growth in the dividend over the past number of years, we have seen the payments go down the past as well, so that makes us cautious.

The Dividend Has Limited Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. PGG Wrightson's EPS has fallen by approximately 12% per year during the past five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future. On the bright side, earnings are predicted to gain some ground over the next year, but until this turns into a pattern we wouldn't be feeling too comfortable.

The Dividend Could Prove To Be Unreliable

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. The track record isn't great, and the payments are a bit high to be considered sustainable. Overall, we don't think this company has the makings of a good income stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Taking the debate a bit further, we've identified 1 warning sign for PGG Wrightson that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NZSE:PGW

PGG Wrightson

Provides goods and services for agricultural and horticultural sectors in New Zealand.

Proven track record with slight risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor